Global| Apr 16 2010

Global| Apr 16 2010U.S. Housing Starts Improve WithBetter Weather

by:Tom Moeller

|in:Economy in Brief

Summary

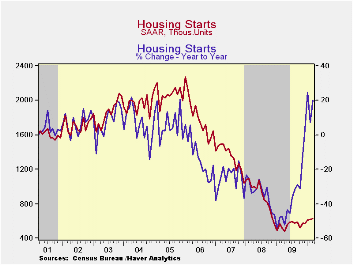

Improved weather last month helped housing starts rise 1.6% from February to 626,000 units (AR). Also good news from the housing sector was that snowstorms didn't depress activity by 5.9% from January as previously reported but [...]

Improved weather last month helped housing starts rise 1.6% from February to 626,000 units (AR). Also good news from the housing sector was that snowstorms didn't depress activity by 5.9% from January as previously reported but instead February starts rose modestly. Consensus expectations had been for 610,000 starts in March.

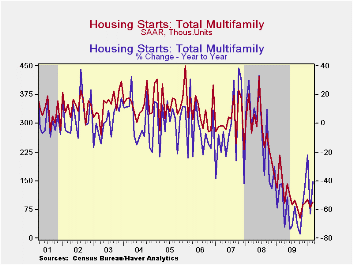

Starts of multi-family housing units accounted for the increase in March activity. Moreover, the upward revision to February to a lesser decline from January was behind much of the revision. Starts of apartments, condominiums & town houses recovered most of the February decline with an 18.8% increase but they still were down 40.6% from last March. Regardless, the q/q increase in starts was the first of this cycle.

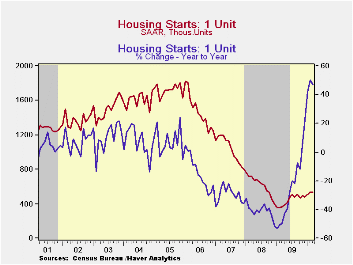

Despite their 0.9% m/m decline from February, starts of single-family homes also showed improvement. The decline was from an upwardly revised February level. It now shows an increase from January instead of the sharp decline reported earlier. Starts rose 48.7% from the recession low during February 2009. Single-family starts in the Northeast rose 5.6% during March and were more-than-double the January '09 low. In the Midwest, single-family starts fell by one-third from February (+19.0% y/y) and reversed all of the February gain. Though starts rose from their January '09 low ,they remained down three-quarters from the 2005 high. Starts in the South rose 9.9% (47.7% y/y) and in the West they rose 0.9% (82.8% y/y).

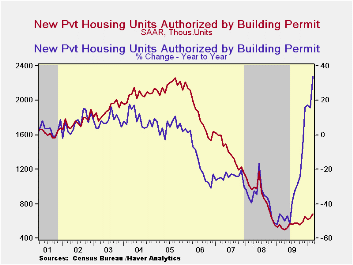

During March, building permits rose 7.5% following a 2.4% February increase. Permits to build a single-family home rose 5.6% and were up 58.8% from the low in January '09. Permits to build multi-family homes rose 15.4% and were 40.6% higher than their low last July.

The housing starts figures can be found in Haver's USECON database.

Coordination of Expectations in the Recent Crisis: Private Actions and Policy Responses from the Federal Reserve Bank of Kansas City is available here.

| Housing Starts (000s, SAAR) | March | February | January | March Y/Y | 2009 | 2008 | 2007 |

|---|---|---|---|---|---|---|---|

| Total | 626 | 616 | 609 | 20.2% | 553 | 900 | 1,342 |

| Single-Family | 531 | 536 | 507 | 47.1 | 440 | 616 | 1,036 |

| Multi-Family | 95 | 80 | 102 | -40.6 | 113 | 285 | 306 |

| Building Permits | 685 | 637 | 622 | 34.1 | 558 | 895 | 1,392 |

by Tom Moeller April 16, 2010

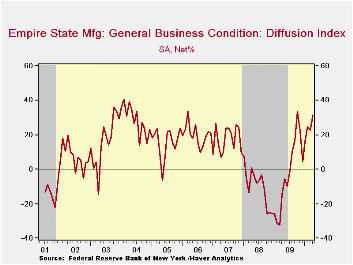

Forward momentum is building behind business conditions in the Northeast region of the country. The Federal Reserve Bank of New York reported that its April Empire State Factory Index of General Business Conditions rose to its highest level in six months. As a result it was near the highest since 2004. At 31.86, the diffusion index was up from its recession low of -32.29 in March 2009. The latest level suggests positive growth in factory sector activity and it beat Consensus expectations for a reading of 24.0.

The figure is a diffusion index. Since the series' inception in 2001, there has been a 74% correlation between its level and the three-month change in U.S. factory sector production. Like the Philadelphia Fed Index of General Business Conditions, the Empire State Business Conditions Index reflects answers to independent survey questions; it is not a weighted combination of the components. The series dates back only to 2001.

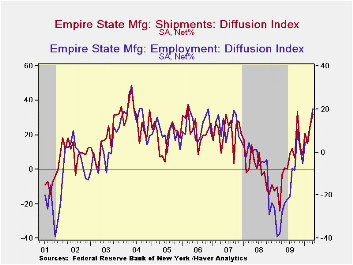

Amongst the separate survey questions, shipments and inventories rose strongly. Also strong was the employment index which rose to 20.25, near its highest since 2004 There has been an 87% correlation between the employment index and the three-month growth in factory sector employment as reported by the Labor Department.

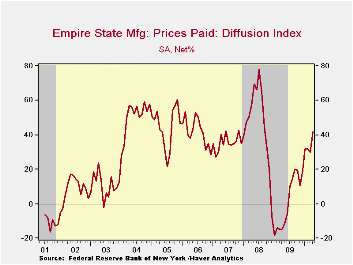

The prices paid index rose m/m to 41.77, its highest since September 2008. Since inception there has been a 76% correlation between the index of prices paid and the three-month change in the core intermediate materials PPI.

The Empire State index of expected business conditions in six months held steady m/m and was near the highest since early-2004. The capital expenditure and technology spending series both remained near the highest levels since the recession began.

The Empire State Manufacturing Survey is a monthly survey of manufacturers in New York State. Participants from across the state in a variety of industries respond to a questionnaire and report the change in indicators from the previous month. Each index is seasonally adjusted. Respondents also state the likely direction of these same indicators six months ahead. For more on the Empire State Manufacturing Survey, including methodologies and the latest report, click here. The Empire State data is available in Haver's SURVEYS database.

| Empire State Manufacturing Survey | April | March | February | April '09 | 2009 | 2008 | 2007 |

|---|---|---|---|---|---|---|---|

| General Business Conditions (diffusion index, %) | 31.86 | 22.86 | 24.91 | -14.59 | -2.76 | -9.97 | 17.22 |

| New Orders | 29.49 | 25.43 | 8.78 | -3.99 | -2.52 | -6.22 | 15.70 |

| Inventories | 11.39 | 4.94 | 0.00 | -35.96 | -22.89 | -7.87 | -3.95 |

| Employment | 20.25 | 12.35 | 5.56 | -28.09 | -17.28 | -5.36 | 11.28 |

| Prices Paid | 41.77 | 29.63 | 31.94 | -14.61 | 1.33 | 46.99 | 35.64 |

by Tom Moeller

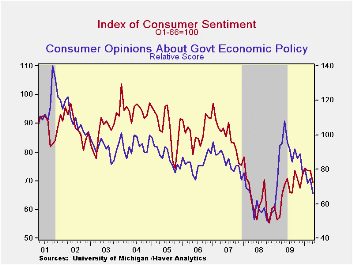

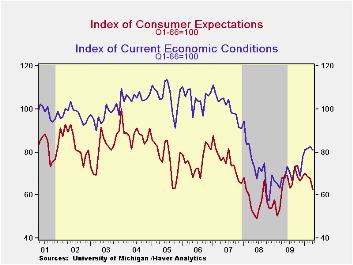

Despite the economy's recent improvement, it has yet to translate into a sustained rise in consumer sentiment. The University of Michigan reported that its mid-April index of consumer sentiment fell to 69.5 from 73.6 and was at its lowest level since November. The figure fell well short of Consensus expectations for a reading of 75.0. Nevertheless, sentiment remained up considerably from the low late in 2008. During the last ten years there has been a 90% correlation between the level of sentiment and the y/y change in real consumer spending.

Respondents' view of government policy, which may influence economic expectations, fell to its lowest level since January of last year. Just 11 percent of respondents thought that a good job was being done by government versus 45% who thought a poor job was being done, the highest since January '09.

The index of expected economic conditions fell 8.2% m/m to the lowest level since March of last year. The decline was led by a 9.8% decline in expectations for business conditions during the next five years to their lowest since July. Expectations for conditions during the next year fell 9.0% to their lowest since November. Perhaps more troubling was the 8.0% m/m decline in expectations for personal finances to the lowest level since February 2009.

The good news was that sentiment about current economic conditions fell a lesser 2.1% last month and remained near its cycle high. The assessment of current personal finances fell 2.6% and also remained near the cycle high and buying conditions for large household goods including furniture, refrigerators, stoves & televisions also fell just moderately.

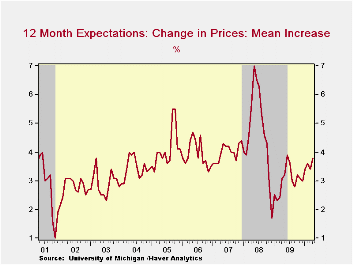

Expected price inflation during the next year rose further to 3.8% and was up from the December 2008 reading of 1.7%.

| University of Michigan | Mid-April | March | February | April y/y | 2009 | 2008 | 2007 |

|---|---|---|---|---|---|---|---|

| Consumer Sentiment | 69.5 | 73.6 | 73.6 | 6.8% | 66.3 | 63.8 | 85.6 |

| Current Conditions | 80.7 | 82.4 | 81.8 | 18.2 | 69.6 | 73.7 | 101.2 |

| Expectations | 62.3 | 67.9 | 68.4 | -1.3 | 64.1 | 57.3 | 75.6 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief