Global| May 16 2007

Global| May 16 2007U.S. Industrial Production Surges Across the Board - Turning Point?

Summary

Industrial production is up strongly at the start of Q2 2007 and its lift is across the aboard. Vehicle output is strong. But output is strong apart from vehicles as well. Consumer product output is also strong and business equipment [...]

Industrial production is up strongly at the start of Q2 2007 and its lift is across the aboard. Vehicle output is strong. But output is strong apart from vehicles as well. Consumer product output is also strong and business equipment is strengthening sharply. All the signs of increased output are good except that domestic demand does not seem to be there to support it. Since inventories have been in a contracting/control mode (except in manufacturing where inventories have seemed to bloat further even as shipments have sagged). What does this surge in output really mean? Either the US is gaining trade competitiveness or the consumer will bail producers out by accelerating spending or what we see is evidence of more unneeded inventories being created.

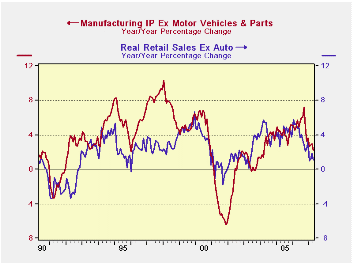

The big picture shows retail spending excluding autos correlates pretty well with industrial production excluding vehicles. Unfortunately both are showing declining trends even with this strong April output report factored in.

We can also look at consumer spending and output separate from capital goods. When we go behind the scenes to that level of detail, we see some evidence of a correlation between consumer spending and the output of consumer goods. But we still see the consumer spending is declining year/year and so is the output of consumer goods despite this month’s output surge.

Turning to capital spending, capital spending by itself is still slowing (y/y) even with this month’s strong rise in output. While durable goods orders (ex aircraft) are still very volatile, capital spending tracks its erratic trend with a lag. Both spending and orders are pointing to weaker performance ahead.Summing up…on balance, the NEWS on industrial production is reassuring by itself. After all producers do the things they do for a reason. But, for the moment we do not know what that is. Year/year consumer trends are slowing and capital spending plans are slowing as well. The rise in output in April only boosts the year/year industrial production growth rate to the point that it stays in a withering trend. Unless the U.S. is benefiting from a surge in trade (exports) that is not yet present in data, the rise in output this month is mostly a mystery.

| 3-Month | 6-Month | Year/Year | Y/Y Yr Ago | |

| Industrial Output | % Change | % Change | % Change | % Change |

| All Prod&Materials | 4.7% | 1.8% | 1.9% | 4.4% |

| All Products | 5.4% | 2.5% | 2.2% | 4.5% |

| Final Products | 6.4% | 3.7% | 3.0% | 4.7% |

| MFG-NAICS | 4.5% | 3.0% | 2.0% | 5.9% |

| MFG-Durables | 7.9% | 4.0% | 2.7% | 9.6% |

| MFG-Nondurables | 0.7% | 1.9% | 1.3% | 1.7% |

| Consumer Goods | 7.1% | 3.7% | 2.3% | 2.3% |

| Business Equipment | 9.0% | 5.1% | 5.7% | 12.7% |

| Materials | 4.3% | 0.9% | 1.4% | 4.4% |

| Capacity Use Level | 81.5 | 81.4 | 81.7 | 80.7 |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief