Global| Apr 24 2007

Global| Apr 24 2007U.S. Housing Drops Sharply, But it’s a Distortion - Look to the Moving Average

Summary

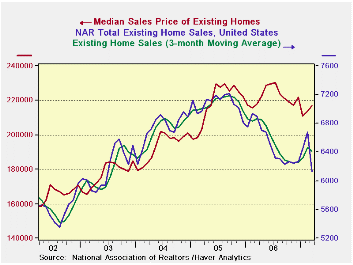

Existing home sales fell sharply in March but only after a similar sharp ramping up over the previous two months. The moving average of sales tells a better story falling by only a modest amount in the month. Meanwhile, home prices [...]

Existing home sales fell sharply in March but only after a similar sharp ramping up over the previous two months. The moving average of sales tells a better story falling by only a modest amount in the month. Meanwhile, home prices came back in the month (NSA) and are still lower year-over-year, but by a fractional 0.3%. Compared to its peak NSA price in July of 2006, median home prices are off by 5.7% and since housing prices make their peak in the summer, that is an exaggeration. Housing remains weak but is hardly falling apart despite his month’s number. Nationwide and in general the decline in home prices has not been large.

The table below shows sequential growth rates for sales by region. There is no clear pattern – but that is actually good news since this month’s drop was so severe and so distorting. Overall, the 3-month pace of sales decline is slightly lower than the year/year pace. But regions show all different results/patterns. House prices are weaker year/year for all regions except the South where a slight gain was posted in March.

By and large while housing has its pessimistic voices and optimistic voices, we are more inclined to see some silver lining in this month’s cloudy (rainy) report. The severity of the headline’s decline in sales is an exaggeration that blunts earlier good news. Price declines are NOT gathering pace. For the most part if the economy does stabilize, housing looks like it will be ok. And there is no trend in housing that makes it look as though it is going to drag economic growth lower. I think the days of those fears are gone. The stock of homes for sale is diminishing and that should reduce pressures too. While some say housing still has not shown the worst of it, we respectfully disagree.

| Mo/Mo% | Total | North-East | Mid-West | South | West |

| Mar.07 | -8.4% | -8.2% | -10.9% | -6.2% | -9.1% |

| Feb.07 | 3.7% | 15.1% | 2.6% | 1.2% | 0.0% |

| Jan.07 | 2.7% | -0.9% | 4.1% | 2.0% | 5.6% |

| Dec.06 | 0.3% | -0.9% | 2.8% | 0.8% | -2.3% |

| 3-Mo:ar | -9.6% | 18.7% | -19.2% | -12.9% | -16.0% |

| 6-mo:ar | -3.5% | 15.4% | -4.2% | -8.7% | -9.5% |

| 1-Year | -11.3% | -5.1% | -13.7% | -9.7% | -16.7% |

| Prices: | Median Prices | ||||

| One Mo: | 1.6% | 2.1% | 3.3% | 1.2% | -1.8% |

| One Year: | -0.3% | -0.7% | -0.2% | 0.4% | -2.9% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief