Global| May 04 2009

Global| May 04 2009U.S. Pending Home Sales Rise For A Second Month

by:Tom Moeller

|in:Economy in Brief

Summary

For March, the National Association of Realtors reported that pending sales of existing homes rose another 3.2% following their little revised 2.0% gain during February. While surprising, the gains failed to recoup a sharp 7.7% [...]

For March, the National Association of Realtors reported that pending sales of existing homes rose another 3.2% following their little revised 2.0% gain during February. While surprising, the gains failed to recoup a sharp 7.7% decline during January. Therefore, for the first quarter as a whole, sales fell 3.8% to a new series low. Consensus expectations had been for no change in March sales versus February.

Last month's gain in home sales was contained to just South (+7.7% y/y) and the West (+1.6%). Elsewhere, sales in the Northeast remained quite weak and fell month-to-month (-24.2%) while sales in the Midwest slipped 1.0%. Year-to-year, however, sales in the Midwest have rebounded 8.3%.

The home sales figures are analogous to the new home sales data from the Commerce Department in that they measure existing home sales when the sales contract is signed, not at the time the sale is closed. The series dates back to 2001.

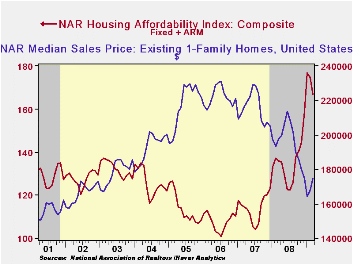

The latest monthly gains in home sales have been accompanied

by a rise in home prices. The median sales price of an existing home

rose 4.2% in March (-12.4% y/y). The increase was the second

consecutive gain but it followed seven straight months of decline.

Prices were down by one quarter from their peak during June 2007. The

latest gains in home prices did lower housing affordability slightly

but the decline has been small. Therefore, combined with lower interest

rates, the affordability index of a home remained up by 22.7%

year-to-year and by three quarters from the 2006 low. The latest level

was a record high for the series which extends back to 1970.

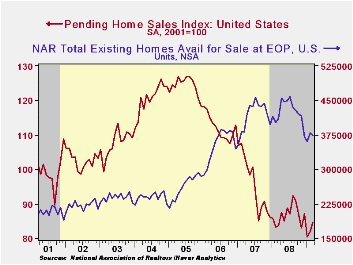

Weak home sales are encouraging potential sellers to keep their homes off the market. The Realtors Association indicated in an earlier report that the number of homes on the market and available for sale fell 9.3% during March versus one year earlier.

At the current sales rate there was a 9.8 months' supply of homes on the market and there was a 10.4 months' supply during all of last year, up from the 8.9 months supply during 2007 and 6.5 months during 2006. For single family homes, there was a 9.3 months' supply in February versus a full-year figure of 10.0 months during 2008.

The pending home sales data are available in Haver's PREALTOR database. The number of homes on the market and prices are in the REALTOR database.

| Pending Home Sales (2001=100) | March | February | Y/Y | 2008 | 2007 | 2006 |

|---|---|---|---|---|---|---|

| Total | 84.6 | 82.0 | 1.1% | 86.8 | 95.8 | 112.1 |

| Northeast | 59.5 | 63.1 | -24.1 | 72.6 | 85.6 | 98.5 |

| Midwest | 82.3 | 83.1 | 8.3 | 80.6 | 89.5 | 102.0 |

| South | 93.2 | 85.9 | 7.7 | 89.8 | 107.3 | 127.3 |

| West | 93.1 | 89.6 | 1.6 | 99.3 | 92.1 | 109.5 |

by Tom Moeller May 4, 2009

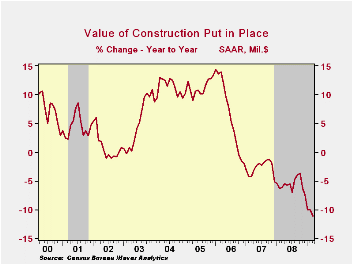

Regrettably, recent gains in the value of construction spending have been limited, small and tenuous. The value of construction put-in-place unexpectedly increased 0.3% during March following five consecutive months of decline in excess of 3% each month. Consensus expectations had been for a 1.5% drop.

A 2.0% jump in the value of nonresidential building activity accounted for much of the March surprise. The collapse of corporate profits, however, has dropped the y/y gain to just 1.7% after double-digit increases during the prior three years. The March increase reflected gains in the lodging (-5.1% y/y), commercial (-20.5 y/y), health care (+3.9% y/y), and educational (5.4% y/y) sectors.

Public construction also was strong during March and posted a

1.1% increase. The recession's effect on tax revenues, however, seems

to be taking hold. The small 2.6% year-to-year increase in the level of

activity for March left the first quarter's level just equal to the

2008 average. The value of spending on transportation facilities did

rise 1.7% in March but it was down 6.0% year-to-year while spending on

highways & streets fell 0.8% (-2.2% y/y) and was down for the

fourth straight month. The value of construction on highways &

streets is roughly one-third of the value of total public construction

spending.

The value of residential building activity continued down hard and it posted a 4.2% decline, off by one-third over the last year. Notably hard hit has been single-family construction activity which fell 8.6% in March and is off by one-half during the last twelve months. Building activity on multi-family units has held up relatively well and posted a March decline of just 1.1% (-13.7% y/y). Spending on improvements fell 1.0% (-13.1% y/y).

During the last twenty years there has been an 84% correlation between the q/q change in the value of residential building and its contribution to growth in real GDP.

The more detailed categories of construction represent the Census Bureau’s reclassification of construction activity into end-use groups. Finer detail is available for many of the categories; for instance, commercial construction is shown for automotive sales and parking facilities, drugstores, building supply stores, and both commercial warehouses and mini-storage facilities. Note that start dates vary for some seasonally adjusted line items in 2000 and 2002, and that constant-dollar data are no longer computed.

The construction put-in-place figures are available in Haver's USECON database.

| Construction (%) | March | February | Y/Y | 2008 | 2007 | 2006 |

|---|---|---|---|---|---|---|

| Total | 0.3 | -1.0 | -11.1 | -5.7 | -2.7 | 6.3 |

| Private | -0.1 | -2.1 | -16.3 | -9.8 | -6.9 | 5.5 |

| Residential | -4.2 | -5.9 | -34.0 | -27.7 | -19.8 | 1.0 |

| Nonresidential | 2.7 | 0.7 | 1.2 | 14.9 | 19.6 | 16.2 |

| Public | 1.1 | 1.3 | 2.6 | 6.7 | 12.3 | 9.3 |

by Tom Moeller May 4, 2009

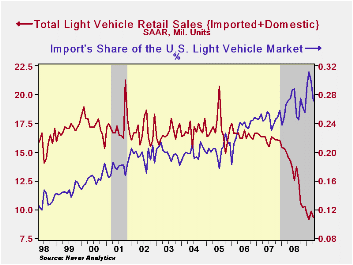

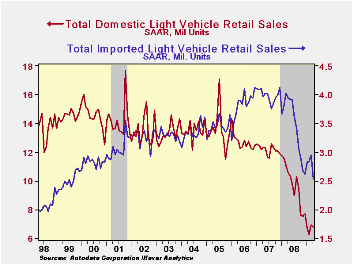

What lift may have been evident in sales of light vehicles dissolved with the report that sales in April fell, despite a new round of price discounts. U.S. unit sales of light vehicles reversed most of a March gain with a 5.5% m/m decline to 9.32M units (SAAR). The best that can be observed about sales is that the earlier decline has flattened out here in 2009 but they do remain near the lowest since 1982 according to the Autodata Corporation and Ward's Automotive News. (Seasonal adjustment of the figures is provided by the U.S. Bureau of Economic Analysis).

Imported light vehicle sales fell a hard

14.0% m/m last month to their lowest level in more than ten years. A

22.7% decline in light truck sales to 0.84M led that decline while

sales of imported autos fell a lesser 8.9%. That drop reversed nearly

all of a March increase and left sales at their lowest level of this

year.

Sales of domestically-made light vehicles reversed a piece of the prior month's 10.1% increase with a m/m decline of 2.0% from March to 6.78M units. Sales of domestically made light trucks slipped 0.6% to 3.67M units after their impressive 8.7% March gain. Auto sales, however, fell larger 3.6% to 3.10M units.

Overall, import's share of the U.S. light vehicle market fell sharply to 27.2% which was their lowest level of this year. Nevertheless, the figure remained up the 2008 average of 26.3%. (Imported vehicles are those produced outside the United States.) Imports' share of the U.S. car market totaled 35.3%, up slightly from the 2008 average, while the share of the light truck market was 18.5%, roughly equal to last year.

The U.S. vehicle sales figures can be found in Haver's USECON database.

New vehicle characteristics and the cost of the corporate average fuel economy standard from the Federal Reserve Bank of Chicago can be found here.

| Light Vehicle Sales (SAAR, Mil. Units) | April | March | February | April Y/Y | 2008 | 2007 | 2006 |

|---|---|---|---|---|---|---|---|

| Total | 9.32 | 9.83 | 9.12 | -35.8% | 13.17 | 16.16 | 16.54 |

| Autos | 4.81 | 5.05 | 4.63 | -35.5 | 6.71 | 7.58 | 7.77 |

| Domestic | 3.11 | 3.23 | 2.89 | -36.0 | 4.42 | 5.07 | 5.31 |

| Imported | 1.70 | 1.83 | 1.74 | -34.7 | 2.29 | 2.52 | 2.45 |

| Light Trucks | 4.51 | 4.78 | 4.50 | -36.2 | 6.47 | 8.60 | 8.78 |

| Domestic | 3.67 | 3.70 | 3.40 | -35.8 | 5.29 | 7.10 | 7.42 |

| Imported | 0.84 | 1.08 | 1.10 | -38.9 | 1.18 | 1.47 | 1.37 |

by Louise CurleyMay 4, 2009

Manufacturing activity

around the world appears to have

stopped contracting.Markit Economics reported today that the diffusion

indexes representing the opinions of purchasing managers in

manufacturing in a number of countries have continued to show

improvement in April. As the attached charts show, the PMI's in

countries in Eastern Europe and in the Far East reached their low

points at the end of last year. Those in Western Europe reached their

low points early this year.

Manufacturing activity

around the world appears to have

stopped contracting.Markit Economics reported today that the diffusion

indexes representing the opinions of purchasing managers in

manufacturing in a number of countries have continued to show

improvement in April. As the attached charts show, the PMI's in

countries in Eastern Europe and in the Far East reached their low

points at the end of last year. Those in Western Europe reached their

low points early this year.

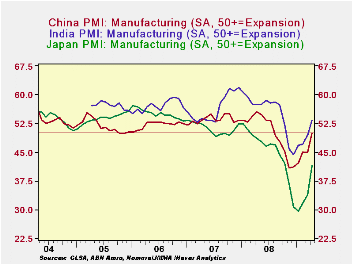

The best showing has been in the Far East. The PMI for India

reached 53.27% in April, putting manufacturing in India in an expansion

phase. China with a PMI of 50.05% has just inched into the expansion

phase. Although Japan's PMI of 41.42% indicates that manufacturing in

Japan is still contracting, the degree of contraction is well below

that reached at the end of last year. The first chart shows the PMI's

for India, China and Japan.

The best showing has been in the Far East. The PMI for India

reached 53.27% in April, putting manufacturing in India in an expansion

phase. China with a PMI of 50.05% has just inched into the expansion

phase. Although Japan's PMI of 41.42% indicates that manufacturing in

Japan is still contracting, the degree of contraction is well below

that reached at the end of last year. The first chart shows the PMI's

for India, China and Japan.

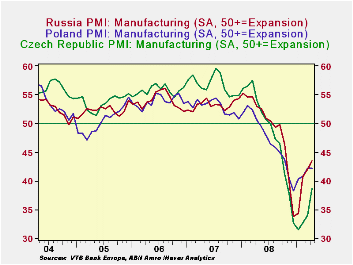

Like Japan the PMI's in Eastern Europe suggest that degree of

contraction in manufacturing in Russia, Poland and the Czech Republic

is slowing, but they are still below the expansion phase, as shown in

the second chart.

Like Japan the PMI's in Eastern Europe suggest that degree of

contraction in manufacturing in Russia, Poland and the Czech Republic

is slowing, but they are still below the expansion phase, as shown in

the second chart.

| PURCHASING MANAGERS SURVEY OF MANUFACTURING | Apr 09 | Mar 09 |

|---|---|---|

| Diffusion Indexes 50+ = Expansion (SA) | ||

| China | 50.05 | 44.83 |

| Japan | 41.42 | 33.83 |

| India | 53.27 | 49.46 |

| Czech Republic | 38.61 | 33.95 |

| Poland | 42.14 | 41.42 |

| Russia | 43.43 | 41.97 |

| Switzerland | 34.69 | 32.62 |

| United Kingdom | 42.85 | 39.50 |

| Euro Area | 36.83 | 33.92 |

by Robert BruscaMay 4, 2009

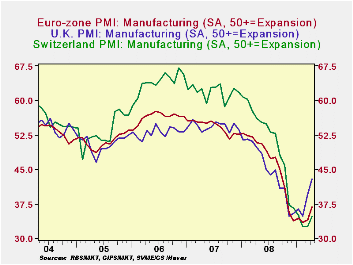

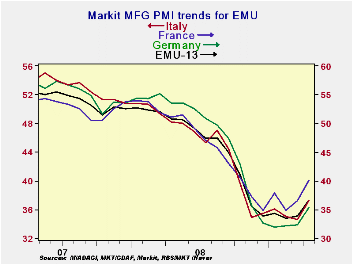

Europe’s PMI readings bounced sharply in April across EMU

nations. France made the second largest monthly rise at 3.59 points

just above the UK’s 3.35 point gain. From its cycle low, the UK has

made the greatest gain rising by 8 points with Spain and Austrian next

on gains of 6.1 and 5.9 points respectively from their cycle lows.

Italy has rebounded the least with a rise from its low reading of just

2.6 points. Looking at the levels of the indices in their respective

range of value they have occupied Italy is also the weakest followed by

Germany even though Italy’s raw MFG reading is higher than Germany’s.

These statistics show us that Europe is stirring from its lows

across countries. The UK and France are making the largest initial

moves, while Germany, the EMU’s largest economy, is one of the worst

laggards.

Just today the EU Commission has cut its outlook for growth in

EU this year, on Monday it revised lower its forecast for growth in the

European Union this year citing consumers reacting to the weakening

labor market and the slump in world trade as well as the effects of an

ongoing housing market correction. The commission, the executive arm of

the EU, presented its spring quarterly economic forecasts that

projected that gross domestic product in both the European Union and

the euro area would contract by 4 percent in 2009 and by 0.1 percent in

2010.

So amid signs that the EMU economy may have begun to

decelerate at a slower rate paving the way for an eventual upturn the

EU commission has unleashed a more pessimistic outlook.

| NTC/Markit MFG Indices | |||||||

|---|---|---|---|---|---|---|---|

| Apr-09 | Mar-09 | Feb-09 | 3-Mo | 6-Mo | 12-Mo | Percentile | |

| Euro-13 | 36.83 | 33.93 | 33.55 | 34.77 | 34.70 | 40.75 | 13.6% |

| Germany | 35.40 | 32.36 | 32.14 | 33.30 | 33.36 | 41.43 | 12.5% |

| France | 40.10 | 36.51 | 34.81 | 37.14 | 36.92 | 41.55 | 21.1% |

| Italy | 37.21 | 34.59 | 34.99 | 35.60 | 35.56 | 40.40 | 11.4% |

| Spain | 34.61 | 32.92 | 31.85 | 33.13 | 31.47 | 35.64 | 21.3% |

| Austria | 38.97 | 33.68 | 34.58 | 35.74 | 35.60 | 41.40 | 22.7% |

| Greece | 40.88 | 38.17 | 38.88 | 39.31 | 40.19 | 45.98 | 15.8% |

| Ireland | 36.10 | 35.12 | 33.20 | 34.81 | 36.39 | 39.99 | 13.1% |

| Netherlands | 38.76 | 35.92 | 35.47 | 36.72 | 37.26 | 43.12 | 13.5% |

| EU | |||||||

| UK | 42.85 | 39.50 | 34.93 | 39.09 | 37.34 | 40.69 | 37.2% |

| percentile is over range since March 2000 | |||||||

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief