Global| Feb 06 2004

Global| Feb 06 2004U.S. Nonfarm Payrolls Disappoint Again

by:Tom Moeller

|in:Economy in Brief

Summary

Growth in nonfarm payrolls again missed expectations. The 112,000 rise in January was versus Consensus expectations for a 175,000 gain. It was the fifth consecutive monthly rise in payrolls. Increases during prior months were raised [...]

Growth in nonfarm payrolls again missed expectations. The 112,000 rise in January was versus Consensus expectations for a 175,000 gain. It was the fifth consecutive monthly rise in payrolls. Increases during prior months were raised somewhat but year to year payrolls remained down slightly.

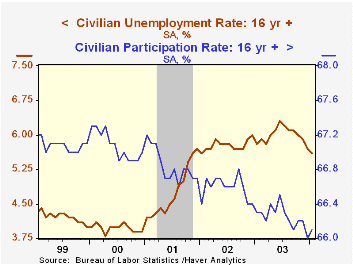

From the separate household survey, the unemployment rate fell to 5.6% versus expectations for an unchanged 5.7%.

Household employment rose 87,000 (+0.8% y/y) following a 54,000 decline in December. The labor force fell 15,000 (+0.7% y/y), the second consecutive down month. The labor force participation rate remained low at 66.1% versus 67.1% averaged from 1997-2000.

Manufacturing sector payrolls fell 11,000 (-3.6% y/y) following a little revised 27,000 decline in December. The one-month diffusion index for factory payrolls remained low at 38.1, continuing to suggest declines in factory payrolls over the near term.

Service producing payrolls rose 105,000 (0.1% m/m, 0.4% y/y). Jobs in retail trade gained back all of the prior two months' declines with a scattered 76,000 (0.1% y/y) increase. Jobs in the financial sector rose a paltry 2,000 (+0.8% y/y) following three months of decline. Temporary help services jobs fell 21,000 (6.0% y/y), the first monthly decline since April. Education & health services jobs rose 22,000 (2.0% y/y).

Construction jobs rose 24,000 (1.4% y/y). Government jobs fell for the third consecutive month (-0.4% y/y). By sector; federal government jobs fell 2.2% y/y, state jobs fell 0.4% y/y and local jobs fell 0.1% y/y.

The index of aggregate hours worked rose 0.8% and recouped most of the prior month's decline. Aggregate hours started 1Q up slightly from the 4Q average.

The one-month diffusion index for private non-farm payrolls dropped to 47.7% from 48.5 in 4Q, suggesting minimal employment growth

Average hourly earnings rose 0.1% (2.0% y/y). Earnings in the factory sector fell 0.6% (+2.3% y/y) as did construction sector earnings for the third month in four (+1.8% y/y).

| Employment | Jan | Dec | Y/Y | 2003 | 2002 | 2001 |

|---|---|---|---|---|---|---|

| Payroll Employment | 112,000 | 16,000 | -0.0% | -0.3% | -1.1% | 0.0% |

| Manufacturing | -11,000 | -27,000 | -3.6% | -4.8% | -7.2% | -4.8% |

| Average Weekly Hours | 33.7 | 33.5 | 33.8 | 33.7 | 33.8 | 34.0 |

| Average Hourly Earnings | 0.1% | 0.1% | 2.0% | 2.7% | 2.9% | 3.8% |

| Unemployment Rate | 5.6% | 5.7% | 5.8% | 6.0% | 5.8% | 4.8% |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief