Global| Sep 11 2008

Global| Sep 11 2008U.S. Total Import Prices Fell With Oil Price Decline

by:Tom Moeller

|in:Economy in Brief

Summary

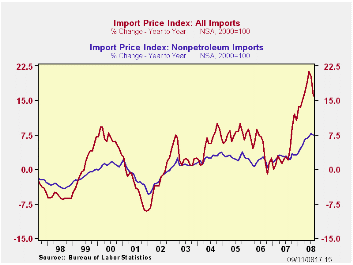

U.S. import prices overall slid 3.7% last month. The decline followed a revised 0.2% July uptick and gains between 2.0% and 3.0% during the prior four months. The August decline was double expectations for a 1.5% drop. The decline was [...]

U.S. import prices overall slid 3.7% last month. The decline followed a revised 0.2% July uptick and gains between 2.0% and 3.0% during the prior four months. The August decline was double expectations for a 1.5% drop.

The decline was paced by a 12.8% drop in petroleum prices and the price index returned nearer to its April level. This month imported crude petroleum prices already are down another 10% .

Less petroleum, import prices slipped 0.3 after a downwardly revised 0.7% July increase. During the last three months prices rose at a 4.6% annual rate, down sharply from the 12-13% growth of this past spring. Growth in import prices, eventually, will slow further given the recent rise in the foreign exchange value of the dollar. During the last ten years there has been a 66% (negative) correlation between the nominal trade-weighted exchange value of the US dollar vs. major currencies and the y/y change in non oil import prices. The correlation is a reduced 47% against a broader basket of currencies.

Prices for industrial supplies & materials excluding oil fell 1.7% and reversed the July gain. Three-month growth of 13.7% (AR) is down due to slower gains in prices for iron & steel products, unfinished metals and chemicals. These detailed import price series can be found in the Haver USINT database.

Capital goods import prices slipped 0.1% after a downwardly revised 0.2% increase during July. On a three-month basis prices were unchanged. Less the lower prices of computers, capital goods prices rose 0.2% after a 0.7% July rise. Three month growth of 4.4% was half its peak and they rose 2.7% last year. Prices of computers, peripherals & accessories fell 1.0% last month, about as they did during the prior three months.

Finally, prices for nonauto consumer goods were unchanged last month and the 1.5% rate of increase during the last three months is down from the 5.9% peak earlier this year. The diminished rate of increase for durables of 1.6% is notable.

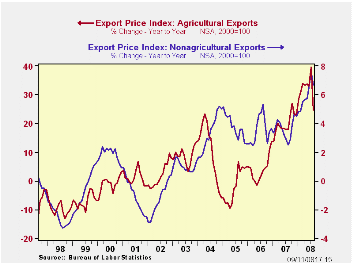

Total export prices reversed their July surge and fell 1.7% as agricultural prices slumped 9.6% (+24.8% y/y). Nonagricultural export prices reversed their July increase and fell 0.7% (+6.7% y/y).

| Import/Export Prices (NSA, %) | August | July | Y/Y | 2007 | 2006 | 2005 |

|---|---|---|---|---|---|---|

| Import - All Commodities | -3.7 | 0.2% | 16.0% | 4.2% | 4.9% | 7.5% |

| Petroleum | -12.8 | -1.0 | 52.0 | 11.6 | 20.6 | 37.6 |

| Non-petroleum | -0.3 | 0.7 | 7.5 | 2.7 | 1.7 | 2.7 |

| Export- All Commodities | -1.7 | 1.5 | 8.2 | 4.9 | 3.6 | 3.2 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief