Global| Oct 14 2008

Global| Oct 14 2008U.S. Small Business Optimism Rose Further

by:Tom Moeller

|in:Economy in Brief

Summary

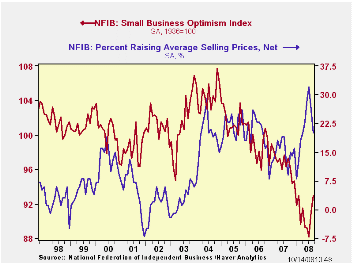

According to the National Federation of Independent Business (NFIB), small business optimism rose another 2.0% during September to the highest level since February. The rise to an index level of 91.1 added to a gain of 3.3% during [...]

According to the National Federation of Independent Business (NFIB), small business optimism rose another 2.0% during September to the highest level since February. The rise to an index level of 91.1 added to a gain of 3.3% during August.

During the last ten years there has been a 70% correlation between the level of the NFIB index and the two quarter change in real GDP.

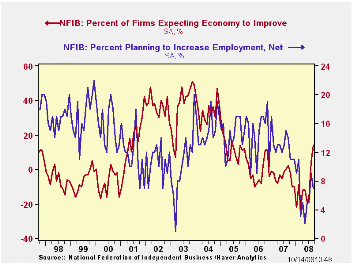

The percent expecting the economy to improve rose again, last month to the highest level since late 2005.

The percentage planning to raise employment dipped slightly to 7%, still near the highest level since February. The percentage of respondents with one or more job openings improved to 18% which was the highest level since June. During the last ten years there has been a 71% correlation between the NFIB employment percentage and the y/y change in nonfarm payrolls.

The percentage of firms actually raising prices fell to 20%, the lowest level since April. During the last ten years there has been a 64% correlation between the y/y change in the producer price index and the level of the NFIB price index. The percentage of firms planning to raise prices also fell further to 24% which was the least since February.

The largest, single most important problems seen by business were poor sales (20%), inflation (16%), insurance cost and availability (10%) and taxes (17%). The latter, however, still was reduced from 27% in early 2007.

About 24 million businesses exist in the United States. Small business creates 80% of all new jobs in America.

The NFIB figures can be found in Haver's SURVEYS database.

The Federal Reserve and other central banks announce further measures to provide broad access to liquidity and funding to financial institutions. Visit the U.S. Federal Reserve site here for more info.

| Nat'l Federation of Independent Business | September | August | Y/Y | 2007 | 2006 | 2005 |

|---|---|---|---|---|---|---|

| Small Business Optimism Index (1986=100) | 92.9 | 91.1 | -4.5% | 96.7 | 98.9 | 101.6 |

by Tom Moeller October 14, 2008

Credit Card Debt and Payment Use from the Federal Reserve Bank of Boston is available here.

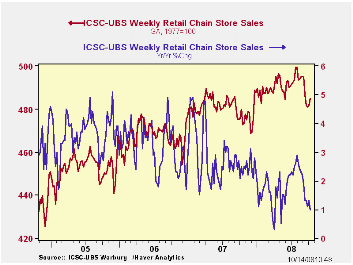

| ICSC-UBS (SA, 1977=100) | 10/11/08 | 10/04/08 | Y/Y | 2007 | 2006 | 2005 |

|---|---|---|---|---|---|---|

| Total Weekly Chain Store Sales | 484.7 | 481.5 | 1.0% | 2.8% | 3.3% | 3.6% |

by Louise Curley October 14. 2008

The September reading of the Bank of France's monthly business survey in industry and the October reading of the ZEW indicator in Germany give some indication of the mood of the French and the Germans as financial conditions worsened world wide.

The indicator of sentiment among French businessmen fell 6.82 points in September to 86.97, 13% below its long term average of 100, but still some 12 points above the low of 74.97 reached in July, 1993. (See the first chart.) The French survey was taken during the first five working days of September when worse news was yet to come.

The ZEW survey was conducted in late September through October 13. According to institutional investors and analysts in Germany, macroeconomic expectations, which had become less negative in August and September, fell sharply in October. The excess of pessimists over optimists increased 21.9 points to 63.0%, just below the all time high of 63.9% in July of this year. The ZEW measure of current conditions dropped 34.6 points in October, even more sharply than the measure of expectations. The measure of current conditions had been positive through July of this year. The ZEW measures of current conditions and of expectations are shown in the second chart.

The ZEW press release noted: "A separate analysis was made for 39 answers that came in on October 13th, the day on which the German Government decided in favour of a rescue package for the German banking sector. It shows that the decline of the economic expectations for Germany was less pronounced after the decision on the rescue package was made.".

| MEASURES OF SENTIMENT | Oct 08 | Sep 08 | Aug 08 | Jul 08 | Jun 08 | May 08 |

|---|---|---|---|---|---|---|

| Bank of France Business Survey | 86.97 | 93.79 | 91.58 | 94.95 | 95.88 | |

| ZEW | ||||||

| Macro Expectations (% balance) | -63.0 | -10.1 | -55.5 | -63.9 | -52.4 | -41.4 |

| Current Conditions (% balance) | -35.9 | -1.0 | -9.2 | 17.0 | 37.6 | 38.6 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.