Global| Feb 22 2008

Global| Feb 22 2008U.S. Loan Delinquencies Up Across the Board

by:Tom Moeller

|in:Economy in Brief

Summary

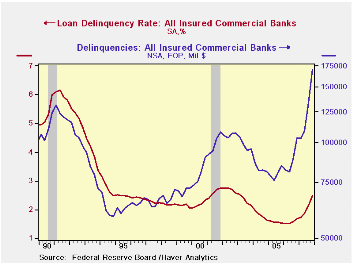

During 4Q 2007, the Federal Reserve Board Reported that the delinquency rate on all consumer loan & leases jumped to 2.49% from 2.13% during the third quarter. The latest reading was the highest since early 2003, but that performance [...]

During 4Q 2007, the Federal Reserve Board Reported that the delinquency rate on all consumer loan & leases jumped to 2.49% from 2.13% during the third quarter. The latest reading was the highest since early 2003, but that performance masks some the real troubles being had in making payments.

The dollar value of these loans totaled a record $170 billion last quarter, more than double the level at the recent low during 2005.

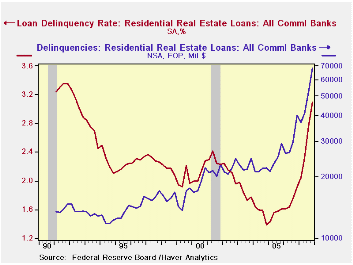

Driving the rise were delinquent payments on residential real estate loans. Delinquent payments on residential real estate loans surged to 3.09% of the loans extended. The current rate is the highest since 1991. Delinquencies on commercial real estate loans, which had been relatively current, jumped. The rate of 2.71% was the highest since late 1996 with a delinquency rate of 2.71%.

The dollar value of those delinquent residential real estate loans jumped to $68.4 billion (+71.2% y/y), more than four times the level ten years ago and 40% of the dollar value of late payments on banks' books.

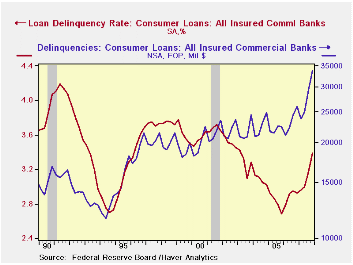

Delinquent payments on consumer loans also rose sharply to a 3.39% rate versus 3.13% for the full year 2007. Delinquent payments on credit card debt rose to 4.55%, 4.25% for the whole year. The rise for credit card debt was larger from the low of 3.52% late in 2005.End of the Credit Line is a 2006 article from the Federal Reserve Bank of Minneapolis and it can be found here.

The dollar value of those delinquent credit card payments amounted to $17.4 brillion, nearly triple the low in 1993.

Delinquencies on C&I loans rose slightly q/q to 1.35% from 1.23% during 3Q, up slightly from 2006 but down from years prior.The dollar values of these loans amounted to $18.1 trillion during 4Q, up by more than one third from one year prior.

These data series are available in Haver's USECON database.

Another Widow: The Term Auction Facility from the Federal Reserve Bank of St. Louis is available here.

| Loan Delinquency Rate (%) | 4Q '07 | 3Q '07 | 4Q '06 | 2007 | 2006 | 2005 |

|---|---|---|---|---|---|---|

| Total Loan & Leases | 2.49 | 2.13 | 1.68 | 2.06 | 1.57 | 1.56 |

| Consumer Loans | 3.39 | 3.17 | 2.93 | 3.13 | 2.90 | 2.81 |

| Credit Cards | 4.55 | 4.34 | 3.92 | 4.25 | 4.01 | 3.70 |

| Real Estate Loans | 2.88 | 2.40 | 1.67 | 2.27 | 1.48 | 1.37 |

| Residential | 3.09 | 2.75 | 1.91 | 2.55 | 1.73 | 1.55 |

| Commercial | 2.71 | 1.98 | 1.32 | 1.94 | 1.13 | 1.07 |

| Commercial & Industrial Loans | 1.35 | 1.23 | 1.17 | 1.23 | 1.27 | 1.51 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.