Global| Dec 06 2007

Global| Dec 06 2007U.S. Mortgage Foreclosures: Conventional Up, Subprime Soared

by:Tom Moeller

|in:Economy in Brief

Summary

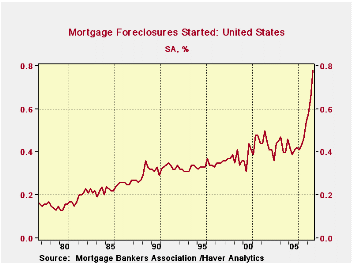

The Mortgage Bankers' Association today reported that foreclosures started on all mortgages rose to a still low 0.78% of mortgages outstanding. Nevertheless, that was by far the highest foreclosure rate on record. Foreclosure rates on [...]

The Mortgage Bankers' Association today reported that foreclosures started on all mortgages rose to a still low 0.78% of mortgages outstanding. Nevertheless, that was by far the highest foreclosure rate on record.

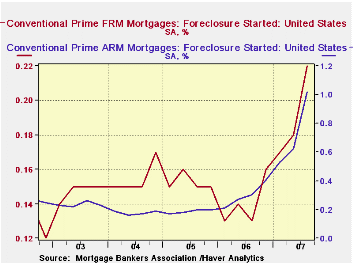

Foreclosure rates on both prime and subprime mortgages rose sharply. Rates for prime FRM rose to 0.22% of loans issued from 0.18% in 2Q and an average of 0.14% last year. 28 million loans were serviced.

Foreclosures on prime ARMs similarly rose to 1.02% from 0.62% and from 0.30% last year. 6 million of these loans were serviced.

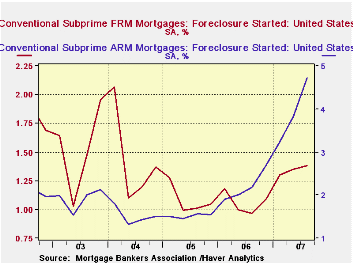

Foreclosures on subprime mortgage debt, however, rose much more sharply as employment growth slowed recently and interest rates rose. In total, foreclosures on subprime mortgages rose to 3.12% of outstanding loans. That amounted to 6 million loans. The rise was evenly spread between fixed and variable rate loans.

Foreclosures on subprime fixed rate debt rose to 1.38% of loans outstanding for a total of 3 million loans serviced.

On variable rate subprime debt, however, foreclosures soared to a 4.72% rate, up from 3.84% in 2Q and up from 2.0% last year. Three million loans were serviced.

The Rise and Fall of Subprime Mortgages from the Federal Reserve Bank of Dallas can be found here.

These data series are available in Haver's MBAMTG database.

| Mortgages in Foreclosure (%) | 3Q '07 | 2Q '07 | 3Q '06 | 2006 | 2005 | 2004 |

|---|---|---|---|---|---|---|

| All Mortgages | 0.78 | 0.65 | 0.46 | 1.84 | 1.64 | 1.73 |

| Conventional Prime | 0.37 | 0.27 | 0.19 | 0.77 | 0.72 | 0.77 |

| Fixed Rate | 0.22 | 0.18 | 0.13 | 0.14 | 0.15 | 0.16 |

| ARM | 1.02 | 0.62 | 0.30 | 0.30 | 0.19 | 0.18 |

| Subprime | 3.12 | 2.72 | 1.82 | 7.23 | 5.66 | 5.98 |

| Fixed Rate | 1.38 | 1.35 | 0.97 | 1.06 | 1.08 | 1.44 |

| ARM | 4.72 | 3.84 | 2.19 | 2.20 | 1.52 | 1.52 |

by Tom Moeller December 6, 2007

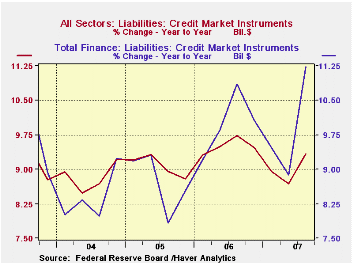

Credit market debt outstanding owed by all sectors of the economy grew 11.0% (AR, 9.3% y/y) during the third quarter. The increase was the strongest since 4Q 2005 and reflected broad based, strong gains in the financial sector..

Credit market debt owed by the financial sector zoomed at a

16.5% (11.2% y/y) annual rate which was the strongest rate of gain

since early 2001. Gains at commercial banks (41.0% y/y), bank holding

companies (23.2 y/y), savings institutions (-8.8% y/y) and credit

unions (68.9% y/y) were well into double or triple digit rates of

growth.

Stable was consumer credit growth which held at an 8.2% (7.8% y/y) quarterly rate of growth. Households' obligations on home mortgages grew 7.3% (8.0% y/y) which was half the growth rates seen a few years back. Conversely, credit card debt rose sharply (5.3% y/y) and the quarterly growth rate of 10.3% was the quickest since 2004. Bank loans also surged.

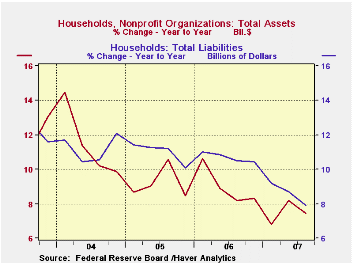

The net worth of the US household sector last quarter improved to a record $58.604 trillion as the dollar gain in household sector assets, which totaled 72.8 trillion, outweighed by four times the growth of liabilities which total $14.1 trillion.

Total assets of households and nonprofit organizations grew at a 4.9% rate (7.4 y/y). Households' ownership of real estate assets was much reduced to a 2.1% growth rate (4.3% y/y), the slowest rate of gain since 1993. That, however, was offset by a 6.4% (9.5% y/y) gain in financial assets led by a one-quarter (7.2% y/y) rise in the value of credit market instruments and a rise in the value of mutual fund share holdings (21.8% y/y). The value of money market shares rose by one third as assets were shifted to a safe haven (24.5% y/y).

| Flow of Funds (Y/Y Chg.) | % of Total | 3Q'07 | 2Q'07 | 2006 | 2005 | 2004 |

|---|---|---|---|---|---|---|

| Total Credit Market Debt Outstanding | -- | 9.3% | 8.7% | 9.5% | 8.8% | 9.2% |

| Federal Government | 12% | 4.3% | 3.0% | 3.9% | 7.0% | 9.0% |

| Households | 27% | 7.8% | 8.2% | 10.3% | 10.7% | 11.5% |

| Nonfinancial Corporate Business | 14% | 11.0% | 9.8% | 8.4% | 5.1% | 3.5% |

| Financial Sectors | 32% | 11.2% | 8.9% | 10.1% | 8.5% | 9.2% |

| Net Worth: Households & Nonprofit Organizations (Trillions) | -- | $58.604 | $57.979 | $56.117 | $52.061 | $48.164 |

| Tangible Assets: Households | -- | $27.484 | $27.325 | $26.671 | $25.019 | $22.464 |

| Financial Assets: Households | -- | $45.277 | $44.579 | $42.880 | $39.203 | $36.747 |

by Tom Moeller December 6, 2007

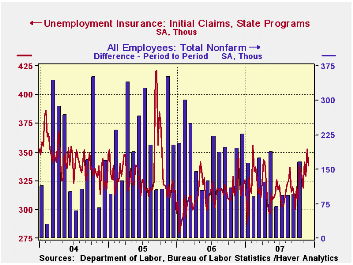

Last week, initial claims for jobless insurance retraced most of the prior period's surge. The 15,000 worker decline to 338,000 followed a little revised increase of 24,000.

The four week moving average of initial claims, a measure which smoothes out most of the series' w/w volatility, rose to 340,250 (4.0% y/y). That was the highest level since 2005.

A claims level below 400,000 typically has been associated with growth in nonfarm payrolls. During the last six years there has been a (negative) 78% correlation between the level of initial claims and the m/m change in nonfarm payroll employment.

By state, some of the largest increases in the four week

average level of claims were in New Jersey, California, &

Indiana, each to or near to the highest level since 2003. Other states

with large increases recently were Florida, Ohio and Pennsylvania.

These detailed claims figures by state are in Haver's Regional Weekly database.

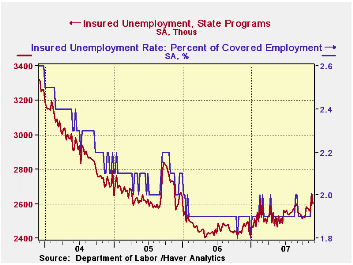

Continuing claims for unemployment insurance fell 59,000 after the 104,000 surge during the prior week. That gain was revised down only slightly from the initial report.

The continuing claims numbers lag the initial claims figures by one week.

The insured rate of unemployment held at 2.0% after the prior week's increase.

The 'Great Moderation' in Output and Employment Volatility: An Update from the Federal Reserve Bank of Dallas is available here.

| Unemployment Insurance (000s) | 12/01/07 | 11/24/07 | Y/Y | 2006 | 2005 | 2004 |

|---|---|---|---|---|---|---|

| Initial Claims | 338 | 353 | 4.6% | 313 | 331 | 343 |

| Continuing Claims | -- | 2,559 | 4.6% | 2,459 | 2,662 | 2,924 |

by Robert Brusca December 6, 2007

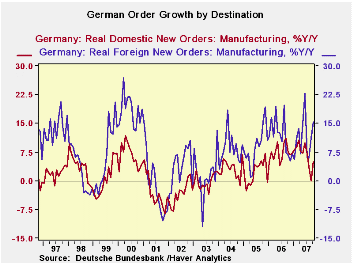

German orders jumped in October rising by 4% after an upward

revised drop of 1.6% in Sept. The gain saw the domestic orders

component rise by 2.7% as foreign orders rose by 5%. Foreign orders are

now rising at a 33% pace over three months and clearly accelerating

while domestic orders post a slightly stronger three month growth rate

of 2.9%. Sales of consumer and intermediate goods remain weak while

capital goods sales surged in October.

Order detail shows that bulk orders account for the surge in

October. Bulk orders were behind the 8.1% surge in investment goods

orders that saw domestic investment goods orders rise by 6.4% and

foreign orders rise by 9.4%. Basic goods orders fell by 0.4% in October

and consumer goods order volumes fell by 0.8%. Orders from outside the

Euro Area increased by 4.2% while Ex-German Euro Area orders rose by a

sharp 6%.

For the quarter underway orders are not tremendously strong

with overall orders rising at an annual rate that exceeds 20%.

On balance German institutes are still cutting their forecasts

for 2008. The chart (above) shows that even with this new surge, orders

are in lower trajectory than they were in their hey-day. It is unclear

what this surge means for the outlook. It may be a fluke of orders

clumping since most other measures continue to show slowing. I do not

think it is a revival.

| German Orders and Sales By Sector and Origin | |||||||

|---|---|---|---|---|---|---|---|

| Real and SA | % M/M | % Saar | |||||

| Oct-07 | Sep-07 | Aug-07 | 3-MO | 6-Mo | 12-Mo | Yr Ago | |

| Total Orders | 4.0% | -1.6% | 1.9% | 17.9% | 8.6% | 10.3% | 7.1% |

| Foreign | 5.0% | -0.8% | 3.2% | 33.6% | 15.6% | 15.5% | 6.7% |

| Domestic | 2.7% | -2.4% | 0.4% | 2.9% | 1.4% | 5.1% | 7.4% |

| Sector Sales | |||||||

| MFG/Mining | 1.2% | -0.3% | 1.3% | 9.2% | 4.5% | 6.6% | 6.4% |

| Consumer | 0.2% | -0.3% | 1.7% | 6.8% | 3.3% | 1.9% | 2.9% |

| Consumer Durables | -1.7% | -4.0% | 4.2% | -6.8% | -3.4% | -0.9% | 7.8% |

| Consumer Nondurables | 0.6% | 0.5% | 1.2% | 9.5% | 4.7% | 2.5% | 2.0% |

| Capital Goods | 3.4% | -0.2% | 1.1% | 18.2% | 8.7% | 9.9% | 7.2% |

| Intermediate Goods | -0.7% | -0.2% | 1.3% | 1.3% | 0.7% | 5.6% | 7.5% |

| All Manufacturing Sales | 1.2% | -0.2% | 1.3% | 9.7% | 4.7% | 6.4% | 5.8% |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief