Global| Sep 10 2009

Global| Sep 10 2009U.S. Weekly Claims For JoblessInsurance Near Cycle Low

by:Tom Moeller

|in:Economy in Brief

Summary

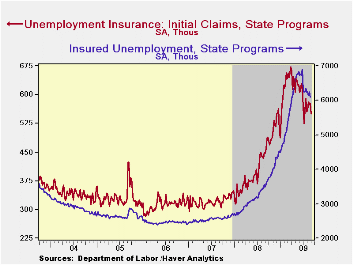

Initial claims for jobless insurance have been suggesting improvement in the labor market, however grudging. For last week, the Labor Department indicated that claims fell 26,000 to 550,000 which was their lowest level since early- [...]

Initial claims for jobless insurance have been suggesting improvement in the labor market, however grudging. For last week, the Labor Department indicated that claims fell 26,000 to 550,000 which was their lowest level since early-July and down from the March weekly peak of 674,000. The latest decline about matched expectations.

Continuing claims for unemployment insurance during the latest week fell and more than reversed all of the prior period's increase. The decline was to the lowest level since early-April and claims were down by 10% from the late-June high, a decline which probably owes partially to the exhaustion of benefits. Continuing claims provide an indication of workers' ability to find employment. The level of 6,088,000 claims is up sharply from the year-ago level. The four-week average of continuing claims fell modestly to 6,182,500. The series dates back to 1966.

Extended benefits for unemployment insurance slipped for the

fourth week in the last five. Nevertheless, the trend in benefits has

been sharply upward as worker rehiring continues weak. Through

mid-August extended benefits averaged 453,831 versus 416,630 during

July.

The insured rate of unemployment dipped slightly to 4.6% and was near the lowest level since mid-April. The rate reached a high of 5.2% during late-June. During the last ten years, there has been a 93% correlation between the level of the insured unemployment rate and the overall rate of unemployment published by the Bureau of Labor Statistics.

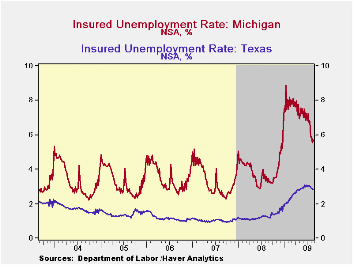

The highest insured unemployment rates in the week ending Aug. 22 were in Puerto Rico (7.0 percent), Pennsylvania (5.9), Oregon (5.9), Michigan (5.7), Nevada (5.7), California (5.3), Wisconsin (5.3), Connecticut (5.2), New Jersey (5.1), North Carolina (4.8), Rhode Island (4.8), and South Carolina (4.8).

The unemployment insurance claims data is available in Haver's WEEKLY database and the state data is in the REGIONW database.

| Unemployment Insurance (000s) | 09/05/09 | 08/29/09 | 08/22/09 | Y/Y | 2008 | 2007 | 2006 |

|---|---|---|---|---|---|---|---|

| Initial Claims | 550 | 576 | 574 | 23.0% | 420 | 321 | 313 |

| Continuing Claims | -- | 6,088 | 6,247 | 71.5% | 3,342 | 2,552 | 2,459 |

| Insured Unemployment Rate (%) | -- | 4.6 | 4.7 | 2.7 (08/2008) | 2.5 | 1.9 | 1.9 |

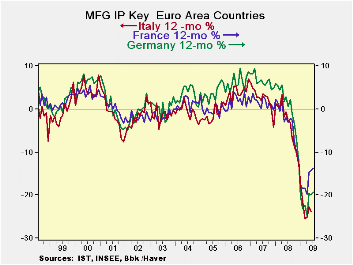

IP In France Edges Higher In July

by Robert Brusca September 10, 2009

French industrial production rose by a thin margin of 0.1% in

June, less than expected. Auto production contracted after a strong

spurt in earlier months. Still, France has showed one of the stronger

rebounds in EMU IP. It did not sink as far as German IP but it has

rebounded just as much.

In France consumer durables output fell by a sharp 2.6% in

July. For nondurables consumer output was up by 1.1%. Capital goods

output took a set back despite what has been a solid run of growth for

that sector. Intermediate goods output rose strongly in July.

Trends in French IP are up strongly and across the board with

the exception of consumer durables.

In the current quarter output is rising at a 7.7% annual rate

with all main sectors doing better than that except, again, consumer

durables which is contracting in the new quarter and weighing down the

headline. On balance the rebound is robust and seems well entrenched.

The lack of progress in consumer durable goods is however a fly in the

recovery ointment. It suggests that consumers are able to be coaxed out

to buy some things but that they do not have the fundamental confidence

to take on the bigger-ticket items.

| French IP Excluding Construction | |||||||

|---|---|---|---|---|---|---|---|

| Saar exept m/m | Jul-09 | Jun-09 | May-09 | 3-mo | 6-mo | 12-mo | Quarter -To-Date |

| IP total | 0.1% | 0.2% | 3.0% | 13.9% | -0.7% | -13.0% | 7.7% |

| Consumer Dur | -2.6% | -2.9% | 0.8% | -17.8% | -20.9% | -21.5% | -23.3% |

| Consumer Ndur | 1.1% | 0.3% | 0.0% | 5.9% | -3.4% | -2.3% | 11.1% |

| Capital | -0.2% | 1.1% | 4.0% | 21.0% | 7.4% | -15.0% | 11.1% |

| Intermed | 1.6% | -0.1% | 3.7% | 22.7% | 4.4% | -19.6% | 17.9% |

| Memo | |||||||

| Auto | -1.9% | 14.3% | 12.5% | 154.2% | 23.2% | -29.8% | 87.2% |

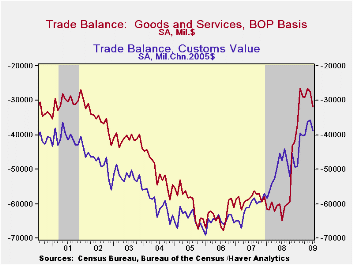

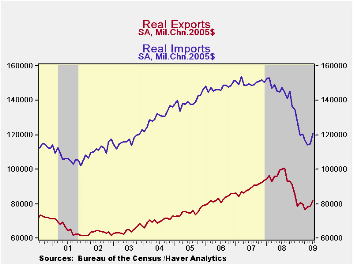

U.S. Trade Deficit Deepens With A Jump In Imports

by Tom Moeller September 10, 2009

Improvement in the U.S. economy probably is behind the July deterioration in the international trade deficit to $32.0B versus a little-revised June deficit of $27.5B. Consensus expectations had been for a deficit of $27.0B. Nonoil imports reversed six months of decline with a 6.1% m/m gain, though that still left them down by one-quarter from the year-ago level. A 3.6% rise in oil imports reflected higher prices. Real petroleum imports slipped m/m and are off 10.8% y/y with the recession. For the third straight month, U.S. exports posted a strong gain. The competitive foreign exchange value of the dollar helped exports to rise by 2.2%, about as they did during May and June. The gains pared the YTD drop to 4.0%.

Adjusted for price inflation overall and for higher oil prices

specifically, the trade deficit in goods deepened somewhat during July

to $38.8B after having fallen to the lowest level since June 1999. It

was down from the peak of $47.6B last July. Real non-auto consumer

goods imports jumped 5.3% m/m but remained off 12.5% from last year.

Real automotive vehicles & parts imports jumped 21.3% and pared

the y/y drop to 33.8%. Non-auto capital goods imports rose 4.3% but

that still left them off one-quarter from last year.

The rise in petroleum imports was driven by higher crude oil prices. Prices rose to a July average of $62.48 per barrel versus the February low of $39.22. The recession and the rise in prices, however, prompted a decline in the volume of petroleum imports. Despite a June gain they have fallen roughly ten-percent since December.

Reflecting the competitive value of the dollar, real merchandise exports jumped 3.9% after two months of lesser increase. The chained dollar value of auto exports led the gain with a 24.7% increase (-40.9% y/y). Non-auto consumer goods exports rose a lesser 2.7% (-14.6% y/y) while real capital goods exports gained 2.2% (-20.0 y/y) for the second month of strong increase.

The international trade data can be found in Haver's USECON database. Detailed figures are available in the USINT database.

| Foreign Trade | July | June | Y/Y | 2008 | 2007 | 2006 |

|---|---|---|---|---|---|---|

| U.S. Trade Deficit | $32.0B | $27.5B | $64.9B (7/08) | $695.9 | $701.4 | $760.4 |

| Exports - Goods & Services | 2.2% | 2.1% | -22.4% | 11.2% | 13.2% | 13.3% |

| Imports - Goods & Services | 4.7% | 2.5% | -30.4% | 7.6 | 6.0% | 10.8% |

| Petroleum | 3.6% | 24.3% | -55.0% | 37.0% | 9.4% | 20.1% |

| Nonpetroleum Goods | 6.1% | -1.1% | -25.7% | 1.5% | 4.8% | 9.1% |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief