Global| Feb 02 2005

Global| Feb 02 2005U.S. Light Vehicle Sales Fell Sharply

by:Tom Moeller

|in:Economy in Brief

Summary

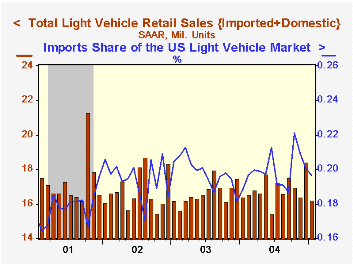

Unit sales of light vehicles in January matched Consensus expectations and gave back all of the prior month's jump with an 11.6% decline to 16.26M. Sales of light trucks dropped 12.2% as sales of domestics skid 12.8% m/m (-4.2% y/y) [...]

Unit sales of light vehicles in January matched Consensus expectations and gave back all of the prior month's jump with an 11.6% decline to 16.26M.

Sales of light trucks dropped 12.2% as sales of domestics skid 12.8% m/m (-4.2% y/y) and imports fell 8.2% (+1.7% y/y).

Total auto sales fell 10.9% m/m paced by a 14.6% (+6.8% y/y) drop in imports. Sales of domestic autos slid 9.5% (+1.5% y/y).

Imports' share of the US market for new vehicles fell slightly to 19.9% in January, about the same as last year's average.

| Light Vehicle Sales (SAAR, Mil. Units) | Jan | Dec | Y/Y | 2004 | 2003 | 2002 |

|---|---|---|---|---|---|---|

| Total | 16.26 | 18.40 | -0.7% | 16.88 | 16.63 | 16.81 |

| Autos | 7.39 | 8.30 | 2.9% | 7.49 | 7.62 | 8.07 |

| Trucks | 8.87 | 10.11 | -3.5% | 9.39 | 9.01 | 8.74 |

by Tom Moeller February 2, 2005

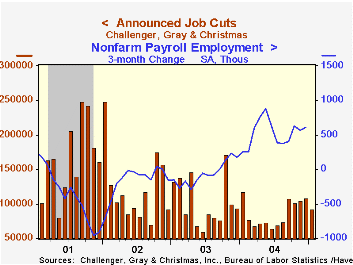

Challenger, Gray & Christmas reported that job cut announcements in January dropped 15.3% m/m to the lowest level since August.

During the last ten years there has been an 85% (inverse) correlation between the three month moving average of announced job cuts and the three month change payroll employment.

Reductions of job cut announcements were widespread across industries last month except in apparel (+86.2% y/y), computers (+167.0% y/y), electronics (+400.9% y/y), financial (-26.0% y/y), services (-0.6% y/y) and government (+81.0% y/y).

Job cut announcements differ from layoffs. Many are achieved through attrition, early retirement or just never occur.

| Challenger, Gray & Christmas | Jan | Dec | Y/Y | 2004 | 2003 | 2002 |

|---|---|---|---|---|---|---|

| Announced Job Cuts | 92,351 | 109,045 | -21.4% | 1,039,175 | 1,236,426 | 1,431,052 |

by Tom Moeller February 2, 2005

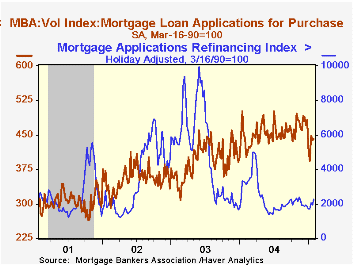

Mortgage applications recovered 7.3% last week but the average level in January remained below the December average by 1.9% according to the Mortgage Bankers Association (MBA) Survey.

Applications to refinance jumped 16.6% w/w and that was enough to pull the January average 8.0% ahead of December.

Purchase applications rose a slight 0.3% w/w and the January average fell 8.6% below December. During the last ten years there has been a 59% correlation between the y/y change in purchase applications and the change in new plus existing home sales.

The effective interest rate on a conventional 30-year mortgage rose slightly to 5.86% versus an average 6.05% during 2004 and 5.95% in December. The effective rate on a 15-year mortgage also rose to 5.42% last week.

The Mortgage Bankers Association surveys between 20 to 35 of the top lenders in the U.S. housing industry to derive its refinance, purchase and market indexes. The weekly survey accounts for more than 40% of all applications processed each week by mortgage lenders. Visit the Mortgage Bankers Association site here.

| MBA Mortgage Applications (3/16/90=100) | 01/28/05 | 01/21/05 | Y/Y | 2004 | 2003 | 2002 |

|---|---|---|---|---|---|---|

| Total Market Index | 706.4 | 658.1 | -17.4% | 735.1 | 1,067.9 | 799.7 |

| Purchase | 440.3 | 439.0 | -0.8% | 454.5 | 395.1 | 354.7 |

| Refinancing | 2,253.9 | 1,932.8 | -30.7% | 2,366.8 | 4,981.8 | 3,388.0 |

by Tom Moeller February 2, 2005

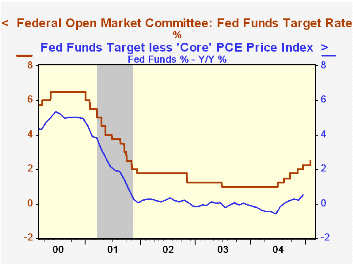

As expected the Federal Open Market Committee raised the target rate for federal funds by 25 basis points to 2.50%. The discount rate also was raised 25 basis points to 3.50%.

The decision was unanimous and it was the sixth increase since last June.

Today's press release from the Fed continued to contain a comment suggesting that rates could be raised again. "The Committee believes that, even after this action, the stance of monetary policy remains accommodative and, coupled with robust underlying growth in productivity, is providing ongoing support to economic activity."

For the complete text of the Fed's latest press release please click here.

A Neutral Fed Funds Rate from the Federal Reserve Bank of St. Louis is available here.

Comparing Forecast-Based and Backward-Looking Taylor Rules: A "Global" Analysis from the Federal Reserve Bank of New York can be found here.

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief