Global| Aug 23 2013

Global| Aug 23 2013UK GDP Is Even Stronger

Summary

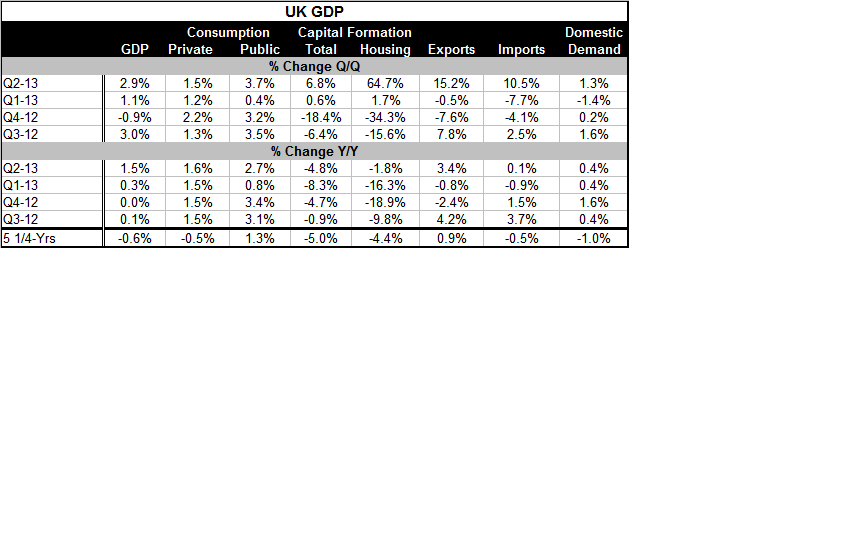

The UK economy expanded 0.7% (Q/Q) in the second quarter, in a revised GDP statement issued today. The new GDP growth rate exceeds the initial estimate of 0.6%. GDP is now advancing at a 2.9% annual rate in the quarter and is up by [...]

The UK economy expanded 0.7% (Q/Q) in the second quarter, in a revised GDP statement issued today. The new GDP growth rate exceeds the initial estimate of 0.6%. GDP is now advancing at a 2.9% annual rate in the quarter and is up by 1.5% Year-over-year in Q2. Construction and manufacturing seem to have performed slightly better in this second pass at estimating GDP.

Trade is the most important contributor to growth in the second quarter. UK export data have been showing strength recently, so this result is no surprise. Export data for the euro-Zone has also showed some pick up. There is evidence of demand stirring in the global economy, although just where that is remains a bit difficult to puzzle out. UK exports jumped at a 15.2% annual rate in real terms in Q2. The quarterly gain in UK exports is the strongest since Q4 of 2011. Meanwhile, imports are advancing as well as domestic demand is reviving. Imports rose at a strong 10.5% annual rate in 2013-Q2- still short of the pace for exports. On the year exports are up by 3.4% compared to imports at 0.1%.

During the downturn and weak recovery public expenditures and exports have helped to soften the blow on the economy as both of those flows have net gains over the period and government spending was always a positive force in GDP while exports have had only a few negative contributions to GDP during the downturn and weak recovery. Imports also have reduced the blow to GDP as they are still lower on average by 0.5%, over the last five and one-quarter years. Imports are a subtraction from GDP. Private consumption has averaged a pace of decline of 0.5% over the last 5 1/4 years as domestic demand averaged a 1% decline. Housing, as always, was weak with an average rate of decline on this period of 4.4%.

However, the big issue has been capital formation. For all of the efforts to try to craft and austerity program that might still return the economy to growth quickly, capital formation fell harder in the last 5 1/4 years on average than other major GDP component, averaging a pace of contraction of 5%- even more severe than that of housing.

In revised data capital formation spending is beginning to pick up. However, it is still lower on balance when measured year-over-year.

The UK economy is doing better than the euro-Zone, although not quite as well as Germany. Recent UK indicators including a robust report from the CBI showing a strong domestic and export order component make it look as though the economy is on the right track. Services are still listless, however.

The UK economy is still importantly plugged into the EMU area where growth, though stirring, has poor underpinnings. The UK itself has a still extraordinary monetary policy being run. The UK growth data have better underpinnings the does the euro-Zone as a whole, but the UK also faces its own issues; like most advanced economics fiscal policy is on the check-list of things it must pay attention to. Many key financial institutions still need a good deal of attention. As growth becomes better-established many of the highly industrialized economies are going to have turn their attention from trying to make their recovery speed even faster to shoring up their excessive fiscal imbalances and banking systems. Growth will do some of the fixing, but not all of it.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief