Global| Mar 10 2010

Global| Mar 10 2010UK Industrial Production Losses Momentum – So What?

Summary

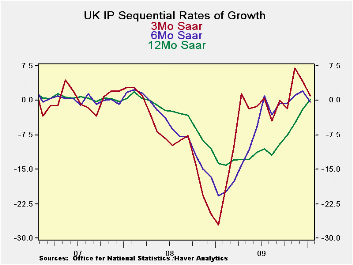

UK IP Sinks - Industrial output in the UK was set back in January unexpectedly. Consumer durables and intermediate goods output fell sharply in January a month with some considerable weather disruptions. January is sharp departure [...]

UK IP Sinks - Industrial output in the UK was set back in January unexpectedly. Consumer durables and intermediate goods output fell sharply in January a month with some considerable weather disruptions. January is sharp departure from December when output rose by 0.9% on advances in all major sectors. The detailed industry results do not show anything worrisome as the key detailed industries do not reveal any with back-to-back declines. Instead we see a 5.5% drop for textile and leather after a 3.4% gain in December- that is volatility not weakness. Motor vehicles also saw output fall by 2% in January after surging by 5.6% in December. While the January result was unexpected, ‘unexpected’ does always mean the start of a new trend, sometimes it is just a spate of volatility.

Unexpected events elsewhere - The month brought other unexpected developments elsewhere as German exports fell and the German trade surplus was chopped nearly in half, unexpectedly. We might be worried except that this German report was preceded by a very strong orders report that had strong foreign orders well represented. The German CPI was up a bit more than expected as well – something the ECB will be watching. In Asia, China’s exports were so strong they had everyone geared for the prospect of some sort of global demand revival. Japan’s core machinery orders, strong in a previous release, backed off in this month’s report setting back hopes for an investment revival there. The truth of the global economy is hidden somewhere in this tangle of volatile monthly reports.

Warning! Caveat recovery - UK Prime Minister Gordon Brown warned on the fragility of the expansion saying data would continue to go to and fro and that recovery was not assured. Thanks for that confidence booster…

Biz as usual - What you usually can depend on in recovery periods is to get mixed signals. That much appears to still be true. One source of volatility and concern may be lessening, however. Former EU Commission Prodi declared the Greek crisis to be over and while that could be a bit of good news we have to wonder if the declaration is premature given the nature of Greece’s difficulties and past transgressions. One good bond offering with high interest rates hardly signals that all is well. Spain, Portugal and Italy will remain as EMU countries under the markets’ sharpest eye in the wake of the Greek problem even if Greece remains on an upswing.

Caveats aside, odds and data still favor the recovery continuing - The UK recovery has flashed hot and cold signs for some time in this cycle. The BOE is letting an inflation overshoot go by without acting, a clear indication that the Bank does not see any overheating. Data releases like today’s IP report only confirm the good judgment of the Bank and its ability to see past monthly volatility in the run of reports. The most likely situation is that growth in the UK and elsewhere continues. The recession was deep, there is pent up demand, in Europe; the strong social welfare system there helps to preserve demand. Meanwhile, recovery still seems to be afoot around the world and for the most part trade data have been strong confirming that some sort of global revival is in place. While German export data may seem to question the notion of strong growth and global economic revival, strong growth in China’s exports seems to brand the German data as anomalies (along with German order flows). As always we will stay tuned to the various monthly reports. But there is no basis for the belief that the recovery is being untracked apart from a streak of pure pessimism.

Pessimists unite! You have nothing to lose since nothing is invested in the market! - We know pessimism is still alive and well and that part of that reluctance traces to the still low level interest rates. Central banks are reluctant to boost rates even though market rates are for the most part high above the levels banks are paying in the interbank markets. Low official rates are contributing to money (wealth) staying on the sidelines. We have had a very strong one-year rally in global stock markets with low participation because so many have been unwilling to commit funds even though he past year’s rally was one of extraordinary scope. Money is continuing to pile up on the sidelines and pessimism is now partly the product of a sour grapes attitude by would-be investors who clearly have stayed on the side lines for far too long. These sorts of considerations dog the ability of those who have stayed out to objectively characterize the progress of the markets and offer an unbiased the assessment of the economy and its prospects. It will take a period of job growth being restored and rates elevating to bring these skeptical once-burned twice-shy (and therefore burned again by a different sort of fire) investors back to the markets. Until then expect each monthly setback to be greeted by the hoots and hollers of the pessimists who have sat back and largely missed the rally to date. It’s all the fun that they can have.

| UK IP and MFG | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Saar except m/m | Mo/Mo | Jan 10 |

Dec 09 |

Jan 10 |

Dec 09 |

Jan 10 |

Dec 09 |

|||

| UK MFG | Jan 10 |

Dec 09 |

Nov 09 |

3Mo | 3Mo | 6mo | 6mo | 12mo | 12mo | Q1 Date |

| MFG | -0.8% | 0.9% | 0.1% | 0.9% | 4.1% | -0.4% | 2.0% | 0.2% | -2.0% | -0.9% |

| Consumer | ||||||||||

| C-Durables | -1.8% | 0.7% | -1.0% | -7.9% | -4.6% | 1.7% | 7.3% | -0.2% | -0.2% | -9.4% |

| C-Non-durables | 0.3% | 0.2% | -0.2% | 1.3% | -3.8% | -3.9% | -3.1% | -1.4% | -1.2% | 2.4% |

| Intermediate | -1.3% | 0.4% | 0.7% | -1.0% | 3.0% | -6.3% | -3.8% | -4.6% | -6.6% | -5.0% |

| Capital | 0.8% | 1.0% | 0.7% | 10.1% | 16.3% | 10.5% | 9.1% | 4.9% | -0.9% | 10.3% |

| Memo: Detail | 1Mo% | 1Mo% | 1Mo% | 3Mo | 3Mo | 6mo | 6mo | 12mo | 12mo | Q1 Date |

| Food Drink&tobacco | 4.1% | -0.1% | -1.4% | 10.5% | -7.7% | 1.2% | -5.1% | 2.0% | -0.5% | 23.0% |

| Textile&Leather | -5.5% | 3.4% | -5.2% | -26.6% | -18.4% | -15.6% | -4.4% | -9.1% | -6.7% | -27.2% |

| Motor Vehicles & trailer | -2.0% | 5.6% | 2.2% | 24.7% | 30.3% | 13.5% | 37.0% | 26.8% | 8.3% | 14.4% |

| Mining and Quarry | 1.4% | -4.9% | 5.1% | 5.6% | 4.0% | -10.1% | -13.4% | -8.8% | -12.0% | -1.9% |

| Electricity, gas&H2O | 1.3% | 3.9% | -3.3% | 7.3% | -4.7% | -0.6% | -4.7% | -5.2% | -6.7% | 17.7% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief