Global| Aug 06 2008

Global| Aug 06 2008U.S. Mortgage Applications Down By One-third

by:Tom Moeller

|in:Economy in Brief

Summary

The total number of mortgage applications ticked up 2.8% last week, but that followed two weeks of sharp decline, according to the Mortgage Bankers Association. As a result, applications in early August were 11.1% below the July [...]

The total number of mortgage applications ticked up 2.8% last week, but that followed two weeks of sharp decline, according to the Mortgage Bankers Association. As a result, applications in early August were 11.1% below the July average. In July, applications fell 2.9% from June following sharper m/m declines during most of this year.

In early August, the level of all mortgage applications was down by one-third from the year-ago level.

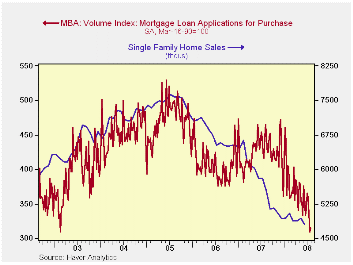

Purchase applications fell 1.8% last week which made up just a

piece of the prior three weeks' sharp declines. That left applications

for a mortgage to purchase a home, early this month, 8.0% below the

July average.

During the last ten years there has been a 61% correlation between the y/y change in purchase applications and the change in new plus existing single family home sales.

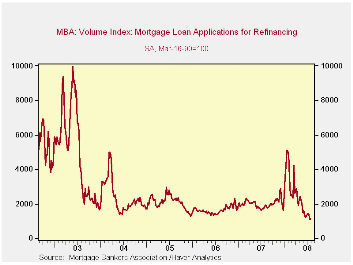

Applications to refinance a home mortgage rose 4.4% after two weeks of strong decline. Applications began this month 15.7% below the July average.

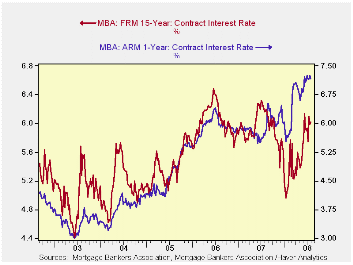

The effective interest rate on a conventional 15-year mortgage ticked up w/w to 6.02% after two months when they averaged 5.94%. For a thirty year mortgage, rates were little changed at 6.41%. Interest rates on 15 and 30 year mortgages are closely correlated (>90%) with the rate on 10-year Treasury securities. For an adjustable rate 1-Year mortgage the rate slipped to 7.17% from a 7.20% average last month.

During the last ten years there has been a (negative) 79%

correlation between the level of applications for purchase and the

effective interest rate on a 30-year mortgage.

The Mortgage Bankers Association surveys between 20 to 35 of the top lenders in the U.S. housing industry to derive its refinance, purchase and market indexes. The weekly survey covers roughly 50% of all U.S. residential mortgage applications processed each week by mortgage banks, commercial banks and thrifts. Visit the Mortgage Bankers Association site here.

The Rise and Fall of Subprime Mortgages from the Federal Reserve Bank of Dallas can be found here.

| MBA Mortgage Applications (3/16/90=100) | 08/01/08 | 07/25/08 | Y/Y | 2007 | 2006 | 2005 |

|---|---|---|---|---|---|---|

| Total Market Index | 432.6 | 420.8 | -34.1% | 652.6 | 584.2 | 708.6 |

| Purchase | 315.2 | 309.5 | -29.5% | 424.9 | 406.9 | 470.9 |

| Refinancing | 1,121.8 | 1,074.4 | -40.4% | 1,997.9 | 1,634.0 | 2,092.3 |

by Robert Brusca August 6, 2008

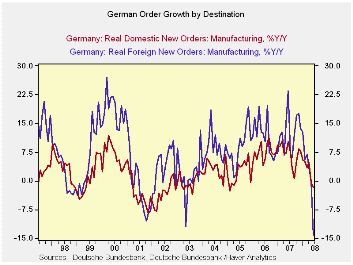

Historically German foreign

orders have been the more volatile

of the two series (foreign and domestic orders for MFG goods). The

current drop is a steep one indeed. The aggressive growth rates show

that growth fore both domestic and foreign orders is getting weaker as

the time period to calculated growth gets shorter. This is accelerating

weakness.

Historically German foreign

orders have been the more volatile

of the two series (foreign and domestic orders for MFG goods). The

current drop is a steep one indeed. The aggressive growth rates show

that growth fore both domestic and foreign orders is getting weaker as

the time period to calculated growth gets shorter. This is accelerating

weakness.

Quarter-to-date the growth rates are terribly weak. This

series is now complete for Q2. In Q2 total orders are falling at a

15.4% annual lead by a 21.3% drop in Foreign orders. Sales are falling

too as Consumer sales are off at an 11% pace even capital goods real

sales are off at a 5.8% annual rate in the quarter. The German

economy’s factory sector is weakening at a rapid pace.

| German Orders and Sales By Sector and Origin | ||||||||

|---|---|---|---|---|---|---|---|---|

| Real and SA | % M/M | % Saar | ||||||

| Jun-08 | May-08 | Apr-08 | 3-Mo | 6-Mo | 12-Mo | Yr Ago | QTR-2-Date | |

| Total Orders | -2.9% | -1.4% | -1.7% | -21.7% | -11.5% | -8.4% | 16.9% | -15.4% |

| Foreign | -5.1% | 0.1% | -3.7% | -30.0% | -16.3% | -14.1% | 23.4% | -21.3% |

| Domestic | -0.6% | -2.8% | 0.3% | -11.9% | -6.1% | -1.7% | 10.2% | -8.8% |

| Real Sector Sales | ||||||||

| MFG/Mining | -0.6% | -0.4% | -1.0% | -7.7% | -3.9% | 2.1% | 5.9% | -7.2% |

| Consumer | -1.6% | 0.2% | -2.0% | -12.8% | -6.6% | -2.9% | 2.2% | -11.0% |

| Consumer Durables | 2.0% | -3.7% | 1.1% | -2.8% | -1.4% | -1.7% | 4.6% | -5.7% |

| Consumer Non-Durable | -2.2% | 1.1% | -2.6% | -14.0% | -7.2% | -3.1% | 1.7% | -11.8% |

| Capital Goods | 0.9% | -2.7% | 2.1% | 0.9% | 0.4% | 4.5% | 7.3% | -5.8% |

| Intermediate Goods | -2.0% | 2.0% | -4.0% | -15.3% | -8.0% | 1.6% | 6.5% | -7.0% |

| All MFG-Sales | -0.7% | -0.5% | -1.0% | -8.4% | -4.3% | 1.5% | 5.8% | -7.7% |

by Robert Brusca August 6, 2008

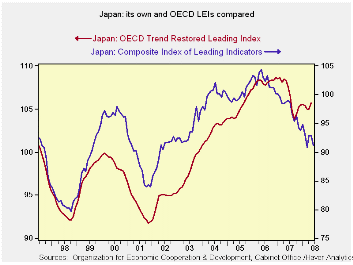

Japan’s leading economic index fell in June after having a

small uptick in May. Over three-months the index is higher but it is

deeply weaker over 24-, 12- and 6-months. The OECD index that is not

quite as up-to-date has been pointing to strength since late 2007.

The Cabinet Office reported that the trend in the composite

coincident index points to a worsening of the economic cycle,

downgrading the view a month earlier that suggested a possible change

in the business cycle. The coincident index, which measures the current

state of the economy, fell sharply to 101.7 from 103.3, in line with

expectations. The leading index signals are not so clear cut with the

OECD’s and Japan’s own indicators pointing in very different directions

– a most unusual development.

| Japan's LEI and its trends | |||||||

|---|---|---|---|---|---|---|---|

| Levels | Growth (saar) | ||||||

| Jun-08 | May-08 | Apr-08 | 3Mo | 6Mo | 12Mo | 24Mo | |

| LEI | 91.2 | 92.9 | 92.8 | 1.8% | -5.5% | -8.0% | -11.5% |

| LEI: OECD | #N/A | 105.7 | 104.9 | 1.1% | 0.9% | -2.4% | -1.1% |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief