Global| Jun 26 2009

Global| Jun 26 2009U.S. Personal Income Surge Lifts Savings Rate To Its Highest Since 1993

by:Tom Moeller

|in:Economy in Brief

Summary

The economic recession continued to damp growth in wages last month, but "automatic stabilizers" kicked in to pick the slack. The result was a 1.4% jump in May personal income which was the largest monthly increase in a year. The rise [...]

The economic recession continued to damp growth in wages last

month, but "automatic stabilizers" kicked in to pick the slack. The

result was a 1.4% jump in May personal income which was the largest

monthly increase in a year. The rise owed to an 8.0% jump (12.2% y/y)

in government payments which included a 3.5% (190.4% y/y) surge in

unemployment insurance benefits and a 21.0% jump in "other" payments.

As might be expected given the recession, these gains offset severe

weakness in the income earned in the private sector. Wages &

salaries slipped 0.1% (-1.1% y/y) for the eighth decline in the last

nine months. In addition, the decline in interest rates took its toll

on interest income which in May was off 5.5% y/y while the corporate

sector paid fewer dividends (-5.2% y/y) as earnings fell.

Lower taxes added further to the income gains fueled by direct payments from the government. Tax payments were down nearly 20% since December. That lifted disposable personal income at a 10.8% annual rate so far this year and by 1.6% just during last month. Adjusted for inflation, real disposable income also has been quite firm and posted a 1.6% increase last month and is up at a 9.0% annual rate since December

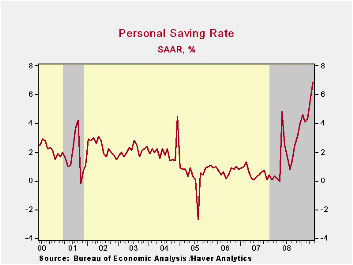

With the recession, consumers have entered a cautious mode and they're letting the income gains rebuild their balance sheets. As a result the personal savings rate jumped again, last month to 6.9% which was the highest level since December of 1993.

Spending restraint was evidenced by the slight 0.3% rise in

May personal consumption expenditures. That followed no change during

April which was slightly better than a 0.1% decline reported last

month. Adjusted for low inflation, May spending rose 0.2%. However, the

1.9% year-to-year retrenchment in real spending was near the fastest

rate at which spending has ever been bulled back. The good news is that

consumers seem to have grown tired of not spending. So far this year

real personal consumption has risen at a 1.5% annual rate.

The consumption details may suggest, however, that the idea of a stabilization still may be a stretch. Real spending on motor vehicles seems to stabilizing and rose 2.4% last month (-16.4% y/y) and it's actually up at a 4.3% annual rate since December. Real spending on furniture & appliances also seems to be stabilizing though it's still down -5.6% y/y. Real spending on apparel made up for an April decline with a 0.2% increase (-7.4% y/y). Spending on services again was roughly unchanged (0.9% y/y).

Finally, all this spending restraint held back the PCE chain price index to a 0.1% uptick. The gain matched the rise in core prices and the annual rate of increase dropped to 1.8%. The latest increase in prices matched Consensus expectations.

The personal income & consumption figures are available in Haver's USECON and USNA databases.

| Disposition of Personal Income (%) | May | April | Y/Y | 2008 | 2007 | 2006 |

|---|---|---|---|---|---|---|

| Personal Income | 1.4 | 0.7 | 0.3 | 3.8 | 6.1 | 7.1 |

| Disposable Personal Income | 1.6 | 1.3 | 0.2 | 4.6 | 5.5 | 6.4 |

| Personal Consumption Expenditures | 0.3 | 0.0 | -1.8 | 3.6 | 5.5 | 5.9 |

| Saving Rate | 6.9 | 5.6 | 4.8 (May '08) | 1.8 | 0.5 | 0.7 |

| PCE Chain Price Index | 0.1 | 0.1 | 0.1 | 3.3 | 2.6 | 2.8 |

| Less food & energy | 0.1 | 0.3 | 1.8 | 2.2 | 2.2 | 2.3 |

by Robert Brusca June 26, 2009

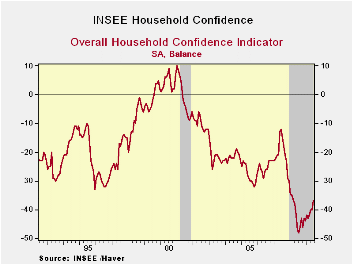

Consumer confidence in France has risen in three of the last

for months with one month marking a pause in the rising trend. French

confidence hit its low point in July of 2008 at a level of -48. Since

then although the recession has worsen in most of the world, French

consumer confidence has embarked on a rising trend that has extended

its trend rise during this whole period of economic malaise.

This is probably one reason that France has weathered the

recession better than other European countries. Another reason being,

of course, that French fiscal spending has been greater, and today we

are hearing some misgivings about the size of the French fiscal

deficit. French Prime Minister Francois Fillon warned on Friday that

budget deficits "could compromise even the survival of our economic

systems if we do not manage to control them."

Confidence is still in the lower 19% of its range since 1990.

By count, confidence has been weaker than this only 6.4% of the time.

So the range reading is more comforting than it should be.

Consumer concern about unemployment is the highest it has

been. Still the outlook for living standards in the 12 months ahead is

in its 17th range percentile compared to a standing of 9% over the past

21 months. Both figures however have been worse only 5.6% of the time.

In that sense there is not improvement in the outlook.

Only about 25% say the time is right for a major purchases;

the response is worse than that only 15% of the time.

On balance the good news is that the French figures show some

improvement. But let’s not kid ourselves; the readings are still

painfully weak. Europe’s leaders should not be counting their chickens

before they are hatched. There is still a lot of risk out there. In

response to a question about European recovery, European Commissioner

for Economic and Monetary Affairs Joaquin Almunia said Friday. "We are

not there. The U.S. Economy is starting to give signals that it is near

to or at the beginning of a recovery." Even though the US is in the

lead no one is ‘there’ yet. And there is no room for complacency. Maybe

the US congress should be more concerned with doing things to aid

recovery than to find itself a scapegoat for an economy gone bad and

stimulus monies (it approved) less than well spent.

| INSEE Household Monthly Survey | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Since Jan 1990 | Since Jan 1990 | |||||||||

| Jun 09 |

May 09 |

Apr 09 |

Mar -09 |

Percentile | Rank % | Max | Min | Range | Mean | |

| Household Confidence | -37 | -40 | -40 | -42 | 19.0 | 6.4 | 10 | -48 | 58 | -19 |

| Living Standards | ||||||||||

| Past 12 Mos | -73 | -75 | -75 | -76 | 9.0 | 5.6 | 18 | -82 | 100 | -40 |

| Next 12-Mos | -47 | -50 | -53 | -58 | 17.1 | 5.6 | 16 | -60 | 76 | -21 |

| Unemployment: Next 12 | 96 | 89 | 84 | 79 | 100.0 | 99.6 | 96 | -37 | 133 | 31 |

| Price Developments | ||||||||||

| Past 12Mo | -24 | -18 | -12 | -7 | 27.3 | 48.3 | 64 | -57 | 121 | -16 |

| Next 12-Mos | -53 | -55 | -53 | -51 | 7.5 | 3.4 | 33 | -60 | 93 | -34 |

| Savings | ||||||||||

| Favorable to save | 9 | 7 | 10 | 14 | 33.3 | 7.3 | 39 | -6 | 45 | 22 |

| Ability to save Next 12 | -18 | -20 | -15 | -13 | 17.2 | 6.4 | 6 | -23 | 29 | -9 |

| Spending | ||||||||||

| Favorable for major purchase | -27 | -28 | -30 | -29 | 25.9 | 15.4 | 16 | -42 | 58 | -14 |

| Financial Situation | ||||||||||

| Current | 12 | 12 | 12 | 12 | 42.9 | 57.3 | 24 | 3 | 21 | 12 |

| Past 12 MOs | -23 | -28 | -26 | -28 | 43.8 | 17.9 | -5 | -37 | 32 | -17 |

| Next 12-Mos | -13 | -16 | -17 | -20 | 31.4 | 8.1 | 11 | -24 | 35 | -1 |

| Number of observations in the period 234 | ||||||||||

by Tom Moeller June 26, 2009

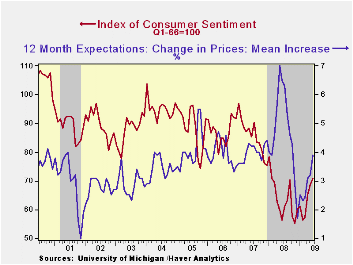

Though the overall economy has yet to make a convincing turn

towards the better, the University of Michigan's June reading of

consumer sentiment suggests a coming improvement in retail spending.

The full-month index level rose slightly to 70.8, an improvement from

the mid-month reading and up sharply from the November low. The figure

was better than Consensus expectations for a reading of 69.0. Indeed,

spending improvement is suggested since during the last ten years,

there has been a 61% correlation between the level of sentiment and the

growth in real spending during the next five months.

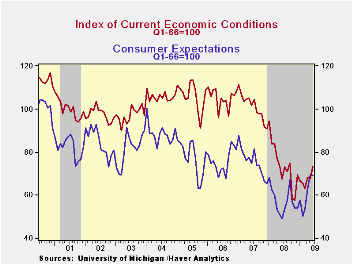

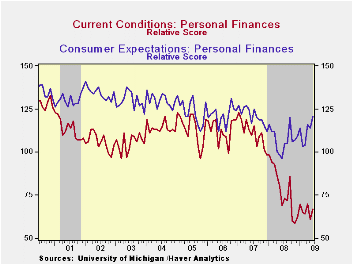

The current economic conditions jumped ten percent from May to its highest level since last September. The reading for current personal finances just about made up the May decline. however, it was the jump in the reading of current conditions for buying large household goods to the highest level since March of last year that powered the increase. Showing a huge increase was the reading of current conditions for buying a motor vehicle. Though conditions for buying a house slipped, the level remained up sharply from last year.

The expectations component of the index improved from the mid-month reading and was up by nearly half versus a year earlier. Expectations for personal finances jumped with higher stock prices. Though expected business conditions during the next year slipped, they remained up sharply from last year. Expected conditions during the next five years also slipped versus May but they were up sharply from one year ago.

The read of current conditions, conversely, deteriorated from

mid-month but remained off its winter low. Buying conditions for large

household goods were at their highest level since early last year but

personal finances were viewed as flat.

The opinion of government policy, which may eventually influence economic expectations, fell this month after having jumped through May. It remained near the highest level since 2002. A reduced 24% of respondents thought that a good job was being done by government while 28% thought that a poor job was being done. Nevertheless, despite these monthly changes, the trend is still very much toward a favorable reading of policy actions.

Inflation expectations for the next year rose further to 3.9%. That compares to a low of 1.7% last December but remained down from a reading which was as high as 7.0% last May.

The University of Michigan survey data is not seasonally adjusted. The reading is based on telephone interviews with about 500 households at month-end; the mid-month results are based on about 300 interviews. The summary indexes are in Haver's USECON database with details in the proprietary UMSCA database.

Inflation and Monetary Policy from the Federal Reserve Bank of Richmond can be found here.

The State of our Interstates from the Federal Reserve Bank of Chicago is available here.

| University of Michigan | June (Final) | Mid-June | May | April | June y/y | 2008 | 2007 | 2006 |

|---|---|---|---|---|---|---|---|---|

| Consumer Sentiment | 70.8 | 69.0 | 68.7 | 65.1 | 25.5% | 63.8 | 85.6 | 87.3 |

| Current Conditions | 73.2 | 74.5 | 67.7 | 68.3 | 8.3 | 73.7 | 101.2 | 105.1 |

| Expectations | 69.2 | 65.4 | 69.4 | 63.1 | 40.7 | 57.3 | 75.6 | 75.9 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief