Global| Oct 01 2009

Global| Oct 01 2009U.S. Personal Income GrowsModestly; PCE Raised By "Cash-for-Clunkers"

by:Tom Moeller

|in:Economy in Brief

Summary

Personal income in August continued to increase at its modest July rate. The 0.2% rise followed a 0.2% gain which was revised from 0.1%. Consensus forecasts were for a 0.1% uptick. These weak increases wholly reflect the current [...]

Personal

income in August continued to increase at its modest July

rate. The 0.2% rise followed a 0.2% gain which was revised

from 0.1%. Consensus forecasts were for a 0.1% uptick. These weak

increases wholly reflect the current recession. Year-to-year income

growth fell 2.6% during the last twelve months after a 2.9% increase

last year.

Personal

income in August continued to increase at its modest July

rate. The 0.2% rise followed a 0.2% gain which was revised

from 0.1%. Consensus forecasts were for a 0.1% uptick. These weak

increases wholly reflect the current recession. Year-to-year income

growth fell 2.6% during the last twelve months after a 2.9% increase

last year.

The dismal job market accounts for this year's negative income growth. Wages & salaries rose modestly m/m during July and August. However, these latest gains were not enough to lift wages yr-to-yr which fell 5.2% after a 2.1% 2008 increase. Wages in the factory sector fell 11.6% y/y while service sector wages fell 5.4%. To a limited extent these declines were offset by a 3.6% increase in government sector earnings.

Unemployment insurance payments picked up just some of the slack in the job market and rose 4.4% during August. That lifted payments to $136.9B versus $60.4B during August of last year. Interest income continued to show the effects of lower rates and fell 6.9% y/y while dividend income fell by one-quarter as corporate profits dried up.

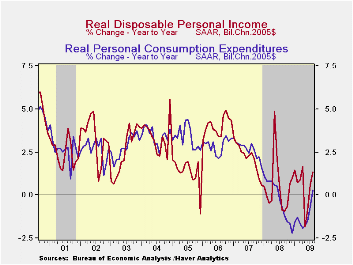

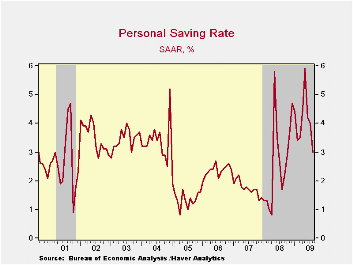

Disposable

personal

income increased just 0.1% following a slight decline during

July. Adjusted for inflation, real disposable income slipped for the

third straight month, although only by 0.2% during August and by 0.1%

in July. Real disposable income growth of 1.3% y/y was lifted by tax

cuts earlier this year. The saving rate fell again with the weakness in

income growth. The decline to 3.0% contrasted with a May peak of 5.9%.

Nevertheless, the rate remained up slightly from last year and double

the 2007 level.

Disposable

personal

income increased just 0.1% following a slight decline during

July. Adjusted for inflation, real disposable income slipped for the

third straight month, although only by 0.2% during August and by 0.1%

in July. Real disposable income growth of 1.3% y/y was lifted by tax

cuts earlier this year. The saving rate fell again with the weakness in

income growth. The decline to 3.0% contrasted with a May peak of 5.9%.

Nevertheless, the rate remained up slightly from last year and double

the 2007 level.

Personal spending showed the full

effect of the "cash-for-clunkers" program for new motor vehicle

purchases. It lifted durables spending by 5.3% (-1.3% y/y) with a 13.3%

gain (6.6% y/y) for autos. Spending on nondurables rose just 2.3%

(-5.3% y/y) as outlays on apparel continued down by 3.8% versus last

year. Spending on furniture continued quite weak and fell 7.7% versus

last year.  Outlays on services increased 0.4% (1.7% y/y) as spending on

health care continued quite strong and posted a 5.2% gain versus last

year. Spending in restaurants and on recreation remained negative.

Outlays on services increased 0.4% (1.7% y/y) as spending on

health care continued quite strong and posted a 5.2% gain versus last

year. Spending in restaurants and on recreation remained negative.

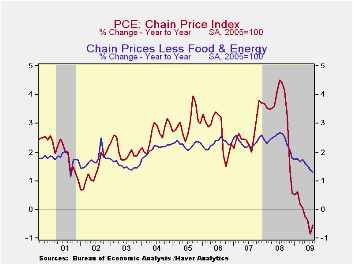

Prices increased 0.3% during August reflecting an 8.4% rise (-30.5% y/y) in gasoline costs and another rise is in store for September. Nevertheless, the PCE chain price index still was down by 0.5% versus last year. Less food-and-energy, "core" prices were again quite tame and posted their fourth consecutive 0.1% increase. Goods prices rose 0.7% (-3.6% y/y while prices for services increased just 1.0% y/y.

The personal income & consumption figures are available in Haver's USECON and USNA databases.

Yesterday's speech titled Central Bank Exit Policies by Vice Chairman Donald L. Kohn can be found here.

| Disposition of Personal Income (%) | August | July | June | Y/Y | 2008 | 2007 |

|---|---|---|---|---|---|---|

| Personal Income | 0.2 | 0.2 | -1.1 | -2.6 | 2.9 | 5.6 |

| Disposable Personal Income | 0.1 | -0.0 | -1.1 | 0.8 | 3.9 | 4.9 |

| Personal Consumption Expenditures | 1.3 | 0.3 | 0.7 | -0.3 | 3.1 | 5.4 |

| Saving Rate | 3.0 | 4.0 | 4.2 | 1.7 (Aug. '08) | 2.6 | 1.7 |

| PCE Chain Price Index | 0.3 | 0.0 | 0.5 | -0.5 | 3.3 | 2.7 |

| Less food & energy | 0.1 | 0.1 | 0.1 | 1.3 | 2.4 | 2.4 |

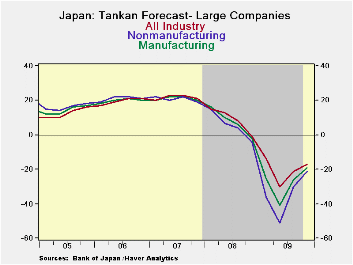

Japan's Tankan Shows Up-Swing... And Less

by Robert Brusca October 01, 2009

Yes, Japan’s Tankan survey has legs and the rise in the

various large company Tankan indices is ongoing. There is somewhat less

vigor in the rise of the future improvement expected but it is still

advancing at a solid pace and the current situation has improved more

rapidly. The fly in the ointment this quarter is that despite ‘improved

confidence’ the plans for capital expenditure have been cut back. In

the end that casts some doubt about the rise in confidence itself.

Firms with profits still under pressure are acting to conserve cash

instead of aggressively re-deploying themselves for growth ahead. That

kind of behavior could help to torpedo recovery even as survey

respondents say that things are getting better.

The table above shows that manufacturing, wholesaling and personal

services are best sectors in terms of the percentile standing of their

respective indices. Even so these sectors are in the bottom 30th

percentile of their respective ranges or lower. Non MFG as a whole is

in the bottom 13 percentile of its range. Manufacturing’s outlook, at a

raw reading of -21, is in the 41st percentile of its range. That is

somewhat better, than the current assessment but still far from good.

Medium sized firms assess their MFG index as in the 23rd percentile of

its ranges for small enterprises it is much worse as they stand in the

bottom 7th percentile of their range. The nonMFG percentiles for the

medium and small enterprises are comparable to the Tankan Large Company

readings for Non MFG – very weak.

Yes Japan has made progress. But the current state of business is still

poor even though it has improved. While the expected improvement is at

a slightly better level than the assessment of current conditions,

firms continue to react to the recession instead of planning ahead for

recovery. As a result, one of the great forces of recovery has yet to

be unleashed- optimism. Japan’s recovery remains cautiously guarded and

in the end that will be a drag on its momentum. Until firms see the

need to invest for the future and as long as they cut and hack at

existing spending plans the look will remain touch and go.

| Tankan Results Large Enterprises | |||||||

|---|---|---|---|---|---|---|---|

| Readings | Averages | PERCENTILES | |||||

| Q3-09 | Q2-09 | Q1-09 | Q4-08 | 1-Y Avg | Since Q3'03 | Since Q1'04 | |

| MFG | -33.0 | -48.0 | -58.0 | -24.0 | -40.5 | 5.3 | 29.8% |

| NonMFG | -24.0 | -29.0 | -31.0 | -9.0 | -26.5 | 7.8 | 13.2% |

| Total Industry | -28.0 | -39.0 | -45.0 | -16.0 | -33.5 | 6.5 | 25.0% |

| Construction | -23.0 | -29.0 | -27.0 | -10.0 | -26.0 | -5.9 | 18.2% |

| Real Estate | -11.0 | -24.0 | -21.0 | -7.0 | -17.5 | 24.3 | 16.9% |

| Wholesale | -29.0 | -41.0 | -44.0 | -7.0 | -35.0 | 8.2 | 22.1% |

| Retail | -32.0 | -39.0 | -42.0 | -18.0 | -35.5 | -0.9 | 17.2% |

| Transportation | -35.0 | -43.0 | -46.0 | -7.0 | -39.0 | 5.8 | 15.7% |

| Services 4 Biz | -22.0 | -30.0 | -21.0 | -1.0 | -26.0 | 15.2 | 11.9% |

| Personal Serv | -4.0 | -11.0 | -9.0 | -11.0 | -7.5 | 7.1 | 23.3% |

| Restaurants & Hotels | -50.0 | -46.0 | -45.0 | -32.0 | -48.0 | -3.3 | 0.0% |

| Forecast | |||||||

| Q4-09 | Q3-09 | Q2-09 | Q1-09 | 1-Y Avg | Since Q3'03 | Since Q1'04 | |

| MFG-OtLk | -21.0 | -30.0 | -51.0 | -36.0 | -34.5 | 5.8 | 41.1% |

| NonMFG -Otlk | -17.0 | -21.0 | -30.0 | -14.0 | -20.5 | 8.4 | 24.5% |

| All Industry-Otlk | -19.0 | -26.0 | -41.0 | -25.0 | -27.8 | 7.0 | 34.9% |

| Tankan Results Medium Enterprises | |||||||

| Q3-09 | Q2-09 | Q1-09 | 1-Y Avg | 1-Y Avg | Since Q3'03 | Since Q1'04 | |

| MFG | -40.0 | -55.0 | -57.0 | -44.0 | -44.0 | -7.8 | 23.0% |

| NonMFG | -30.0 | -36.0 | -37.0 | -31.0 | -31.0 | -8.9 | 15.6% |

| Forecast | |||||||

| Q4-09 | Q3-09 | Q2-09 | Q1-09 | 1-Y Avg | Since Q3'03 | Since Q1'04 | |

| MFG-OtLk | -35.0 | -46.0 | -61.0 | -45.0 | -46.8 | -9.1 | 34.7% |

| NonMFG -Otlk | -28.0 | -32.0 | -45.0 | -32.0 | -34.3 | -10.5 | 32.7% |

| All Industry-Otlk | -31.0 | -39.0 | -51.0 | -38.0 | -39.8 | -10.1 | 32.8% |

| Tankan Results Small Enterprises | |||||||

| Q4-09 | Q3-09 | Q2-09 | Q1-09 | 1-Y Avg | Since Q3'03 | Since Q1'04 | |

| MFG | -52.0 | -57.0 | -57.0 | -54.5 | -54.5 | -15.0 | 7.5% |

| NonMFG | -39.0 | -44.0 | -42.0 | -41.5 | -41.5 | -20.2 | 13.2% |

| Total Industry | -39.0 | -44.0 | -42.0 | -41.5 | -41.5 | -20.2 | 12.2% |

| Forecast | |||||||

| Q4-09 | Q3-09 | Q2-09 | Q1-09 | 1-Y Avg | Since Q3'03 | Since Q1'04 | |

| MFG-OtLk | -44.0 | -53.0 | -63.0 | -48.0 | -52.0 | -16.2 | 26.4% |

| NonMFG -Otlk | -40.0 | -45.0 | -52.0 | -42.0 | -44.8 | -23.9 | 27.3% |

| All Industry-Otlk | -41.0 | -48.0 | -56.0 | -44.0 | -47.3 | -21.1 | 27.8% |

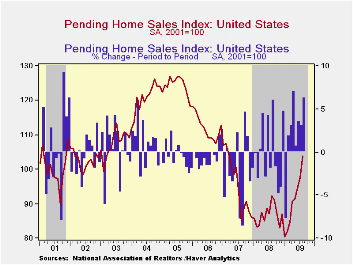

U.S. Pending Home Sales Climb Another 6.4% in August

by Carol Stone October 1, 2009

Housing

demand continues to improve. The National Association of Realtors (NAR)

reported that during August, pending home sales increased 6.4%, notably

stronger than June's 3.6% and July's 3.2% gains. NAR's index

stood at 103.8, the highest since March 2007; the index base is

2001=100.

Housing

demand continues to improve. The National Association of Realtors (NAR)

reported that during August, pending home sales increased 6.4%, notably

stronger than June's 3.6% and July's 3.2% gains. NAR's index

stood at 103.8, the highest since March 2007; the index base is

2001=100.

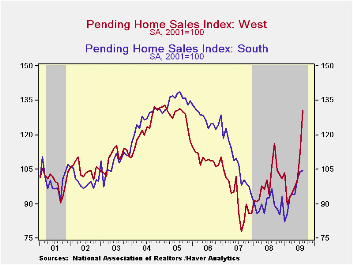

In this report, all four regions of the

country participated in the firming sales pattern. The West

led again, with a whopping 16.0% jump. This is a

monthly rate; you can annualize it, if you like, and see a really

eye-popping figure. The sales index there was 130.5; its

all-time high in the West is 133.0 in February 2005. This

upturn in sales has been helped by weak house prices, but as noted

elsewhere on these pages recently, these prices have started to firm;

while there are no price data with this report, NAR's tally of sales

closed in August showed an outright increase in prices in the West of

1.3%; since an apparent trough in April, these prices have risen a

total of 8.6%.

This

upturn in sales has been helped by weak house prices, but as noted

elsewhere on these pages recently, these prices have started to firm;

while there are no price data with this report, NAR's tally of sales

closed in August showed an outright increase in prices in the West of

1.3%; since an apparent trough in April, these prices have risen a

total of 8.6%.

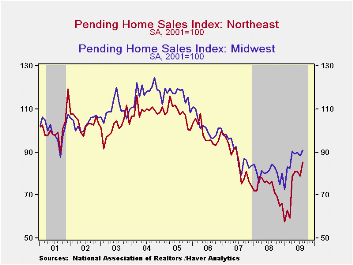

Elsewhere, sales advanced 8.2% in the Northeast, and at 85.3, this index is up 47.6% since the low there in January. In the Midwest, sales gained 3.1% in August, and they are 25.1% above their low, also in January. Sales in the South just barely edged higher, 0.8%, but they have risen more in prior months, so that they are now 27.3% above their January trough.

These

home sales figures are analogous to the new home sales data from the

Commerce Department in that they measure existing home sales when the

sales contract is signed, not at the time the sale is closed. The

series dates back to 2001.

These

home sales figures are analogous to the new home sales data from the

Commerce Department in that they measure existing home sales when the

sales contract is signed, not at the time the sale is closed. The

series dates back to 2001.

The pending home sales data are available in Haver's PREALTOR database. The number of homes on the market and prices are in the REALTOR database.

| Pending Home Sales (2001=100) | August | July | June | Y/Y | 2008 | 2007 | 2006 |

|---|---|---|---|---|---|---|---|

| Total | 103.8 | 97.6 | 94.6 | 12.3% | 86.8 | 95.8 | 112.1 |

| Northeast | 85.3 | 78.8 | 81.2 | 11.9 | 73.1 | 85.9 | 98.9 |

| Midwest | 90.8 | 88.1 | 89.9 | 7.6 | 80.6 | 89.5 | 101.9 |

| South | 104.6 | 103.8 | 100.7 | 8.3 | 89.6 | 107.3 | 127.2 |

| West | 130.5 | 112.5 | 100.4 | 22.3 | 99.5 | 92.3 | 109.6 |

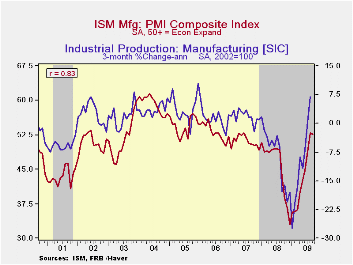

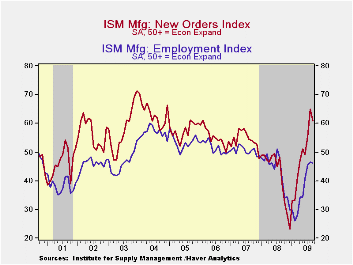

ISM Factory Index Remains Near Highest Level Since Early-2007 Suggesting Positive Growth

by Tom Moeller October 1, 2009

The National

Association of Purchasing Management data continued to indicate that

the recession in U.S. factory sector activity is over. Though the

September composite index slipped to 52.6 from 52.9 in August, it

remained near the highest level since June of 2007. (Any reading above

the break-even point of 50 suggests rising activity.) The latest figure

was up from the low of 32.9 hit last December but it fell short of

Consensus expectations for a reading of 54.0. The ISM data is available

in Haver's USECON database.

The National

Association of Purchasing Management data continued to indicate that

the recession in U.S. factory sector activity is over. Though the

September composite index slipped to 52.6 from 52.9 in August, it

remained near the highest level since June of 2007. (Any reading above

the break-even point of 50 suggests rising activity.) The latest figure

was up from the low of 32.9 hit last December but it fell short of

Consensus expectations for a reading of 54.0. The ISM data is available

in Haver's USECON database.

A sharp decline in

the production component to a still firm 55.7 accounted for much of the

latest decline. During the last ten years there has been an 84%

correlation between the level of the production component of the

composite index and the three-month growth in factory sector industrial

production.  It is appropriate to correlate the ISM index level

with factory sector output growth because the ISM

index is a diffusion index. It measures growth by using all of the

positive changes in activity added to one half of the zero change in

activity measures. The new orders component fell

just modestly. On the up side, the export order index at 55.0 was near

the highest in over a year, suggesting that recessions abroad are

winding down. During the last ten years there has been a 53%

correlation between the index and the q/q change in real exports of

goods in the GDP accounts.

It is appropriate to correlate the ISM index level

with factory sector output growth because the ISM

index is a diffusion index. It measures growth by using all of the

positive changes in activity added to one half of the zero change in

activity measures. The new orders component fell

just modestly. On the up side, the export order index at 55.0 was near

the highest in over a year, suggesting that recessions abroad are

winding down. During the last ten years there has been a 53%

correlation between the index and the q/q change in real exports of

goods in the GDP accounts.

The employment index also fell just slightly. Though the 46.2 reading continued to suggest a lower level of hiring, the index was near its highest level since last August and was up from the February low of 26.1. During the last ten years there has been a 90% correlation between the index level and the three-month change in manufacturing payrolls.

A reduced

rate of inventory

liquidation seems to be behind the factory sector's recent improvement.

The inventory index jumped to 42.5 which was its highest level since

last October. The speed of supplier deliveries also points toward

improvement in activity. Slower delivery speeds are indicated by a rise

in the index to its highest level since 2005 (no typo).

A reduced

rate of inventory

liquidation seems to be behind the factory sector's recent improvement.

The inventory index jumped to 42.5 which was its highest level since

last October. The speed of supplier deliveries also points toward

improvement in activity. Slower delivery speeds are indicated by a rise

in the index to its highest level since 2005 (no typo).

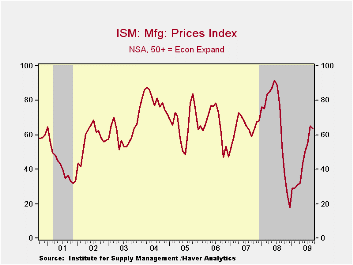

The separate index of prices paid also suggests improved factory sector activity. At 63.5, the reading was near its highest level since last August and it's up from the December low of 18.0. During the last twenty years there has been a 79% correlation between the price index and the three-month change in the PPI for intermediate goods.

| ISM Mfg | September | August | September '08 | 2008 | 2007 | 2006 |

|---|---|---|---|---|---|---|

| Composite Index | 52.6 | 52.9 | 43.4 | 45.5 | 51.1 | 53.1 |

| New Orders Index | 60.8 | 64.9 | 39.2 | 42.1 | 54.3 | 55.4 |

| Employment Index | 46.2 | 46.4 | 40.9 | 43.2 | 50.5 | 51.7 |

| Prices Paid Index (NSA) | 63.5 | 65.0 | 53.5 | 66.5 | 64.6 | 65.0 |

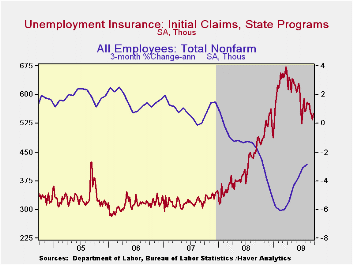

U.S. Weekly Claims For Jobless Insurance Tick Higher

by Tom Moeller October 1, 2009

Initial claims for jobless insurance ticked higher last week and suggested little labor market improvement since the summer. The Labor Department indicated that claims reversed the prior week's decline and rose 17,000 to 551,000, the highest since July. Nevertheless the latest was own from the March weekly peak of 674,000. The latest increase contrasted with expectations for 535,000 claims.

The largest increases in initial claims for the week ending

September 19 were in California (+5,112), Texas (+3,946), Florida

(+2,348), Iowa (+2,013), and Illinois (+1,945), while the largest

decreases were in Kansas (-1,545), Wisconsin (-1,258), Oregon (-833),

Ohio (-804), and New York (-623).

Continuing claims for unemployment insurance during the latest week fell 70,000 to their lowest level since April. The decline owes partially to the exhaustion of benefits. Continuing claims provide an indication of workers' ability to find employment. The four-week average of continuing claims fell modestly to 6,154,500. The series dates back to 1966.

Extended benefits for unemployment insurance rose for the third consecutive week. Through mid-September extended benefits averaged 440,716.

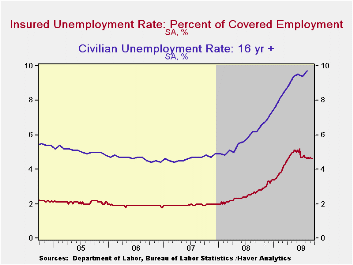

The insured rate of unemployment held at 4.6% and was near the lowest level since mid-April. The rate reached a high of 5.2% during late-June. During the last ten years, there has been a 93% correlation between the level of the insured unemployment rate and the overall rate of unemployment published by the Bureau of Labor Statistics.

The highest insured unemployment rates in the week ending September 12 were in Puerto Rico (6.1 percent), Oregon (5.4), Nevada (5.3), Pennsylvania (5.3), California (4.9), Michigan (4.9), Wisconsin (4.8), New Jersey (4.7), North Carolina (4.7), Arkansas (4.6), and South Carolina (4.6).

The unemployment insurance claims data is available in Haver's WEEKLY database and the state data is in the REGIONW database.

| Unemployment Insurance (000s) | 09/26/09 | 09/19/09 | 09/12/09 | Y/Y | 2008 | 2007 | 2006 |

|---|---|---|---|---|---|---|---|

| Initial Claims | 551 | 534 | 550 | 12.4% | 420 | 321 | 313 |

| Continuing Claims | -- | 6,090 | 6,160 | 67.4% | 3,342 | 2,552 | 2,459 |

| Insured Unemployment Rate (%) | -- | 4.6 | 4.6 | 2.7 (09/2008) | 2.5 | 1.9 | 1.9 |

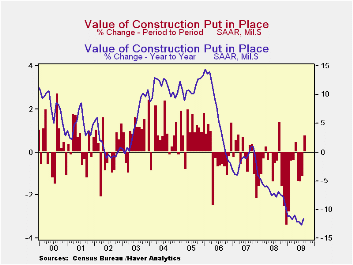

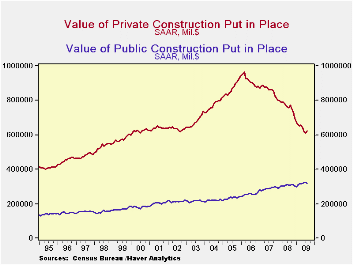

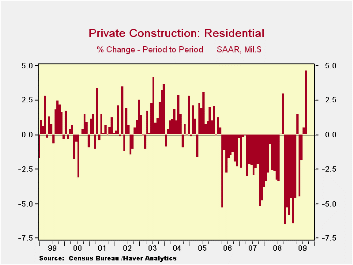

U.S. Construction Spending Gains in August, But June & July Revised Down

by Carol Stone October 1, 2009

The

headline sounded so promising: construction spending rose

0.8% in August, when forecasters had looked only for a 0.2% decrease.

But the pleasure with this result was short-lived. July's amount was

revised from -0.2% to -1.1% and June's from a marginal 0.1% increase to

a 1.4% fall. Some parts of the economy are improving, but much of

construction activity continues to lag. Total outlays in August were

11.6% below a year ago.

The

headline sounded so promising: construction spending rose

0.8% in August, when forecasters had looked only for a 0.2% decrease.

But the pleasure with this result was short-lived. July's amount was

revised from -0.2% to -1.1% and June's from a marginal 0.1% increase to

a 1.4% fall. Some parts of the economy are improving, but much of

construction activity continues to lag. Total outlays in August were

11.6% below a year ago.

Nonresidential projects remain the weakest. Those outlays

edged down 0.1% in August, and July was revised from -1.2% to -2.6%,

while June's figure was cut back from -2.2% to -4.0%. Over these last 3

months combined, nonresidential outlays dropped by 6.5%; the weakest

segments have been lodging, commercial and amusements, each down

12-15%; education (private structures), offices, transportation,

manufacturing and communication, down 5-8%, and health care, power and

religious construction activity have been flat to somewhat higher.

However, as Tom Moeller pointed out here a month ago, these declines

result mainly from poor business profits during the worst of the

recession; planning and building lead-times mean that recent work

reflects those discouraging business conditions from at least several

months ago or more. Now profits are improving and recovery in the

residential sector seems to be more firmly established. So the

implications for sustained turnaround in nonresidential construction

are much more positive now.

Over these last 3

months combined, nonresidential outlays dropped by 6.5%; the weakest

segments have been lodging, commercial and amusements, each down

12-15%; education (private structures), offices, transportation,

manufacturing and communication, down 5-8%, and health care, power and

religious construction activity have been flat to somewhat higher.

However, as Tom Moeller pointed out here a month ago, these declines

result mainly from poor business profits during the worst of the

recession; planning and building lead-times mean that recent work

reflects those discouraging business conditions from at least several

months ago or more. Now profits are improving and recovery in the

residential sector seems to be more firmly established. So the

implications for sustained turnaround in nonresidential construction

are much more positive now.

Public construction was down in August by 1.1%, as federal building activity fell 7.6%, while state and local government outlays decreased 0.5%. Increases over previous months mean that the year-on-year comparison still shows a gain, this of 3.3%.

| Construction (%) | August | July | June | Y/Y | 2008 | 2007 | 2006 |

|---|---|---|---|---|---|---|---|

| Total | 0.8 | -1.1 | -1.4 | -11.6 | -6.9 | -1.6 | 6.3 |

| Private | 1.8 | -1.4 | -3.2 | -17.8 | -11.1 | -5.7 | 5.5 |

| Residential | 4.7 | 0.6 | -1.8 | -26.7 | -29.1 | -19.7 | 1.0 |

| Nonresidential | -0.1 | -2.6 | -4.0 | -10.5 | 13.2 | 23.1 | 16.2 |

| Public | -1.1 | -0.7 | 2.2 | 3.3 | 5.6 | 13.1 | 9.3 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief