Global| Dec 21 2007

Global| Dec 21 2007U.S. Personal Consumption & Prices Firm, Income Light

by:Tom Moeller

|in:Economy in Brief

Summary

Personal consumption expenditures surged 1.1% last month after an upwardly revised 0.4% rise. The November increase beat Consensus expectations for a 0.7% rise. Adjusted for inflation spending rose 0.5% after the upwardly revised 0.1% [...]

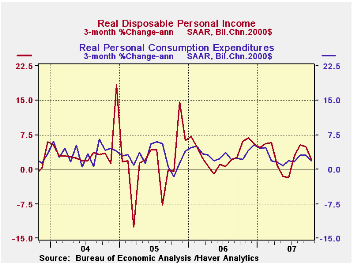

Personal consumption expenditures surged 1.1% last month after an upwardly revised 0.4% rise. The November increase beat Consensus expectations for a 0.7% rise. Adjusted for inflation spending rose 0.5% after the upwardly revised 0.1% uptick. Three month growth in real spending rose to 3.4% (AR).

Spending on discretionary items was firm led by a 1.8% (9.6% y/y) jump in real spending on household furniture & appliances. Spending on apparel also rose a firm 0.9% (5.6% y/y) but spending on motor vehicles fell 0.8% (+2.4% y/y). Spending on electricity surged 5.9% (6.9% y/y) but real spending on gasoline fell 0.3% (-0.6% y/y). Medical care spending rose 0.2% and spending on recreation fell 0.1%). Spending on food rose 0.7% (2.2% y/y). Real spending excluding food & energy rose 0.4% (3.2% y/y). These detailed spending figures are available in Haver's USNA database.

The PCE chain price index surged 0.6%%, lifted by higher energy prices. The core PCE price index gained a steady 0.2% but y/y growth in core prices picked up further to 2.2%. Three month growth in core prices rose to 2.9% (AR) due to faster growth in services prices where the three month growth of 4.0% was the fastest since late 2005.

Personal income during November rose 0.4% and the gain fell just short of expectations for a 0.5% rise. The October increase was unrevised at 0.2%. Three month growth in income was 4.2% (AR), its worst since June.

Lower interest rates caused a shortfall in interest income of 0.4% (+6.2% y/y) which was the same decline as in October. Conversely, growth in dividend income held steady at 0.9% (12.6% y/y), the same as during the prior two months.

Growth in wages & salaries picked back up to 0.6% (5.2% y/y) after an unchanged reading for October. Three month growth amounted to 5.3%. Factory sector wages rose 0.4% (2.2% y/y) after declining during the prior two months.Wage & salary income in the private service-producing industries rose 0.7% (6.1% y/y) after no change in October. Wages in the government sector again increased 0.4% (4.6% y/y).

Personal current taxes rose a firm 0.7% (8.1% y/y) and that left disposable personal income to rise 0.3% (5.8% y/y). Adjusted for inflation disposable personal income fell 0.3% (+2.1% y/y) for the second month of decline. That left the three month growth in real DPI negative at -0.9%, its worst since June.

| Disposition of Personal Income | November | October | Y/Y | 2006 | 2005 | 2004 |

|---|---|---|---|---|---|---|

| Personal Income | 0.4% | 0.3% | 6.1% | 6.6% | 5.9% | 6.2% |

| Personal Consumption | 1.1% | 0.4% | 6.7% | 5.9% | 6.2% | 6.4% |

| Saving Rate | -0.5% | 0.3% | 0.5% (Nov. 06) | 0.4% | 0.5% | 2.1% |

| PCE Chain Price Index | 0.6% | 0.3% | 3.6% | 2.8% | 2.9% | 2.6% |

| Less food & energy | 0.2% | 0.2% | 2.2% | 2.2% | 2.2% | 2.1% |

by Tom Moeller December 21, 2007

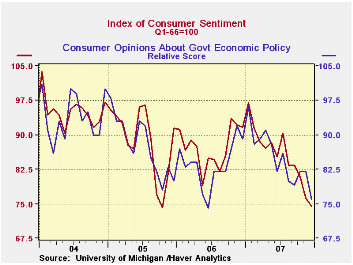

The University of Michigan's consumer sentiment index for all of this month fall 0.9% to 75.5.That was somewhat better than the reading at mid-month and it beat expectations for a December reading of 74.9. Nevertheless it left sentiment down 17.7% y/y.

Somewhat improved expectations caused the better December result. Expected business conditions during the next year fell only 6.8% (-35.2% y/y), an improvement from the -11.0% preliminary reading. Expectations for business conditions during the next five years also improved 6.6% (-16.5% y/y) from the November level and versus the initial read of a m/m decline. Down still is the result versus 3Q. Expectations for personal finances fell further by 2.6% (-9.7% y/y).

The current conditions index in fact was revised lower from the mid-month reading and fell 0.5% after a hefty 6.3% November decline. Current buying conditions for large household goods improved modestly m/m but remained down 13.0% from last December. The view of current personal finances, however, slid 3.0% for the second sharp monthly decline (-17.6% y/y).

The rise in gasoline prices raised expectations for inflation during the next twelve months to 4.4% (slightly lower than the mid-month read) from 4.3% in November and from 3.5% one year ago. For the next five to ten years expectations were for a 3.6% rise in prices.

Opinions about government policy dropped 9.8% m/m which brought this opinion measure down 16.9% from one year ago.

The University of Michigan survey is not seasonally adjusted.The reading is based on telephone interviews with about 500 households at month-end; the mid-month results are based on about 300 interviews. The summary indexes are in Haver's USECON database, with details in the proprietary UMSCA database.

Consumer sentiment, the economy, and the news media is a 2004 paper from the Federal Reserve Bank of San Francisco and it can be found here.

| University of Michigan | Dec (Final) | Dec (Prelim) | Nov | Dec y/y | 2006 | 2005 | 2004 |

|---|---|---|---|---|---|---|---|

| Consumer Sentiment | 75.5 | 74.5 | 76.1 | -17.7% | 87.3 | 88.5 | 95.2 |

| Current Conditions | 91.0 | 92.1 | 91.5 | -15.8% | 105.1 | 105.9 | 105.6 |

| Expectations | 65.6 | 63.2 | 66.2 | -19.2% | 75.9 | 77.4 | 88.5 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief