Global| Jun 06 2007

Global| Jun 06 2007U.S. Productivity is Down and Unit Labor Costs are Up

Summary

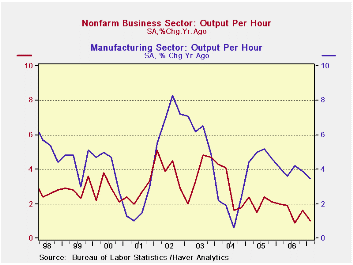

Productivity is trending lower for manufacturing (MFG) as well as overall for nonfarm businesses. The accompanying chart makes the downturn clear. For nonfarm business the erosion seems to date back to mid-2005. For nonfarm [...]

Productivity is trending lower for manufacturing (MFG) as well as overall for nonfarm businesses. The accompanying chart makes the downturn clear. For nonfarm business the erosion seems to date back to mid-2005. For nonfarm productivity it looks like a trend decline is still in train - that would be very bad news indeed. It’s bad enough that productivity has slowed to 1% Yr/Yr.

With productivity at 1% Yr/Yr and population growth at about 1% Yr/Yr, GDP growth faces strong constraints. While labor force growth can surpass population growth, one-half of one percent is about all the extra growth it might be prudent to look for. And to encourage greater labor force participation it generally takes higher wages and that would be a problem for the Fed since it is trying to keep inflation contained. On balance, 2.5% growth seems about the limit to GDP under this new productivity growth rate scenario.

Of course productivity is a fickle series. The chart on the left shows a good deal of variation in Yr/Yr growth. Quarterly growth in productivity and GDP can move around by a lot more. Still it is the trend we should be most concerned with. That is what the Fed will be looking at as it makes an assessment of its own policy options.

The main implication of structurally weaker productivity growth is that the Fed will be seeing the economy with a lower speed limit. This is something markets have been having a hard time dealing with for sometime now. We have seen the slowing in labor force growth that has meant that 118K jobs per month (in nonfarm payrolls) is all that the job market needs to produce to steady the unemployment rate. Now a lower GDP number will also associate with that weaker job growth.

The paradox is that this low growth will not be a cause for alarm that growth is slipping, rather the Fed will get worried about inflation pressures and speeding at growth rates that used to be quite acceptable and sustainable.

Productivity is one of the most important contributors to growth and it is one of the most volatile. As such it is a variable that is hard to pin down. Even so the Fed will not be pleased with the new result and the trend it hints at.

A diminished trend in productivity means that wage pressures can become inflation problems more easily. With high productivity in train sizeable wage increases can be blunted and ‘paid for’ by accelerated productivity growth. But when productivity growth is low, firms have to be more careful about giving in to wage demands since the productivity cushion is smaller.

In Q1 2007 compensation per hour of 3.2% less productivity of 1% leaves unit labor costs higher by 2.2%. In Q4 of 2005 compensation per hour of 3.7% translated into unit labor costs of just +1.5% because productivity was up by 2.1%.

With the Fed putting the top of its inflation comfort zone at 2% in terms of Core PCE it is easy to see that wages are to be held in a narrow band if productivity stays this low and if the Fed is to be successful in keeping inflation at bay.

| Year/Year Pct | 07/Q1 | 06/Q4 | 06/Q3 | 06/Q2 | 06/Q1 | 05/Q4 |

| NF Unit Labor Cost | 2.2% | 4.0% | 2.6% | 3.1% | 3.6% | 1.5% |

| NF Output/Hr | 1.0% | 1.6% | 0.9% | 1.9% | 2.0% | 2.1% |

| NF Comp/Hr | 3.2% | 5.6% | 3.5% | 5.1% | 5.7% | 3.7% |

| NF Real Comp/Hr | 0.7% | 3.6% | 0.1% | 1.0% | 1.9% | 0.0% |

| Manufacturing | ||||||

| MFG Unit Labor Cost | -0.4% | 0.7% | -2.3% | 0.1% | 2.0% | -1.2% |

| MFG Output/Hour | 3.5% | 3.9% | 4.2% | 3.6% | 4.1% | 4.6% |

| MFG Comp/Hour | 3.1% | 4.6% | 1.8% | 3.7% | 6.1% | 3.4% |

| MFG Real Comp/Hour | 0.6% | 2.6% | -1.5% | -0.3% | 2.3% | -0.4% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief