Global| Apr 17 2007

Global| Apr 17 2007U.S. Housing Starts Hit a Plateau

Summary

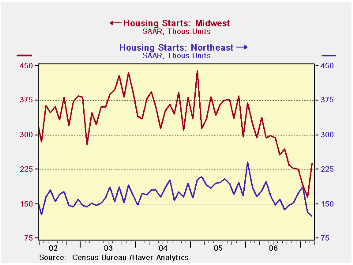

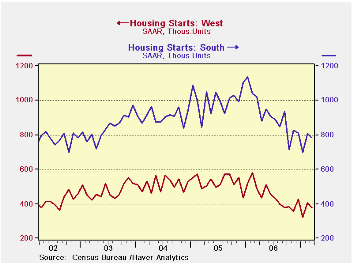

We plot the trends by region to show the common patterns. Each region shows a long down slope reflecting the lasting weakness in housing across the nation. But then most regions show some stability - or at least a hint of it. There is [...]

| · The table below shows the percent changes in starts and permits on different horizons without compounding. It shows that each measure except for the large projects (5 of more) is above its three-month average in March. This finding tends to reinforce the sense that there is some stability developing in the sector. To be sure, all measures are down over 3 months and 12 months. Two-to-four unit projects alone are flat or up compared to six months. Firmness on the three-month horizon is mostly in the Midwest where there is a 23% bounce (annualized) and in the South where a -12% annual rate trims the -33% annual rate drop over 6 months. |

|---|

| Seas Adj Annual Rate | Total | One Unit | 2- 4 Units | 5 or more | ||||

| In 000's of Units | Starts | Permits | Starts | Permits | Starts | Permits | Starts | Permits |

| This Month: | 1,518 | 1,544 | 1,218 | 1,114 | 38 | 72 | 262 | 358 |

| 3-month avg | 1,474 | 1,549 | 1,177 | 1,112 | 31 | 73 | 267 | 363 |

| 1-month % chg | 0.8% | 0.8% | 2.0% | 1.4% | 22.6% | 0.0% | -6.8% | -0.8% |

| 3-month % chg | -7.0% | -4.3% | -2.2% | -4.6% | -22.4% | -4.0% | -22.7% | -3.2% |

| 6-month % chg | -11.9% | -5.7% | -12.6% | -8.6% | 31.0% | 0.0% | -13.2% | 3.2% |

| yr/yr % chg | -23.0% | -25.9% | -24.6% | -28.4% | 5.6% | -13.3% | -18.4% | -19.9% |

We plot the trends by region to show the common patterns. Each region shows a long down slope reflecting the lasting weakness in housing across the nation. But then most regions show some stability - or at least a hint of it.

There is an outright bounce in the Midwest and somewhat slower erosion in the West. The South is still declining but is also slowing its pace of decline. The Northeast is unclear, having bounced in January, probably on the weather, then having started a new slide since then, but still not quite making a new low.

On balance, housing is still having troubles. The rise in starts this month came about only because of a DOWNWARD revision to the previous month. Had February not been revised lower the new level in March would have been a decline from February since the preliminary February reading was higher than the level of starts that now prevails in March. Even so the clearest evidence we have is that the pace of decline is slowing and that for the moment two of the three types of starts and the overall are above their 3-month average. Housing is still faltering but no longer seems to have the downward momentum. It’s sort of like a horror movie seen the second time around -- no longer any surprises and you’ve already seen the worst of it. But unlike the movie the second time around, you still don’t know where this one is going. Not for sure.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief