Global| May 14 2009

Global| May 14 2009U.S. PPI Firms With Higher Food Prices, Core Price Gains Still Trending Lower

by:Tom Moeller

|in:Economy in Brief

Summary

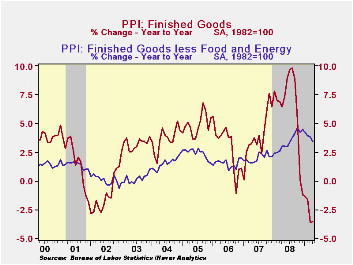

U.S. producer prices for finished goods rose 0.3% last month following their 1.2% downdraft during March. The latest rise outpaced Consensus expectations for a 0.1% uptick. It did not, however, represent a broad-based firming of the [...]

U.S.

producer prices for finished goods rose 0.3% last month following their

1.2% downdraft during March. The latest rise outpaced Consensus

expectations for a 0.1% uptick. It did not, however, represent a

broad-based firming of the recent weakness in pricing power. In fact

pricing power was very limited. · Finished food prices jumped

1.5% m/m led by firm gains in beef (-4.2% y/y) & vegetable

(1.3% y/y) prices as well as a notable 43.7% surge in egg prices (-4.0%

y/y). That surge was, however, just recovering declines during the

prior two months.

U.S.

producer prices for finished goods rose 0.3% last month following their

1.2% downdraft during March. The latest rise outpaced Consensus

expectations for a 0.1% uptick. It did not, however, represent a

broad-based firming of the recent weakness in pricing power. In fact

pricing power was very limited. · Finished food prices jumped

1.5% m/m led by firm gains in beef (-4.2% y/y) & vegetable

(1.3% y/y) prices as well as a notable 43.7% surge in egg prices (-4.0%

y/y). That surge was, however, just recovering declines during the

prior two months.

Energy prices ticked 0.1% lower (-25.2% y/y) after their 5.5% decline during March. Finished gasoline prices rose 2.6% which reversed just a piece of a 13.1% decline in March (-46.7% y/y). That monthly increase was offset, however, by a 6.2% decline in natural gas prices (-18.1% y/y).

Prices of core finished consumer goods rose

another 0.2%.  The gain

left the y/y increase at a respectable 3.8% but

the trend has been moving lower since the end of last year. Durable

consumer goods prices increased 0.3% after having been unchanged during

March but, here again, the trend rate of gain has eased. On a

three-month basis prices have risen at a 2.0% annual rate versus a 6.4%

rise last October. The three-month gain in core nondurable goods prices

also has eased to 3.4% (AR), half the peak rate of increase last fall.

Finally, capital equipment prices have started to fall. The April

decline of 0.1% added to a 0.2% March drop and that was enough to pull

the three-month change negative versus a 5%+ rate of increase as of

last fall.

The gain

left the y/y increase at a respectable 3.8% but

the trend has been moving lower since the end of last year. Durable

consumer goods prices increased 0.3% after having been unchanged during

March but, here again, the trend rate of gain has eased. On a

three-month basis prices have risen at a 2.0% annual rate versus a 6.4%

rise last October. The three-month gain in core nondurable goods prices

also has eased to 3.4% (AR), half the peak rate of increase last fall.

Finally, capital equipment prices have started to fall. The April

decline of 0.1% added to a 0.2% March drop and that was enough to pull

the three-month change negative versus a 5%+ rate of increase as of

last fall.

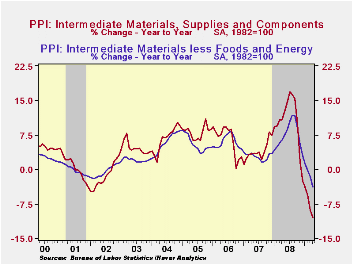

Falling again were prices for intermediate goods and that should foreshadow even lower finished goods prices. Intermediate goods prices dropped another 0.5% pulling the year-to-year change to still another record rate of decline of 10.4%. Excluding food & energy prices continued to move lower, last month by 0.9% which was their seventh monthly decline. Pricing here has been so weak that the 3.8% y/y decline was a record drop for the series which dates back to 1974.

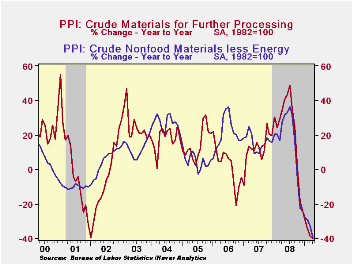

The crude

materials PPI prices rose for the first

month since last summer. The modest 3.0% rise reflected higher food

prices which still are down a sharp 18.7% y/y. Core pricing power

continued to reflect the weak economy and prices fell 0.6%. They

remained down by more than one-third versus last year due to lower

metals and chemicals prices.

The crude

materials PPI prices rose for the first

month since last summer. The modest 3.0% rise reflected higher food

prices which still are down a sharp 18.7% y/y. Core pricing power

continued to reflect the weak economy and prices fell 0.6%. They

remained down by more than one-third versus last year due to lower

metals and chemicals prices.

The Producer Price Index data is available in Haver's USECON database. More detailed data is in the PPI and in the PPIR databases.

Rethinking the Implications of Monetary Policy: How a Transactions Role for Money Transforms the Predictions of Our Leading Models from the Federal Reserve Bank of Philadelphia can be found here.

| Producer Price Index (%) | April | March | Y/Y | 2008 | 2007 | 2006 |

|---|---|---|---|---|---|---|

| Finished Goods | 0.3 | -1.2 | -3.5 | 6.4 | 3.9 | 2.9 |

| Core | 0.1 | 0.0 | 3.4 | 3.4 | 2.0 | 1.5 |

| Intermediate Goods | -0.5 | -1.5 | -10.4 | 10.5 | 4.0 | 6.4 |

| Core | -0.9 | -0.3 | -3.8 | 7.6 | 2.8 | 6.0 |

| Crude Goods | 3.0 | -0.3 | -39.9 | 21.2 | 11.9 | 1.4 |

| Core | -0.6 | -1.6 | -39.7 | 15.0 | 15.6 | 20.8 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief