Global| Sep 21 2009

Global| Sep 21 2009U.S. Leading Indicators Rise For AFifth Straight Month And Signal Economic Recovery

by:Tom Moeller

|in:Economy in Brief

Summary

The Conference Board's Index of Leading Economic Indicators continued to suggest a pending economic recovery with a 0.6% August increase that was close to expectations. The rise in the composite index of leaders was the fifth in a row [...]

The

Conference Board's Index of Leading Economic Indicators continued to

suggest a pending economic recovery with a 0.6% August increase that

was close to expectations. The rise in the composite index of leaders

was the fifth in a row and the 4.7% increase during those five months

was the strongest since early-1983. The index itself was at the highest

level since January of last year. The leading index is based on actual

reports for eight economic data series. The Conference Board initially

estimates two series, orders for consumer goods and orders for capital

goods.

The

Conference Board's Index of Leading Economic Indicators continued to

suggest a pending economic recovery with a 0.6% August increase that

was close to expectations. The rise in the composite index of leaders

was the fifth in a row and the 4.7% increase during those five months

was the strongest since early-1983. The index itself was at the highest

level since January of last year. The leading index is based on actual

reports for eight economic data series. The Conference Board initially

estimates two series, orders for consumer goods and orders for capital

goods.

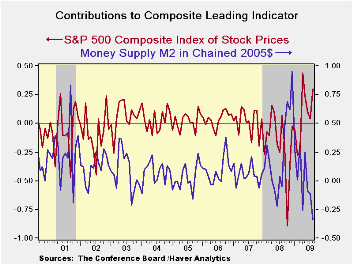

Perhaps tempering the outlook was that the 0.6% August increase in the leaders was the weakest of the last five months. Moreover, a slightly diminished 60% of the index components rose. Higher stock prices and a steeper interest rate yield curve, along with a slower speed of vendor deliveries, made the largest positive contributions to the latest overall increase in the leaders. However, the real money supply fell for the fourth month in the last five and average weekly factory hours worked were unchanged as were new orders for consumer goods & materials.

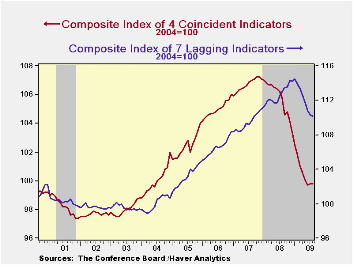

Continuing

to

suggest that the rate of decline in the economy is slowing were the

coincident indicators. They were unchanged during August after a slim

0.1% July gain. While hardly indicative of a robust economy, these

declines compare with monthly shortfalls of 0.6%-to-1.1% dating back to

September. Fostering the turnaround have been slight increases in

industrial production and real personal income as well as diminished

monthly declines in payrolls.

Continuing

to

suggest that the rate of decline in the economy is slowing were the

coincident indicators. They were unchanged during August after a slim

0.1% July gain. While hardly indicative of a robust economy, these

declines compare with monthly shortfalls of 0.6%-to-1.1% dating back to

September. Fostering the turnaround have been slight increases in

industrial production and real personal income as well as diminished

monthly declines in payrolls.

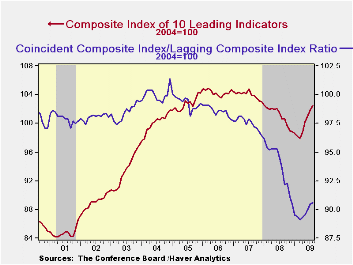

Wringing out past economic

excesses is needed for real economic recovery. In a further sign that

excesses in the U.S. economy are diminishing, the lagging index fell

for the eight month in the last nine. To that point, C&I loans

outstanding fell sharply for the ninth straight month and consumer

credit versus personal income was off for the fifth month this year. Regardless, the average duration of unemployment shortened and the

change in CPI for services eased. The ratio of coincident-to-lagging

indicators (a measure of economic excess) also continued higher for the

fifth straight month to the highest level since November.

Regardless, the average duration of unemployment shortened and the

change in CPI for services eased. The ratio of coincident-to-lagging

indicators (a measure of economic excess) also continued higher for the

fifth straight month to the highest level since November.

The Conference Board figures are available in Haver's BCI database. Visit the Conference Board's site for coverage of leading indicator series from around the world.

Beyond Inflation Targeting: Should Central Banks

Target the Price Level? from the Federal Reserve Bank

of Kansas City is available here.

How Will Unemployment Fare Following the Recession? also from the Federal Reserve Bank of Kansas City can be found here.

| Business Cycle Indicators (%) | August | July | June | May 6-Month % (AR) | 2008 | 2007 | 2006 |

|---|---|---|---|---|---|---|---|

| Leading | 0.6 | 0.9 | 0.8 | 6.2 | -2.8 | -0.3 | 1.5 |

| Coincident | 0.0 | 0.1 | -0.4 | -5.4 | -0.9 | 1.6 | 2.5 |

| Lagging | -0.1 | -0.5 | -0.9 | -8.6 | 2.9 | 2.8 | 3.3 |

by Tom Moeller September 21, 2009

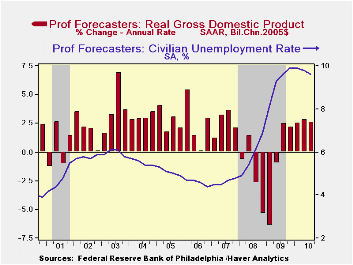

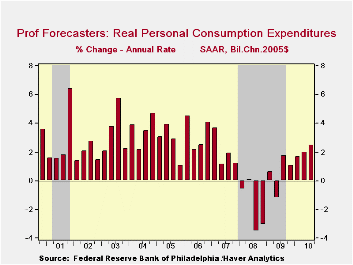

Each

quarter, the Federal Reserve Bank of Philadelphia surveys a group of

professional forecasters to gain perspective on the outlook for the

U.S. economy. In the August survey, the panel expected the recession to

have reached its end, though the recovery is expected to be subpar.

That subpar nature is expected to keep unemployment high but it is not

expected to prevent inflation and interest rates from rising.

Each

quarter, the Federal Reserve Bank of Philadelphia surveys a group of

professional forecasters to gain perspective on the outlook for the

U.S. economy. In the August survey, the panel expected the recession to

have reached its end, though the recovery is expected to be subpar.

That subpar nature is expected to keep unemployment high but it is not

expected to prevent inflation and interest rates from rising.

Just 2.4% growth in real GDP is expected during the current quarter to be followed by growth at about that rate into next year. That follows the 3.9% y/y drop in real GDP through last quarter, which was the deepest decline since the Great Depression. Indeed, this recovery is subpar compared to prior periods of severe recession. Following the 1973-75 recession, when GDP fell at a peak y/y rate of 2.3%, growth shortly rebounded to 6.2%. Similarly following the 1981-82 recession, when GDP fell 2.7% y/y, a snapback came quickly at near an 8% rate.

The subpar nature of the coming economic

recovery stems very much from the consumer who remains burdened by

excessive levels of debt.

A swing towards inventory accumulation also should play a part in the pending economic recovery, yet here again it's not a huge part. Accumulation at near a $20 billion annual rate is expected by the end of next year. Certainly that is improved from the peak rate of decumulation of $141 last quarter, and the dollar swing is impressive. But as a percentage of the economy's overall real size it amounts to barely half the swing after prior severe recessions. As for the foreign trade deficit, recent improvement has helped forestall an even deeper decline in U.S. GDP during this recession. However, that improvement is expected to now end with little or no improvement through next year as foreign economies remain weak.

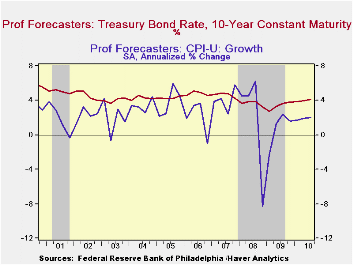

Weak

economic growth is expected to do little reduce unemployment. The

unemployment rate is expected to average 9.9% and then dip just to 9.6%

by next year's third quarter.  These rates are the highest jobless rates

since 1982-83 and reflect little or no growth in expected employment.

Pricing power is thus expected to be severely constrained. The y/y

growth in the overall GDP price deflator is expected to drift up to

1.5% from its low of 1.0% this year. Perhaps not-so-surprisingly,

forecasters expect that lift to stem from a liquidity-driven rise in

core consumer prices to 1.6% from a low of 1.1% being reached now.

Ten-year Treasury yields are expected to rise in tandem to highs near

4% by the middle of next year.

These rates are the highest jobless rates

since 1982-83 and reflect little or no growth in expected employment.

Pricing power is thus expected to be severely constrained. The y/y

growth in the overall GDP price deflator is expected to drift up to

1.5% from its low of 1.0% this year. Perhaps not-so-surprisingly,

forecasters expect that lift to stem from a liquidity-driven rise in

core consumer prices to 1.6% from a low of 1.1% being reached now.

Ten-year Treasury yields are expected to rise in tandem to highs near

4% by the middle of next year.

The full Third Quarter 2009 Survey of Professional Forecasters from the Federal Reserve Bank of Philadelphia is available here

. The data are available in Haver's SURVEYS database.| FRB Philadelphia Survey of Professional Forecasters (AR) | 2Q '09 | 3Q '09 | 4Q '09 | 1Q '10 | 2Q '10 |

|---|---|---|---|---|---|

| Real GDP | -1.0% | 2.4% | 2.2% | 2.5% | 2.8% |

| PCE | -1.2 | 1.7 | 1.1 | 1.7 | 2.0 |

| Non-Residential Investment | -8.9 | -7.3 | -6.3 | 2.1 | 3.8 |

| Residential Investment | -29.3 | -7.3 | 1.8 | 5.6 | 13.4 |

| Federal Government | 10.9 | 6.2 | 4.1 | 1.5 | 2.1 |

| Change in Business Inventories | $-141.1B | $-89.9B | $-32.7B | $-1.7B | $9.5B |

| Net Exports | -339.3 | -340.0 | -342.1 | -353.6 | -366.0 |

| Unemployment Rate (%) | 9.3 | 9.6 | 9.9 | 9.9 | 9.8 |

| Consumer Price Index (Y/Y, %) | 2.4 | 1.7 | 1.1 | 1.5 | 1.5 |

by Robert Brusca September 21, 2009

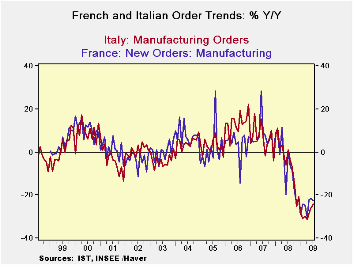

French orders were up by a solid 2% in July as foreign orders

surged by 14%. In Italy orders jumped by 3.2% on foreign order strength

of 15.6%. Both Italy and France as seeing strong orders in the new

quarter (Q3, one month in) led by huge gains in orders from abroad.

Both Italy and France show recovery patterns of order growth

but order levels that remain just a bit less than 25% below year-ago

levels.

Europe- Europe continues to show economic recovery. But with

the G-20 set to meet in the re-made but old US industrial city of

Pittsburgh, the OECD, the IMF and a German think-tank have taken this

opportunity to highlight the risks to the future of this recovery. The

OECD is very concerned about the health of banks and that there could

be some backsliding and troubles with capitalization. The IMF is

concerned that German employment could rise sharply over the next year,

pushing unemployment to over 10.5% and creating weak growth under 0.5%

in 2010. This would clearly become a problem for growth in the rest of

the e-Zone. Not to be outdone by this sort of sour outlook, the German

think-tank IWH Institute warns of a credit crunch highlighting the

potential for a double dip as government stimulus programs come off the

books.

Pessimism shuns trends: Despite some very strong current

indicators that spread across the major EMU economies there remains in

Europe, much like in the US, a core of pessimism about the risks.

Unlike after other recessions apparently this recovery cannot be

trusted to bottom and begin to rise and for that upswing to be

self-sustaining. The abnormal degree of and scope of early government

help that will eventually be rescinded is one of the common culprits in

both US and European pessimism. If that is so what ever do it in the

first place?

Professional pessimists: While we expect the main

international regulators and oversight agencies to be less than

cheerleaders and to be wary of risks, the extent to which private

sector naysayers have piggy-backed on that tact is surprising. For now

we are left with the reality of an upswing and one that is looking

quite nice and consistent across EMU nations. Meanwhile, the outlook

sours as we speak. While the future may still hold risks, one must

wonder if they are as great as is being said or if lowering

expectations has been taken to a new extreme by politicians who in the

end are chastened by their own role in this crisis by seeing it develop

and watching powerlessly, aware that it is a disaster that occurred on

their watch.

| Italy Orders | ||||||

|---|---|---|---|---|---|---|

| Saar exept m/m | Jul-09 | Jun-09 | May-09 | 3-mo6-mo12-mo | ||

| Total | 3.2% | 2.6% | 0.8% | 29.5% | -1.9% | -24.2% |

| Foreign | 15.6% | 2.6% | 0.9% | 105.4% | 17.6% | -19.1% |

| Domestic | -2.9% | 2.5% | 0.7% | 0.9% | -11.3% | -26.9% |

| Memo | ||||||

| Sales | 0.7% | -1.6% | -1.0% | -7.4% | -11.0% | -22.1% |

| French Orders | ||||||

| Saar exept m/m | Jul-09 | Jun-09 | May-09 | 3-mo6-mo12-mo | ||

| Total | 2.0% | 1.2% | 0.0% | 13.7% | 5.6% | -22.6% |

| Foreign | 14.0% | -3.0% | 7.0% | 96.1% | 19.1% | -16.7% |

| IP xConstruct | 0.6% | 0.2% | 3.0% | 16.3% | 2.8% | -13.8% |

Recent Data For The Russian Economy

by Louise Curley September 21, 2009

Preliminary data suggest that the Russian Gross Domestic

Product, fell 0.5% in the second quarter, a marked improvement over the

9.0% decline in the first quarter. (These figures are based on the

series that have been seasonally adjusted by Haver Analytics.) August

data on production, construction, and retail sales have been

disappointing. Production and construction declined in contrast to

increases in July and retail sales showed a smaller increase in August

than in July. The unemployment rate, however, was 8.6% in August 2

basis points below July.

Preliminary data suggest that the Russian Gross Domestic

Product, fell 0.5% in the second quarter, a marked improvement over the

9.0% decline in the first quarter. (These figures are based on the

series that have been seasonally adjusted by Haver Analytics.) August

data on production, construction, and retail sales have been

disappointing. Production and construction declined in contrast to

increases in July and retail sales showed a smaller increase in August

than in July. The unemployment rate, however, was 8.6% in August 2

basis points below July.

In spite of the July hiccup particularly in industrial

production, the prospects for increased activity in Russia have

brightened. Oil prices are up, the Reserve Bank has steadily lowered

the refinancing rate from 13% in March to 10.5% in September. Inflation, though still high, was 11.6% in August, down from 13.15% in

April. Recent data for these aspects of the Russian economy are shown

in the table below.

Inflation, though still high, was 11.6% in August, down from 13.15% in

April. Recent data for these aspects of the Russian economy are shown

in the table below.

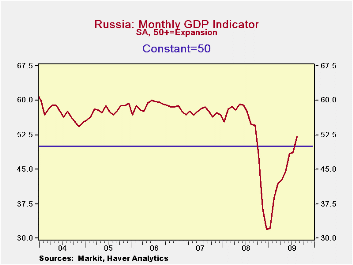

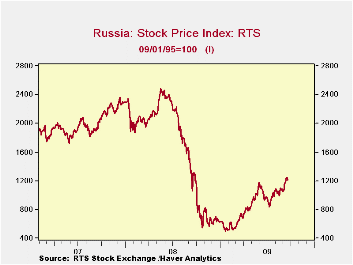

The Purchasing Mangers Survey published by Markit Economics in London reported earlier this month that the GDP indicator for Russia reached the expansion stage in August (above 50) for the first time since September, 2008 as shown in the first chart. Finally, the Stock Market has increased 44% from the recent low point reached on July10 and 1208 today is 139% above the low reached on February 2, 2009. The decline and rise in the stock market is shown in the second chart.

| RUSSIA | Sep 09 | Aug 09 | Jul 09 | Jun 09 | May 09 | Apr 09 | Mar 09 |

|---|---|---|---|---|---|---|---|

| Industrial Production (M/M % Chg) | -- | -3.0 | 4.7 | 4.5 | -2.1 | -8.1 | -- |

| Retail Sales (M/M % Chg) | -- | 1.68 | 2.36 | 0.88 | 1.70 | 0.71 | -- |

| Value of Construction Work Performed (M/M % Chg) | -- | -2.66 | 2.61 | 210.55 | 0.74 | 11.54 | -- |

| Unemployment Rate (%) | -- | 8.6 | 8.8 | 8.7 | 8.9 | 8.7 | -- |

| Inflation (%) | -- | 11.6 | 12.0 | 11.9 | 12.3 | 13.2 | -- |

| Refinancing Rate (%) | 10.50 | 10.75 | 11.00 | 11.50 | 12.00 | 12.50 | 13.00 |

| Oil Price Brent Crude (Ave of Daily Prices $ per barrel) | -- | 72.86 | 65.62 | 69.24 | 58.25 | 51.18 | -- |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief