Global| Jun 02 2010

Global| Jun 02 2010U.S. Pending Home Sales StrongAgain

by:Tom Moeller

|in:Economy in Brief

Summary

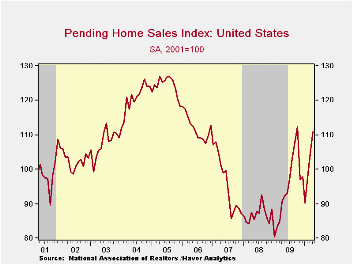

The National Association of Realtors (NAR) reported that pending sales of existing single-family homes rose 6.0% during April versus March. The gain left home sales up 37.8% from the low in January of last year. The latest marginally [...]

The National Association of Realtors (NAR) reported that pending sales of existing single-family homes rose 6.0% during April versus March. The gain left home sales up 37.8% from the low in January of last year. The latest marginally beat Consensus expectations for a 5.0% increase.

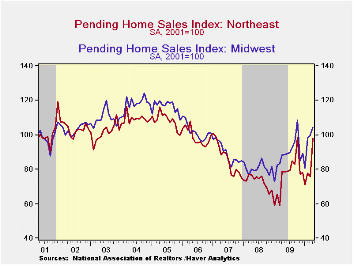

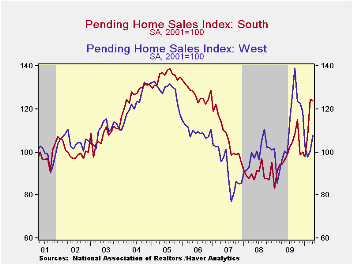

The m/m performance of home sales continued to vary across the country. Last month sales rose in the Northeast (24.4 y/y), Midwest (18.0% y/y) and in the West (12.0% y/y). A modest decline in sales was logged in the South but sales still rose by nearly one-third versus last year.

Pending home sales figures are analogous to the new home sales data from the Commerce Department in that they measure existing home sales when the sales contract is signed, not at the time the sale is closed. The series dates back to 2001 and the data is available in Haver's PREALTOR database.

| Pending Home Sales (2001=100) | April | March | February | Y/Y % | 2009 | 2008 | 2007 |

|---|---|---|---|---|---|---|---|

| Total | 110.9 | 104.6 | 97.7 | 22.4 | 95.1 | 86.9 | 95.9 |

| Northeast | 97.9 | 75.6 | 77.7 | 24.4 | 76.7 | 73.0 | 86.1 |

| Midwest | 104.2 | 100.1 | 97.7 | 18.0 | 88.8 | 80.7 | 89.6 |

| South | 123.9 | 124.6 | 107.5 | 31.4 | 98.9 | 90.3 | 107.4 |

| West | 107.9 | 100.4 | 98.0 | 12.0 | 109.9 | 99.2 | 92.1 |

by Tom Moeller June 2, 2010

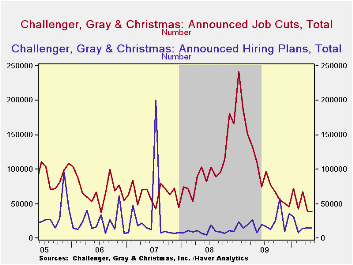

According to the outplacement firm of Challenger, Grey & Christmas the level of layoffs rose slightly m/m during May to 38,810. Nevertheless, the figure was off by roughly two-thirds from last year and just slightly above the lowest level since 2000. Planned layoffs announced during the first five months of 2010 totaled 258,319, down 68.6% from the 822,282 announced during early-2009. In virtually all industries except entertainment/leisure and pharmaceutical layoffs were down last month versus May 2009.

Challenger also samples firms' hiring plans. During May plans fell slightly after a strong gain during April. Versus May '09 plans rose 83.7% but during the first five months of this year they've fallen slightly y/y. Plans eased during May in the transportation, health care & financial sectors but strengthened in the auto, energy, industrial goods & services industries.

During the last ten years there has been a 67% (inverse) correlation between the three-month moving average of announced job cuts and the three-month change in payroll employment. Job cut announcements differ from layoffs. Many are achieved through attrition, early retirement or just never occur.

The Challenger figures are available in Haver's SURVEYS database.

| Challenger, Gray & Christmas | May | April | March | Y/Y | 2009 | 2008 | 2007 |

|---|---|---|---|---|---|---|---|

| Announced Job Cuts | 38,810 | 38,326 | 67,611 | -65.1% | 1,288,030 | 1,223,993 | 768,264 |

| Announced Hiring Plans | 14,922 | 15,654 | 13,994 | 83.7% | 272,573 | 118,600 | 365,583 |

by Robert Brusca June 2, 2010

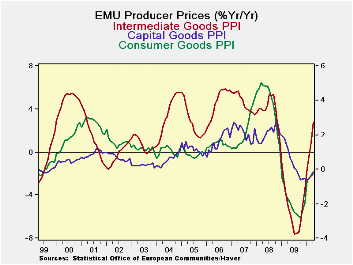

Producer price trends have been rising sharply in EMU over the past few months. The PPI has taken a decided and sharp turn for the worse. Prices are accelerating in two of the three main sectors of the PPI. Only consumer prices fail to show acceleration from three-months to six months. Consumer prices and intermediate prices are still lower Yr/Yr but their trends are nonetheless rising sharply. Intermediate goods prices are up very strongly from past weakness.

Germany and France show manufacturing prices ex-energy or ex-energy and ex-food trends (the former for Germany, the latter for France) with accelerations in train. UK manufactures prices are accelerating (the UK is an EU member). Italy’s prices are actually decelerating over three months compared to stronger pressures earlier.

While the PPI is not the price a gauge of choice for the ECB, having such pressures stirred up will not be good news. The dropping euro undoubtedly has something to do with this.

Still Yr/Yr prices are contained for consumer goods and capital goods. Intermediate goods prices are the biggest problem. There the rise in the dollar price of oil and the dropping euro form a double-whammy on prices. If these trends develop in the HICP they will put the ECB on the spot since growth in the Zone is not doing well and the ECB will not want inflation trends like this to take hold in consumer prices.

| Euro-Area and UK PPI Trends | ||||||

|---|---|---|---|---|---|---|

| M/M | Saar | |||||

| Euro-Area | Apr-10 | Mar-10 | 3-Mo | 6-MO | Yr/Yr | Y/Y Yr Ago |

| TotalxConstruct | 0.7% | 0.6% | 5.8% | 6.4% | 2.8% | -4.7% |

| Capital Gds | 0.2% | 0.1% | 1.1% | 0.4% | -0.2% | 1.2% |

| Consurmer Gds | 0.1% | 0.0% | 0.5% | 0.7% | -0.3% | -1.7% |

| Intermediate&Cap Gds | 1.0% | 0.8% | 8.1% | 6.8% | 2.7% | -5.1% |

| MFG | 0.4% | 0.6% | 3.9% | 6.2% | 3.7% | -5.9% |

| Germany | ||||||

| Gy ExEnergy | 0.5% | 0.2% | 4.3% | 3.1% | 1.1% | -1.9% |

| France:Tot | ||||||

| Fr ExF&Energy | 0.6% | 0.3% | 4.2% | 3.3% | 1.0% | -1.6% |

| Italy | 0.5% | 0.5% | 3.7% | 6.7% | 4.1% | -6.2% |

| UK | 0.9% | 0.6% | 8.1% | 7.1% | 5.8% | 1.3% |

| Euro-Area Harmonized PPI ex construction | ||||||

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief