Global| Apr 07 2008

Global| Apr 07 2008U.S. Payrolls: Areas of Strength & Weakness

by:Tom Moeller

|in:Economy in Brief

Summary

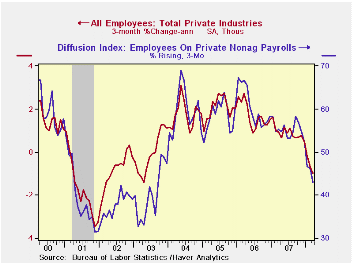

The latest three month's employment data show that hiring momentum has turned negative. The 0.7% annual rate of decline in nonfarm payrolls through March is down from positive growth of 1.1% last year and of 1.8% during 2006. Is a [...]

The latest three month's employment data show that hiring momentum has turned negative. The 0.7% annual rate of decline in nonfarm payrolls through March is down from positive growth of 1.1% last year and of 1.8% during 2006. Is a recession indicated? The latest numbers hardly measure up to those at the depths of the last two recessions. But they are indicative of the downward momentum at the start of the 2001 and the 1990 downturns.

With the measure showing that total hiring momentum down the Labor Department also provides a figure on just how far across industries the weakness spreads. Diffusion indexes measure that breadth of change amongst industry categories and on a three month basis, only 42.9% of payrolls were rising in March. In recession that figure falls into the 30-40% range, so it's close to giving a downturn signal.

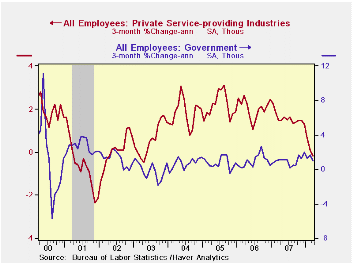

Of the 42.9%, virtually all of the employment gains have occurred in three of the categories listed in each month's data release: education & health, leisure & hospitality, and government. Within the first category, education payrolls have grown at a 4.0% rate during the last three months which is nearly double the growth from 2003 to 2007. Health care & social services payrolls also have grown at a roughly steady, firm 2.6% rate. In the second category, jobs in the leisure & hospitality sector also have grown recently but at a lesser 1.4% rate which is down from the 2.5% average growth during the last four years. Finally, in the government sector growth in payrolls has been limited to the state and local sectors. Federal government payrolls have been trending lower since 2003.

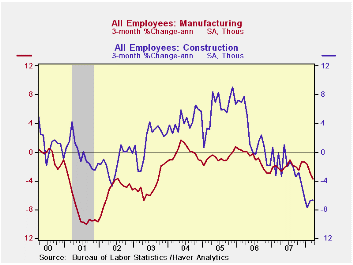

Construction sector jobs have suffered due to the fallout from the housing sector's decline. Within the total, residential sector jobs have lately been falling at an 11.3% rate. The depth of that rate of decline has been mitigated somewhat by just a 3.0% shortfall in commercial sector employment. Jobs amongst specialty trade contractors, by far the largest grouping in the construction total, have been falling at a 6.0% rate and by nearly double that rate in the residential subgroup.

In nearly all of the goods producing categories there has been job loss. The few exceptions are computers & peripherals, communications equipment and machinery. To the downside, job losses have been logged in the semiconductor, metals, electrical equipment, plastics and the paper industries. Most notable are the job losses in the motor vehicle, furniture, textile and the apparel industries where loss rates have been near or above double digit.

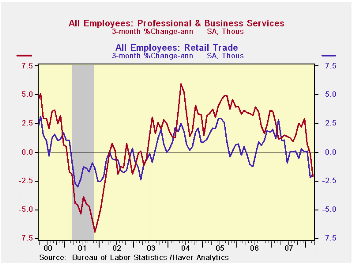

In the private service sector industries the rate of job creation also has been hit severely. Jobs have fallen hard in the retail trade sector, the information and in the financial service businesses. Additionally, cutbacks in real estate sector jobs aside from rental & leasing have been running at a 3.6% annual rate; a record rate of decline for this series which dates back only to 1990. Employment in the finance & insurance businesses has been ticking down at a 0.6% rate led by a 5.8% rate of decline in investment funds & trusts. That has been offset by payroll growth at commercial banks and securities & investment houses. Professional & business service service jobs have been falling at a 2.1% rate, the quickest since 2003. Jobs in temporary help agencies have plummeted at an 8.9% rate. The information sector also has lost jobs at a 1.1% rate over the last three months but jobs in motion pictures & sound recording have posted gains at a 5.5% rate.

The data behind the series in this report all can be found in Haver's USECON data base.

Population Aging, Labor Demand, and the Structure of Wages is a working paper from the Federal Reserve Bank of Boston and it can be found here.

| Employment: 000s | % of Total Payrolls | March (000) | 3-Month % (AR) | Y/Y % | 2007 (%) | 2006 (%) |

|---|---|---|---|---|---|---|

| Payroll Employment | -80 | -0.7 | 0.4 | 1.1 | 1.8 | |

| Private | 84 | -98 | -1.0 | 0.3 | 1.3 | 1.9 |

| Goods Producing Industries | 16 | -93 | -4.4 | -2.8 | -1.4 | 1.6 |

| Manufacturing | 10 | -48 | -3.7 | -2.2 | -1.9 | -0.5 |

| Construction | 5 | -51 | -6.6 | -4.6 | -1.0 | 4.9 |

| Service Producing Industries | 68 | -5 | -0.2 | 1.0 | 1.8 | 2.1 |

| Retail Trade | 12 | -12 | -1.9 | -0.7 | 0.9 | 0.5 |

| Information | 2 | -6 | -1.1 | -0.7 | -0.3 | -0.8 |

| Financial Activities | 6 | -5 | -1.2 | -1.3 | -0.2 | 2.2 |

| Real Estate, Rental & Leasing | 2 | -5 | -2.8 | -2.0 | -0.5 | 1.8 |

| Professional & Business | 13 | -35 | -2.1 | 0.9 | 2.2 | 3.7 |

| Education, Health & social services | 14 | 42 | 2.9 | 3.0 | 2.8 | 2.6 |

| Leisure & Hospitality | 10 | 18 | 1.4 | 2.5 | 2.8 | 2.3 |

| Government | 16 | 18 | 1.0 | 1.1 | 1.0 | 0.8 |

| Federal | 2 | 2 | -1.3 | -0.1 | -0.2 | -0.0 |

| State | 4 | 3 | 1.2 | 1.1 | 1.0 | 0.8 |

| Local | 10 | 13 | 1.3 | 1.3 | 1.3 | 0.9 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief