Global| Jan 29 2010

Global| Jan 29 2010U.S. GDP Rise Is The Quickest Since 2003

by:Tom Moeller

|in:Economy in Brief

Summary

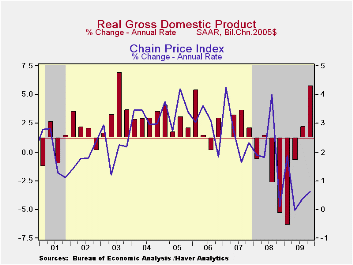

The current economic recovery picked up momentum last quarter. Constant dollar GDP rose 5.7% (AR), more-than double the 3Q growth rate and the quickest increase since 3Q 2003. Consensus expectations had been for a lesser 4.6% rise. [...]

The current economic recovery picked up momentum last quarter. Constant dollar GDP rose 5.7% (AR), more-than double the 3Q growth rate and the quickest increase since 3Q 2003. Consensus expectations had been for a lesser 4.6% rise.

The principle lift to last quarter's growth was inventories. The 3.4 percentage point contribution from inventory accumulation was necessitated by vigorous decumulation dating back to 2005. It had reduced desired inventory levels too far below demand even though sales were then declining.

Improvement in the foreign trade deficit also contributed one half of a percentage point to growth last quarter as exports remained strong. The 18.1% rate of increase (-1.7% y/y) followed a 17.8% 3Q gain as the lower value of the dollar continued to improve the competitiveness of U.S. products. Real imports, conversely, rose at a lesser 10.5% rate and remained down 7.7% versus last year.

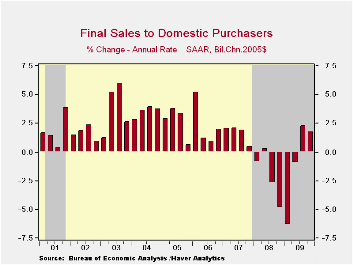

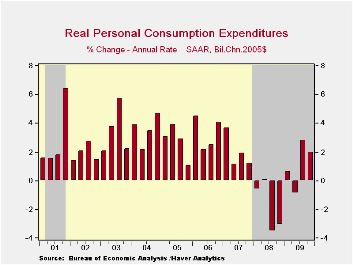

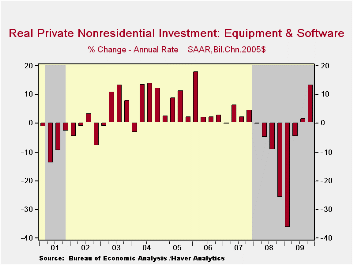

Growth in domestic final demand moderated to 1.7% after a 2.3% 3Q rise. Nevertheless, these were the first back-to-back quarterly increases since 2007. A 13.3% increase (-8.7% y/y) in business investment in equipment & software led the gain after its 1.5% 3Q rise. Investment in business construction, however, offset much of this increase with a 15.4% decline (-24.7% y/y). Residential investment also was strong and posted its second quarterly increase (-12.1% y/y). Personal consumption growth lagged with a 2.0% gain (1.1% y/y) that was dragged down by a sharp quarterly decline in spending on new autos with end of the "cash-for-clunkers" sales campaign. Spending on furniture & appliances rose for the second straight quarter (0.1% y/y) while spending on clothing surged q/q but remained down 0.7% y/y. Spending of services last quarter rose moderately (0.6% y/y). Finally, quarterly spending by governments fell slightly (+1.6% y/y), mostly due to a drop in defense spending though it remained up 3.1% y/y.

Price inflation remained moderate. The chained GDP price index rose at a 0.6% annual rate after a similarly small 3Q rise. Diminished price gains for all of last year pulled the annual increase down to 1.2% which was nearly its weakest increase since the early 1960s. The overall domestic final sales price index was basically flat for the year despite an accelerated 2.2% 4Q increase. The personal consumption chain price index rose 2.7% in 4Q but increased just 0.2% for the year.· The U.S. National Income & Product Account data are available in Haver's USECON and the USNA databases.

Focusing on Bank Interest Rate Risk Exposure is the title of this mornings speech be Fed Vice Chairman Donald L Kohn and it can be found here.

| Chained 2005$, % AR | 4Q '09 | 3Q '09 | 2Q '09 | 4Q Y/Y | 2009 | 2008 | 2007 |

|---|---|---|---|---|---|---|---|

| GDP | 5.7 | 2.2 | -0.7 | 0.1 | -2.4 | 0.4 | 2.1 |

| Inventory Effect | 3.4 | 0.7 | -1.4 | 0.0 | -0.7 | -0.4 | -0.4 |

| Final Sales | 2.2 | 1.5 | 0.7 | 0.1 | -1.7 | 0.8 | 2.5 |

| Foreign Trade Effect | 0.5 | -0.8 | 1.7 | 1.0 | 1.0 | -1.2 | 0.8 |

| Domestic Final Demand | 1.7 | 2.3 | -0.9 | -0.9 | -2.7 | -0.4 | 1.7 |

| Chained GDP Price Index | 0.6 | 0.4 | -0.0 | 0.7 | 1.2 | 2.1 | 2.9 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief