Global| Aug 23 2007

Global| Aug 23 2007U.S. Loan Delinquencies Up Slightly, But Still Low

by:Tom Moeller

|in:Economy in Brief

Summary

For all the media hype regarding the "subprime" loan issuance problem, the latest data issued by the Federal Reserve Board for 2Q07 indicate only slight increases in delinquent payments on consumer, real estate and commercial & [...]

For all the media hype regarding the "subprime" loan issuance problem, the latest data issued by the Federal Reserve Board for 2Q07 indicate only slight increases in delinquent payments on consumer, real estate and commercial & industrial loans at commercial banks.

Even if delinquencies rise further this quarter (which they probably will), the levels are still quite low absolutely and relative to historical comparison, i.e., relative to the late 1980s and the early 1990s.

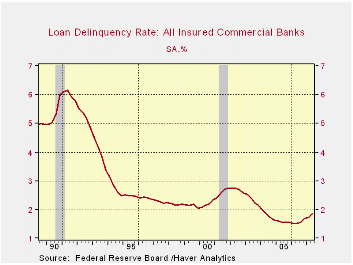

For all loans and leases, the delinquency rate increased to 1.86% during the second quarter from 1.72% during 1Q07. That level is up versus 1.57% during the prior two years but, still, it is only a third of the delinquency rate during the last two recessions.

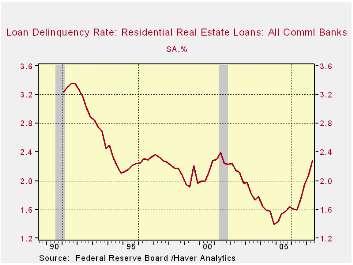

The rise in delinquent payments on residential real estate loans indeed is more dramatic to 2.28% from 2.07% in 1Q07. It is equal to where it was during the last recession. Yet these figures are below the high seen in 1991 of 3.32%. Again, these comments await the update for this quarter.

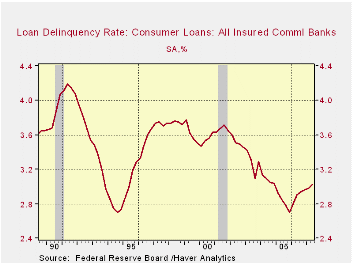

For consumer loans, the delinquency rate rose to 3.02% from 2.98% during 1Q. That's up from the 2005 low of 2.82%, but down from the highs during the last two recessions. It's lower even than the 3.75% range that prevailed during the late 1990s expansion.

Delinquencies on C&I loans actually fell q/q to 1.17% from 1.18% during 1Q. Delinquent C&I loans last year averaged 1.27% of the total outstanding.

These data series are available in Haver's USECON database.

Subprime Mortgages is recent Congressional testimony delivered by Sandra F. Braunstein of the Federal Reserve Board and it is available here.

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief