Global| Oct 02 2009

Global| Oct 02 2009U.S. Payrolls Decline Again While Jobless Rate Increases

by:Tom Moeller

|in:Economy in Brief

Summary

For September, the employment figures from the Bureau of Labor Statistics were uniformly weak. Payrolls fell a more-than-expected 263,000. Hours worked fell again. The unemployment rate rose to 9.8%, the highest since 1983. All in [...]

For September, the employment figures from the Bureau of Labor

Statistics were uniformly weak. Payrolls fell a more-than-expected

263,000. Hours worked fell again. The unemployment rate rose to 9.8%,

the highest since 1983. All in all, they suggest that the rate of

decline in the job market has slowed, but an upturn still is not

evident.

For September, the employment figures from the Bureau of Labor

Statistics were uniformly weak. Payrolls fell a more-than-expected

263,000. Hours worked fell again. The unemployment rate rose to 9.8%,

the highest since 1983. All in all, they suggest that the rate of

decline in the job market has slowed, but an upturn still is not

evident.

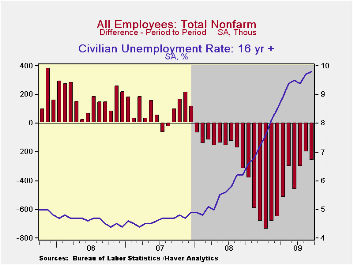

Nonfarm payrolls fell 263,000 during September. That exceeded expectations for a 180,000 decline and while the August shortfall was lessened, July's was deepened. So far during this recession employment has fallen by a total of 7.2 million, by far the record for a 21-month period. In percentage terms, jobs are down 5.2% since the 2007 peak, also a record. If there is good news, it's that the decline in payroll declines moderated to an average 256,000 over the last three months versus a peak rate of 701,000 this past winter.

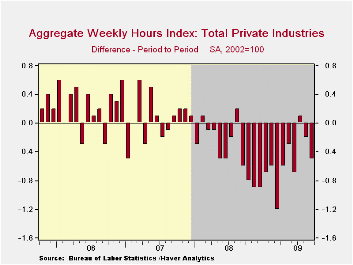

The length of the average workweek fell back to the cycle low of 33.0 hours. Combined with the decline in payrolls that was enough to pull 3Q aggregate hours worked (employment times hours) down at a 3.0% annual rate after a 7.8% decline during 2Q. Productivity needs to rise more than that if real GDP is going to rise as is widely expected.

The increase in the unemployment rate to 9.8% from 9.7% was

as-expected and it left the rate at the highest level since 1983. The

rate's cycle low of 4.4% occurred in October 2006. The official

unemployment rate pales, however, in comparison to the rate which

includes "marginally attached workers" and those who are working

part-time for economic reasons. It rose to 17.0%. Including

"discouraged workers" the unemployment rate stood at 10.2%.

The increase in the unemployment rate to 9.8% from 9.7% was

as-expected and it left the rate at the highest level since 1983. The

rate's cycle low of 4.4% occurred in October 2006. The official

unemployment rate pales, however, in comparison to the rate which

includes "marginally attached workers" and those who are working

part-time for economic reasons. It rose to 17.0%. Including

"discouraged workers" the unemployment rate stood at 10.2%.

The increase in the overall jobless rate was due to a 785,000 (-4.3% y/y) decline in household employment. That was shallower than the worst monthly declines of this past winter but worse than those of the last several months. It was accompanied by a sharp 571,000 (-0.4% y/y) decline in the labor force reflecting the discouraged workers. Also from the household survey, the median duration of unemployment jumped m/m to 17.3 weeks, just below this cycle's high reached in June. The ranks of the long-term unemployed rose to 5.438 million (166.4% y/y), an historic high. By educational attainment, those with a high school diploma but no college saw employment fall 5.2% y/y while those with a bachelor's degree or higher experienced a 0.7% decline.

From the payroll survey, the quickening in the rate of job

loss last month was due to a faster 94,000 (-3.1% y/y) decline in

private service payrolls. Declines were broad-based notably in retail

trade, educational services, and professional & tech services.

Also, in the government sector employment fell a sharp 53,000 (-0.6%

y/y as budgets shrank with lower tax revenues. The number of local

gov't jobs led the decline with a 37,000 (-0.9% y/y) drop. Jobs with

the federal government fell 5,000 (+1.9% y/y) for the third decline in

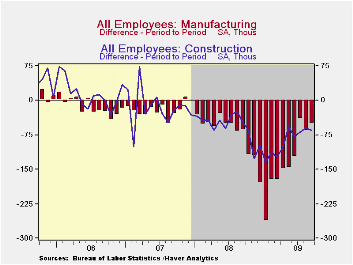

the last four months. Manufacturing sector jobs fell 51,000 last month

after a 66,000 July decline. These shortfalls compare to average

monthly declines of 131,000 this year. Construction jobs fell 64,000

and they fell an average 89,000 each month this year.

From the payroll survey, the quickening in the rate of job

loss last month was due to a faster 94,000 (-3.1% y/y) decline in

private service payrolls. Declines were broad-based notably in retail

trade, educational services, and professional & tech services.

Also, in the government sector employment fell a sharp 53,000 (-0.6%

y/y as budgets shrank with lower tax revenues. The number of local

gov't jobs led the decline with a 37,000 (-0.9% y/y) drop. Jobs with

the federal government fell 5,000 (+1.9% y/y) for the third decline in

the last four months. Manufacturing sector jobs fell 51,000 last month

after a 66,000 July decline. These shortfalls compare to average

monthly declines of 131,000 this year. Construction jobs fell 64,000

and they fell an average 89,000 each month this year.

The breath of the decline in payroll employment extended to 14.9% of industries during the last twelve months while it rose to 28.0% during the last three months.

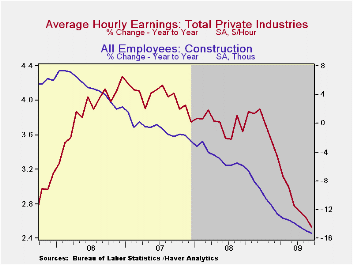

Average hourly earnings ticked up just 0.1% during September. That pulled the y/y gain down to 2.5% which was its weakest since late-2004, down from 4.2% reached during 2007. Earnings in the factory sector actually have improved recently and rose 0.7% (2.8% y/y). Growth in durable sector's earnings rose 0.7% and the y/y rate quickened to 3.7%. Earnings in the private service sector rose just 0.5% (2.7% y/y) while construction sector earnings fell 1.4% y/y.

The Labor Department offered a preliminary look at the

benchmark revision to the payroll data to be issued in February, 2010.

The revised data show that the level of payroll employment as of March

of 2009 will be lowered by 824,000, or 0.6%, from current published

numbers.

The Labor Department offered a preliminary look at the

benchmark revision to the payroll data to be issued in February, 2010.

The revised data show that the level of payroll employment as of March

of 2009 will be lowered by 824,000, or 0.6%, from current published

numbers.

The figures referenced above are available in Haver's USECON database. Additional detail can be found in the LABOR and in the EMPL databases.

Fed Policy in the Financial Crisis: Arresting the Adverse Feedback Loop from the Federal Reserve Bank of Dallas is available here.

| Employment: 000s | September | August | July | Y/Y | 2008 | 2007 | 2006 |

|---|---|---|---|---|---|---|---|

| Payroll Employment | -263 | -201 | -304 | -4.2% | -0.4% | 1.1% | 1.8% |

| Previous | -- | -216 | -276 | -- | -- | -- | -- |

| Manufacturing | -51 | -66 | -41 | -12.0% | -3.3% | -2.0% | -0.5% |

| Construction | -64 | -60 | -69 | -15.3% | -5.5% | -0.8% | 4.9% |

| Service Producing | -147 | -69 | -188 | -2.6% | 0.2% | 1.6% | 1.8% |

| Average Weekly Hours | 33.0 | 33.1 | 33.1 | 33.6 (Sept. '08) | 33.6 | 33.8 | 33.9 |

| Average Hourly Earnings | 0.1% | 0.4% | 0.3% | 2.5% | 3.8% | 4.0% | 3.9% |

| Unemployment Rate | 9.8% | 9.7% | 9.4% | 6.2% (Sept. '08) | 5.8% | 4.6% | 4.6% |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief