Global| May 11 2007

Global| May 11 2007U.S. Retail Sales: Weak in April but Stronger in March

Summary

Result: Surprising - good growth in Q2. Retail sales fell by 0.2% in April the first month of the second quarter yet sales in Q2 are up nicely so far. How can that be? The reason is that for GDP we look at what happens in quarter on [...]

Result: Surprising - good growth in Q2.

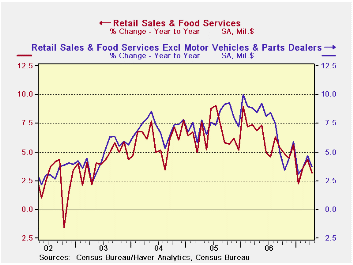

Retail sales fell by 0.2% in April the first month of the second quarter… yet sales in Q2 are up nicely so far. How can that be? The reason is that for GDP we look at what happens in quarter on average. And in Q1 sales got stronger as the quarter went on. So, in March, the month of the quarter sales were well above the Q1 average. The small drop in sales in April therefore leaves sales growing in Q2. The growth rate for nominal sales in the quarter so far is 3.7% for overall sales. Taking out vehicle sales raises that to 5.5%. With vehicle and gasoline station sales removed the rise is 2.7%. While the 2.7% figure seems weak with gas station sales out of the total, most of the energy is removed so that comes much closer to being a real sales figure.On balance Q2 is off to a reasonably good start. The early Easter packed sales into March by sucking them out of April. But on balance we are still in good shape in Q2. Trends are moderately lower, but only moderately (see graph).

Clothing sales were weak in the month and are weak over the past three months with a three-month growth rate of -6.1% annualized. General merchandise is weak in that same way. But nondurables excluding gasoline sales are up at a 5.5% pace over three months and remain at a very steady pace (see table below). Durables spending was weak in the quarter on weakness in vehicle sales (-1%) and weakness in building materials (-2.3%) while furniture and electronics sales were up (1%) over three months. Durables sales are dropping, but only at a -0.6% annual rate. Year/year durables sales are flat due to the on-again off-again nature of vehicle sales and ongoing weakness in building materials. The weakness in building materials shows no sign of letting up.

| Retailing: | Mo/Mo | Seasonally Adjusted Annual Rate | |||

| Totals | Apr 2007 | 3-Mo | 6-Mo | Yr/Yr | Year Ago: Y/Y |

| Retail & Food Service | -0.2% | 5.3% | 5.6% | 3.2% | 6.8% |

| Retail Excl Motor Vehicles & Parts | 0.0% | 6.6% | 7.0% | 3.7% | 8.4% |

| Retail Excl Motor Vehicles & Parts & Gasoline |

-0.2% | 3.9% | 4.3% | 4.0% | 7.4% |

| Retailing: | Mo/Mo | Seasonally Adjusted Annual Rate | |||

| Durables | Apr 2007 | 3-Mo | 6-Mo | Yr/Yr | Year Ago: Y/Y |

| Total Durables | -1.0% | -0.6% | 0.9% | 0.0% | 5.0% |

| Building Materials | -2.3% | -7.7% | -2.9% | -6.0% | 14.0% |

| Motor Vehicles & Parts | -1.0% | 0.8% | 0.7% | 1.3% | 1.2% |

| Motor Vehicles Dealers | -0.9% | 0.8% | 1.0% | 1.4% | 1.0% |

| Furniture, Electronics | 1.0% | 5.0% | 7.6% | 4.9% | 7.8% |

| Retail | Mo/Mo | Seasonally Adjusted Annual Rate | |||

| Nondurables | Apr 2007 | 3-Mo | 6-Mo | Yr/Yr | Year Ago: Y/Y |

| Total Nondurables | 0.2% | 8.5% | 8.2% | 4.8% | 7.8% |

| Food & Beverages | 0.5% | 8.2% | 5.1% | 6.6% | 4.0% |

| Health | 0.9% | 8.7% | 5.7% | 8.1% | 6.0% |

| Gasoline | 1.7% | 29.2% | 30.0% | 1.5% | 16.3% |

| Clothing | -2.0% | -6.1% | 3.2% | 4.7% | 5.2% |

| Sport Goods | -0.8% | 9.5% | 4.0% | 0.1% | 6.9% |

| General Merchandise | -1.2% | -1.3% | 4.3% | 3.1% | 6.2% |

| Non-Store Retailers | 1.8% | 22.5% | 10.7% | 9.3% | 10.9% |

| Miscellaneous Retail | 0.4% | 8.7% | 5.7% | 8.1% | 6.0% |

| Nondurables Excl Gasoline | -0.1% | 5.5% | 5.1% | 5.4% | 6.5% |

| Services | |||||

| Food Service & Drinking | -0.1% | 2.0% | 3.7% | 4.9% | 7.4% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief