Global| May 17 2007

Global| May 17 2007U.S. LEI Weakness in April… One Trick Pony

Summary

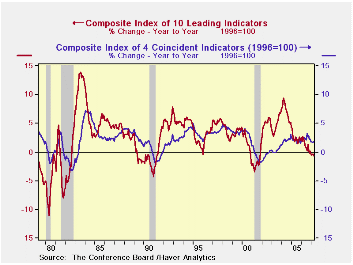

The LEI is increasing its year/year pace of decline and is now falling by 0.7% year/year. However, a brief look at history shows that the current combination of a weak LEI and weak coincident index is not producing a weakening at a [...]

The LEI is increasing its year/year pace of decline and is now falling by 0.7% year/year. However, a brief look at history shows that the current combination of a weak LEI and weak coincident index is not producing a weakening at a pace that signals recession. They are weakening more like they did in 1995, but not even as severely as that…and there is less weakening power in the pipeline that it seems.

Periods in which the coincident index is growing more slowing than the leading index do tend to be slowdown periods. But not all of them become recession periods. Some of them are extended periods that eventually transition into recession. Only the aftermath of the 1995 episode left a good solid period of growth in its wake.

While the LEI has dropped to a weaker growth rate on year/year measures, this is not a period with increased downward momentum in general. The 3-month and 6-month rates of growth are not getting progressively lower. The six month rate speeded up but the three-month rate is the one that has fallen sharply. Over the same recent three-months the coincident index has speeded up slightly. The LEI has been very flat so that there is really little in the way for further declines in the pipeline from one-year ago. May of 2006 was weaker than April of that year implying that the year/year LEI will be lower by only 0.2% year/year unless it falls further in May. Even the three-month growth rate (annualized) is not set for further weakness despite its relatively sharp drop in April. If the LEI is unchanged next month it will rise in May over the next three-month period, not fall.

Apart from these technical considerations there are the economic data that have begun to show a bit more strength.

The LEI is falling. Its rate of decline has accelerated this month. But there does not appear to be an ongoing process here nor does the rate of descent appear to be particularly disturbing.

| LEADING | COINCIDENT | LAGGING | |

| Month-to-month | |||

| Apr-07 | -0.5% | 0.2% | 0.2% |

| Mar-07 | 0.6% | 0.1% | 0.0% |

| Feb-07 | -0.6% | 0.2% | 0.2% |

| Jan-07 | -0.3% | -0.1% | -0.1% |

| SAAR | |||

| 3-Mos | -2.0% | 1.6% | 1.6% |

| 6-Mos | -0.4% | 1.3% | 3.7% |

| 12-Mos | -0.7% | 1.7% | 3.3% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief