Global| May 17 2010

Global| May 17 2010UK CBI Trends Are Up

Summary

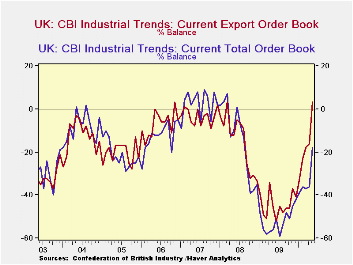

The UK CBI index improved sharply and much more sharply than expected in May. The orders index jumped from a -36 reading to -18, remaining negative but halving its negative reading. The result was completely unexpected. Export orders [...]

The UK CBI index improved sharply and much more sharply than expected in May. The orders index jumped from a -36 reading to -18, remaining negative but halving its negative reading. The result was completely unexpected. Export orders have improved to the point where their reading is positive for the first time since early 2008. The overall all orders index has just made the largest jump month to month since at least 1989.

The 3-month-ahead volume outlook index improved this month to a net balance reading of +17 from +14 in April. April has seen a big boost to +14 from +5 in March. The outlook volume index stands in the 77th percentile of its range which is a pretty strong standing. The export reading has tied its high since 1996 and has seen no higher reading since August of 1995.

This sort of industrial turnaround could put the BOE on the defensive. UK inflation data have not been good. But if the economy shows signs of strength the inflation data could come to have a more pejorative interpretation.

For now the rise in the industrial in orders index is sharp but only brings it to a reading of -18. Still that is a 58th percentile reading and, by itself, that is not as weak-sounding to me as a minus eighteen scoring sounds. So the BOE has balance for now. The industrial sector seems to be making a push but it is still showing a lot of weakness. Still, the main point stands. The stronger that the industrial sector and the rest of the economy gets, the more that any inflation overshoot will begin to worry the BOE.

| UK Industrial volume data CBI Survey | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Reported: | May 10 |

Apr 10 |

Mar 10 |

Feb 10 |

Jan 10 |

12MO Avg | Pcntle | Max | Min | Range |

| Total Orders | -18 | -36 | -37 | -36 | -39 | -47 | 58% | 13 | -61 | 74 |

| Export Orders | 3 | -16 | -18 | -23 | -33 | -40 | 77% | 20 | -55 | 75 |

| Stocks:FinGds | 10 | 10 | 5 | 12 | 13 | 16 | 36% | 31 | -2 | 33 |

| Looking ahead | ||||||||||

| Output Volume:Nxt 3M | 17 | 14 | 5 | 7 | 4 | -3 | 77% | 36 | -48 | 84 |

| Avg Prices 4Nxt 3m | 16 | 17 | 8 | 8 | -6 | -3 | 69% | 37 | -30 | 67 |

| From early 1989 | ||||||||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief