Global| Dec 04 2007

Global| Dec 04 2007U.S. Vehicle Sales Still Driven By Gasoline Prices

by:Tom Moeller

|in:Economy in Brief

Summary

U.S. sales of light vehicles nudged up 0.9% last month to a 16.20M unit annual selling rate, according to the Autodata Corporation. The uptick followed declines in four of the prior five months. Nevertheless, sales so far in 4Q are [...]

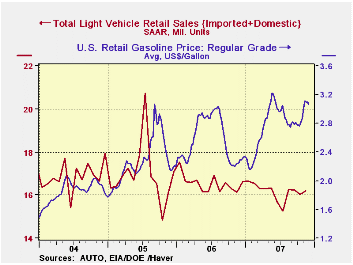

U.S. sales of light vehicles nudged up 0.9% last month to a 16.20M unit annual selling rate, according to the Autodata Corporation. The uptick followed declines in four of the prior five months. Nevertheless, sales so far in 4Q are running slightly ahead of the 3Q average due to an abysmal start to that quarter.

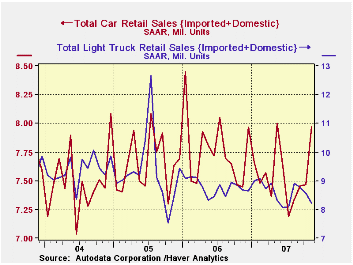

Sales of domestically made light vehicles improved 1.0% m/m to 12.20M units (0.1% y/y). The gain came as sales of U.S. made cars jumped 9.9% to 5.47M units and that more than offset a 4.8% m/m drop in sales of domestic light trucks, still feeling the effects of higher gas prices. It was the third sharp m/m decline in U.S. made light truck sales.

Sales of imported light vehicles inched up 0.4% after firm gains during the prior two months. The rise to 4.00M units (1.4% y/y) was to the highest level since June. The increase was due to a 1.5% gain in sales of imported autos which was the third strong gain in as many months. Sales of imported light trucks fell a moderate 1.4% after a like increase in October.

Import's share of the U.S. light vehicle market remained stable m/m at 24.7% versus an average 23.1% for all of last year.

U.S. Economic Growth Will Be Somewhat Below Potential in 2008 according to participants of the Chicago Fed Economic Outlook Symposium and the news release is available here.

| Light Vehicle Sales (SAAR, Mil. Units) | November | October | Y/Y | 2006 | 2005 | 2004 |

|---|---|---|---|---|---|---|

| Total | 16.20 | 16.05 | 0.4% | 16.55 | 16.96 | 16.87 |

| Autos | 7.97 | 7.47 | 7.0% | 7.77 | 7.65 | 7.49 |

| Domestic | 5.47 | 5.01 | 9.9% | 5.31 | 5.40 | 5.36 |

| Imported | 2.50 | 2.46 | 1.2% | 2.45 | 2.25 | 2.14 |

| Light Trucks | 8.22 | 8.59 | -5.3% | 8.78 | 9.32 | 9.37 |

| Domestic | 6.73 | 7.07 | -6.8% | 7.42 | 8.12 | 8.15 |

| Imported | 1.49 | 1.52 | 1.9% | 1.37 | 1.20 | 1.23 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief