Global| Nov 09 2007

Global| Nov 09 2007U.S. September Trade Deficit Smallest Since 2005

by:Tom Moeller

|in:Economy in Brief

Summary

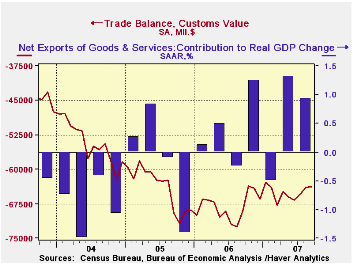

The September U.S. foreign trade deficit fell to $56.5B, the smallest since May 2005. The deficit for August was revised shallower from the initial report and the latest figure was a surprise to Consensus expectations for a deeper [...]

The September U.S. foreign trade deficit fell to $56.5B, the smallest since May 2005. The deficit for August was revised shallower from the initial report and the latest figure was a surprise to Consensus expectations for a deeper deficit of $58.5B.

The deficit averaged $58.6B during the first nine months of this year compared to an average of $64.6B during the first nine months of 2006.

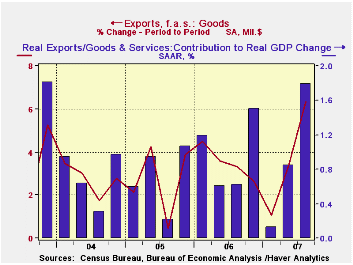

U.S. exports jumped 1.1% after the small 0.7% rise in August which was revised up slightly.

Exports of goods recovered 1.3% (14.1% y/y) after just a 0.4% up tick in August. Exports of nonauto consumer goods led the gain with a 2.6% surge (18.4% y/y). Exports of foods, feeds & beverages also jumped 9.4% (42.4% y/y) after a 7.9% August surge.Exports of autos & products rose 0.7% (18.5% y/y). Exports of capital goods fell 1.0% ( +7.8% y/y), for the second consecutive month of decline, led by a 7.5% drop in exports of civilian aircraft (+8.1% y/y. Exports of advanced technology goods also fell by 1.5% (+3.9% y/y).

U.S. exports of services rose 0.7% (12.5% y/y) after an upwardly revised 1.4% August gain.

Overall imports rose 0.6% though imports of petroleum products fell 0.2% (+4.6% y/y) after a very much downwardly revised gain of 0.1% during August. Imports of nonauto consumer goods rose 0.5% (4.0% y/y) and capital goods imports jumped 2.0% (6.8% y/y). Imports of advanced technology products increased 0.4% (7.1% y/y).

The U.S. trade deficit in goods with China deteriorated m/m to $23.8B versus a deficit of $22.9B during September of '06. During the first nine months of this year the deficit with China averaged $20.8B versus $18.5B in 2006. Exports rose 16.6% and imports rose 13.5%.

International Trade: Why We Don’t Have More of It from the Federal Reserve Bank of Philadelphia is available here.

Is the United States Losing Its Productivity Advantage? from the Federal Reserve Bank of New York can be found here.

| Foreign Trade | September | August | Y/Y | 2006 | 2005 | 2004 |

|---|---|---|---|---|---|---|

| U.S. Trade Deficit | $56.5B | $56.8B | $64.1B (9/06) |

$758.5 | $714.4B | $612.1B |

| Exports - Goods & Services | 1.1% | 0.7% | 13.6% | 12.7% | 10.9% | 13.7% |

| Imports - Goods & Services | 0.6% | -0.7% | 4.9% | 10.4% | 12.9% | 16.8% |

by Tom Moeller November 9, 2007

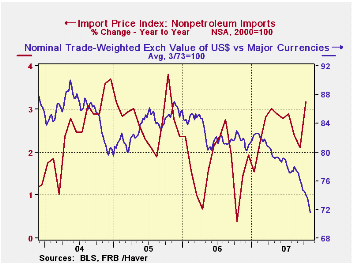

U.S. import prices during October surged 1.8%, the largest one month gain since May of last year, as petroleum prices jumped. Consensus expectations had been for a 1.1% increase.

Prices of petroleum products rose jumped 6.9% as Brent crude oil prices rose 7.4% to an average $82.70 per barrel.

Less petroleum, the 0.5% gain in import prices was the largest one month gain since May and the y/y gain in prices of 3.2% was the fastest since the end of 2005.The lower dollar is having its effect in raising import prices. During the last ten years there has been a 66% (negative) correlation between the nominal trade-weighted exchange value of the US dollar vs. major currencies and the y/y change in non oil import prices. The correlation is a reduced 47% against a broader basket of currencies.

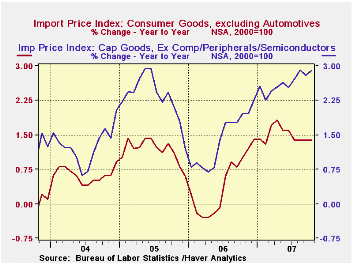

So far, the dollar's effect has been moderate but it has led to a turnaround in pricing pressure. Capital goods prices less the high tech sector rose 0.2% in October (2.9% y/y) but that y/y gain is an acceleration from the 1.4% rise during all of 2006. Consumer goods prices rose 0.1% for the third straight month, but again, the y/y rise of 1.4% is up from the 0.4% 2006 increase. Imported motor vehicle & parts prices rose 0.4% producing a y/y gain of 1.2%, double last year's gain.

Why a Dollar Depreciation May Not Close the U.S. Trade Deficit from the Federal Reserve Bank of New York is available here.

Prices for industrial supplies & materials excluding petroleum surged 1.5% after three months of decline, lifting the y/y change to 8.9% and continuing the strength of the last several years. The detailed import price series can be found in the Haver USINT database.

Overall export prices increased 0.9%. Prices for agricultural products jumped another 3.9% (26.8% y/y) and nonagricultural export prices rose 0.5% (3.9% y/y), roughly equal to the annual gains during the last three years.

A Falling Dollar: Good News or Bad News? from the Federal Reserve Bank of Atlanta can be found here.

| Import/Export Prices (NSA) | October | September | Y/Y | 2006 | 2005 | 2004 |

|---|---|---|---|---|---|---|

| Import - All Commodities | 1.8% | 0.8% | 9.6% | 4.9% | 7.5% | 5.6% |

| Petroleum | 6.9% | 4.6% | 41.4% | 20.6% | 37.6% | 30.5% |

| Non-petroleum | 0.5% | -0.2% | 3.2% | 1.7% | 2.7% | 2.6% |

| Export- All Commodities | 0.9% | 0.3% | 5.6% | 3.6% | 3.2% | 3.9% |

by Carol Stone November 9, 2007

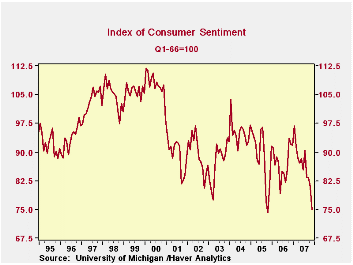

The University of Michigan's consumer sentiment index fell 5.9 points in early November to 75.0 from October's 80.9. This was a 7.3% drop, almost as large as August's 7.7%, and the fourth consecutive month without an increase. Consensus expectations in the Action Economics survey called for only a slight ease to 80.0.

Both major sub-indexes were down markedly as well. Current conditions declined from October's 97.6 to 91.0, the weakest since March 2003. Expectations fell from 70.1 to 64.7, lowest since October 2005.

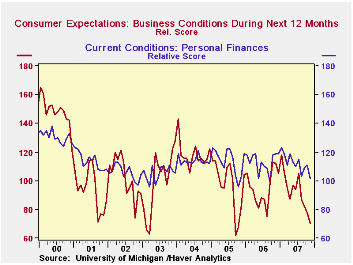

All the summary line items fell by significant amounts, ranging from 5.6%, for current buying conditions, to 10.3%, for business conditions in the next 12 months. Current personal finances were down 8.1% and expected personal finances by 7.6%. Five-year business expectations fell 7.1%.

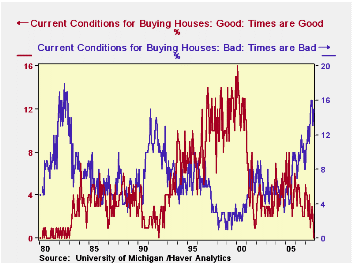

Among the survey details, those related to buying conditions for houses seem particularly relevant. The overall score for "buying conditions for houses" is 124, compared with 131 in October. This measure was 160 during the 2004 housing market peak. The overall "good time" rating eased to 61 in early November from 64 last month, while the "bad time" rating rose to 37 from 33. Readings of these respective magnitudes have prevailed for about the last 15 to 18 months, the most adverse combination since the Gulf War in late 1990/early 1991.

The survey lists reasons why this is a "good time" or a "bad time" to buy. Respondents who told the poll-takers that "times [in general] are bad" numbered 15% of the total, the highest since 1982. The number feeling that "times are good; there is prosperity" was zero. This reading has never been very high, with a peak of 16 in early 2000, just as the stock market was reaching a peak. But readings of zero have also been rare: early 1992 and the double-digit inflation/interest rate/recession period from 1980 to 1982. One favorable note came in the item home "prices are low; there are good deals"; 52% of respondents believe this is true. Perhaps there's the seed of some recovery in that.

The University of Michigan survey is not seasonally adjusted.The reading is based on telephone interviews with about 500 households at month-end; the mid-month results are based on about 300 interviews. The summary indexes are in Haver's USECON database, with details in the proprietary UMSCA database.

| University of Michigan | Nov (Prelim) | Oct | Sept | Nov y/y | 2006 | 2005 | 2004 |

|---|---|---|---|---|---|---|---|

| Consumer Sentiment | 75.0 | 80.9 | 83.4 | -18.6% | 87.3 | 88.5 | 95.2 |

| Current Conditions | 91.0 | 97.6 | 97.9 | -14.2% | 105.1 | 105.9 | 105.6 |

| Expectations | 64.7 | 70.1 | 74.1 | -22.2% | 75.9 | 77.4 | 88.5 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief