Global| Feb 02 2010

Global| Feb 02 2010U.S. Pending Home Sales Improve

by:Tom Moeller

|in:Economy in Brief

Summary

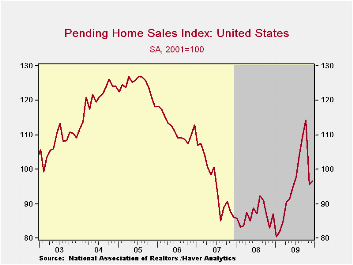

Home sales recovered during December after falling sharply in November with the (since-extended) expiration of an $8,000 first-time home buyers tax credit. The National Association of Realtors (NAR) reported that December pending home [...]

Home

sales

recovered during December after falling sharply in November with the

(since-extended) expiration of an $8,000 first-time home buyers tax

credit. The National Association of Realtors (NAR) reported that

December pending home sales rose 1.0% from November. Home sales

remained up 20.1% from the January low and the latest increase matched

Consensus expectations.

Home

sales

recovered during December after falling sharply in November with the

(since-extended) expiration of an $8,000 first-time home buyers tax

credit. The National Association of Realtors (NAR) reported that

December pending home sales rose 1.0% from November. Home sales

remained up 20.1% from the January low and the latest increase matched

Consensus expectations.

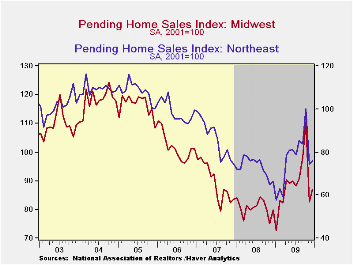

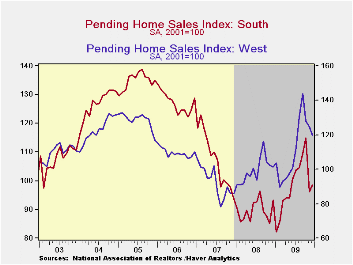

Modest monthly gains in home sales were recorded across the country.

These home sales figures are analogous to the new home sales data from the Commerce Department in that they measure existing home sales when the sales contract is signed, not at the time the sale is closed. The series dates back to 2001 and the data is available in Haver's PREALTOR database.

Recent Development in Mortgage Finance from the Federal Reserve Bank of San Francisco can be found here.

| Pending Home Sales (2001=100) | December | November | October | Y/Y | 2009 | 2008 | 2007 |

|---|---|---|---|---|---|---|---|

| Total | 98.6 | 95.6 | 114.3 | 10.9% | 95.1 | 86.8 | 95.8 |

| Northeast | 76.1 | 74.4 | 100.2 | 15.0 | 76.6 | 73.1 | 85.9 |

| Midwest | 86.9 | 82.6 | 110.3 | 8.6 | 88.7 | 80.6 | 89.5 |

| South | 98.4 | 96.3 | 115.1 | 14.8 | 98.2 | 89.6 | 107.3 |

| West | 119.9 | 124.6 | 128.1 | 18.6 | 111.5 | 99.5 | 92.3 |

by Tom Moeller February 2, 2010

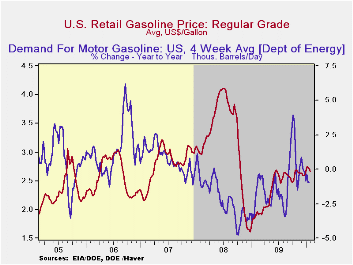

After

hitting the high last June the pump price for regular

gasoline has been roughly unchanged. Last week, the price

slipped to $2.66 and compares to $2.69 reached during June.

Nevertheless, prices remained up 41% from last year. Yesterday, the

spot market price for a gallon of regular gasoline was near last week's

level at $1.94 but down from the January high of $2.14. The figures are

reported by the U.S. Department of Energy and can be found in Haver's WEEKLY

& DAILY databases.

After

hitting the high last June the pump price for regular

gasoline has been roughly unchanged. Last week, the price

slipped to $2.66 and compares to $2.69 reached during June.

Nevertheless, prices remained up 41% from last year. Yesterday, the

spot market price for a gallon of regular gasoline was near last week's

level at $1.94 but down from the January high of $2.14. The figures are

reported by the U.S. Department of Energy and can be found in Haver's WEEKLY

& DAILY databases.

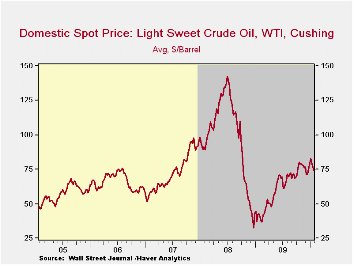

Earlier strength in the price for a barrel of light sweet crude (WTI) oil eased somewhat. Last week's price of $74.03 for a barrel of light sweet crude (WTI) was down from the high of $82.59 reached three weeks earlier. Yesterday, the spot price of $74.43 was up slightly from last week. Nevertheless, prices have risen from $71.53 early this past December and are more than double the December 2008 low of $32.37.· Demand for gasoline last week posted a 1.0% decline versus one year ago. That decline compared to a 3.9% increase at the beginning of October. Breaking away from earlier y/y strength, the demand for residual fuel oil fell 19.8% y/y. Distillate demand fell 9.8% y/y, a decline more moderate than the 21.6% y/y shortfall at the beginning of last July. Inventories of crude oil and petroleum products fell in January by 6.1% from the July high and were up just 0.4% from one year ago.

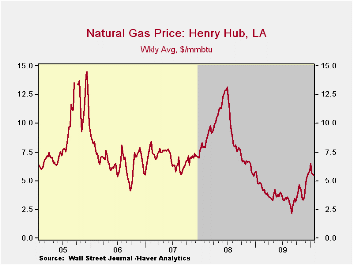

As temperatures moderated, U.S. natural gas prices backed off to an average $5.46 per mmbtu (15.0% y/y) from the high of $6.50 early in January. Nevertheless they remained up from $3.35 in November, triple the September low but down by half from the high reached in early-July of 2008 of $13.19/mmbtu.

The energy price data can be found in Haver's WEEKLY database while the daily figures are in DAILY. The gasoline demand figures are in OILWKLY.· Real-time inflation Forecasting in a Changing World from the Federal Reserve Bank of New York can be found here

| Weekly Prices | 02/01/10 | 01/25/10 | 01/18/10 | Y/Y | 2009 | 2008 | 2007 |

|---|---|---|---|---|---|---|---|

| Retail Regular Gasoline ($ per Gallon, Regular) | 2.66 | 2.71 | 2.74 | 40.6% | 2.35 | 3.25 | 2.80 |

| Light Sweet Crude Oil, WTI ($ per bbl.) | 74.03 | 76.76 | 80.07 | 74.1% | 61.39 | 100.16 | 72.25 |

by Robert Brusca February 2, 2010

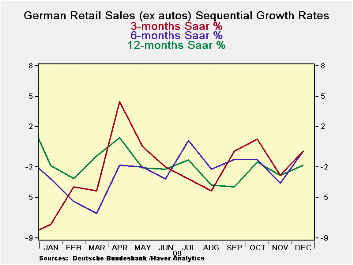

German retail sales rose by 0.8% in both real and nominal terms (ex autos) in December. The rise still leaves the 3-month nominal growth rate for sales in a mild negative path while in real terms retail sales are flat over three months. In the quarter the annual rate pace for both real and nominal sales is just below 1%. Car sales that had boosted consumer activity due to government incentives to buy a new car and scrap an old one have now left sales week. Auto registration fell by 15.7% in December after falling by 9.8% in November. Auto registrations are now off by 4.7% Yr/Yr

The trend for the German consumer is still poor. There is a very gradual improvement as the negative growth rates are climbing slowly back toward zero. But at this pace the German consumer is not posed to take the German economy anywhere.

German Real and Nominal Retail Sales| German Real and Nominal Retail Sales | QTR | |||||||

|---|---|---|---|---|---|---|---|---|

| Nominal | Dec-09 | Nov-09 | Oct-09 | 3-MO | 6-MO | 12-MO | YrAgo | Saar |

| Retaill Ex auto | 0.8% | -1.9% | 1.0% | -0.4% | -0.4% | -1.8% | 3.2% | -0.8% |

| MV and Parts | 0.8% | -1.7% | 0.9% | 0.0% | 0.4% | -2.5% | 3.4% | -0.7% |

| Food Bev & Tobacco | 1.0% | -0.5% | -0.9% | -1.6% | 0.4% | -0.9% | 4.1% | -5.1% |

| Clothing footwear | 3.4% | -9.3% | 8.8% | 8.0% | 2.1% | 0.2% | 1.9% | 10.6% |

| car registrations (units) | -15.7% | -9.8% | -0.1% | -66.6% | -60.2% | -4.7% | -6.7% | 0.0% |

| Real | ||||||||

| Retail Ex auto | 0.8% | -1.7% | 0.9% | 0.0% | 0.4% | -2.5% | 3.4% | -0.7% |

by Louise Curley February 2, 2010

Data

for

retail sales, excluding motor vehicles and motorcycles, in France and

in Germany were released today. The latest date for France is

November and for Germany, December.

Data

for

retail sales, excluding motor vehicles and motorcycles, in France and

in Germany were released today. The latest date for France is

November and for Germany, December.

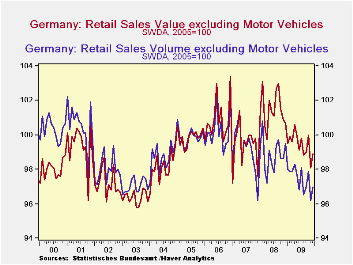

Retail trade in Germany continues to disappoint. Both the volume and value of trade increased 0.8% in December but they are no higher than they were October. The volume of trade in December was 97.0 (2005=100) compared with 97.9 in October. The corresponding figures for the value of trade were 98.9 and 100.0. With the GfK Consumer Climate Survey released last week pointing to a continuing deterioration of the consumer climate in January and February, the outlook for retail sales is not encouraging. The first chart shows that the declining trends in both the value and the volume of retail trade, which began in early 2008, are continuing.

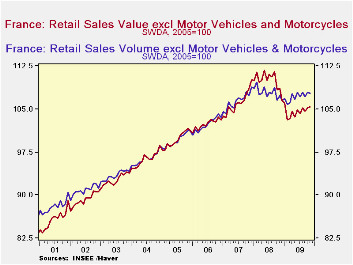

The picture in France is more

encouraging.

Although both volume and value have had their

ups and down, the declines in the volume and value of retail trade have

been less severe than those in Germany and the trends for both appear

to have begun to turn up since May of this year. There was no

change in the value of trade in November--the index remaining at 105.2;

there was a slight decline in the volume of trade to 107.8 from 107.9

in October. The value and volume of retail trade in France

are shown in the second chart.

encouraging.

Although both volume and value have had their

ups and down, the declines in the volume and value of retail trade have

been less severe than those in Germany and the trends for both appear

to have begun to turn up since May of this year. There was no

change in the value of trade in November--the index remaining at 105.2;

there was a slight decline in the volume of trade to 107.8 from 107.9

in October. The value and volume of retail trade in France

are shown in the second chart.

Since the data are available only in index form, the absolute volume and value of retail trade are unknown. All we know is that, in the case of Germany, the volume of retail trade in December was 3% below its volume in 2005 and the value, 1.1% below 2005. In France, the volume of retail trade in November was 7.8% above its 2005 volume and the value, 5.2% above. The volume and value of retail sales in Germany are still below levels reached in 2005, while in France the volume and value of retail sales have surpassed 2005 levels.

| Value of Retail Trade (2005=100) | Dec 09 | Nov 08 | Oct 09 | Sep 09 | Aug 09 | Jul 09 | Jun 09 | May 09 |

|---|---|---|---|---|---|---|---|---|

| Germany | 98.9 | 98.1 | 100.0 | 99.0 | 98.8 | 99.8 | 99.1 | 99.9 |

| France | 105.2 | 105.2 | 104.6 | 105.2 | 104.2 | 104.9 | 103.6 | |

| Volume of Retail Trade (2005=100) | ||||||||

| Germany | 97.0 | 96.2 | 97.9 | 97.0 | 96.5 | 98.1 | 96.8 | 97.7 |

| France | 107.8 | 107.9 | 107.1 | 107.9 | 107.1 | 107.9 | 106.7 | |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief