Global| Oct 22 2015

Global| Oct 22 2015U.S. FHFA Prices Slow

Summary

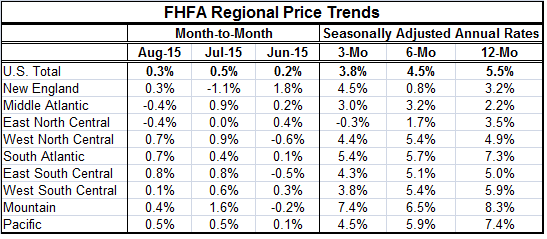

U.S. FHFA home prices slowed in August, rising by just 0.3% after a 0.5% July increase, data from the Federal Housing Finance Agency showed. Also year-over-year prices slowed, rising by 5.5% in August after a 5.8% July rise. The July [...]

U.S. FHFA home prices slowed in August, rising by just 0.3% after a 0.5% July increase, data from the Federal Housing Finance Agency showed. Also year-over-year prices slowed, rising by 5.5% in August after a 5.8% July rise. The July gain of 5.8% was a recent cycle peak and the largest year-over-year gain since May of this year. The year-over-year gain was last stronger in April 2014. House prices are no longer accelerating.

U.S. FHFA home prices slowed in August, rising by just 0.3% after a 0.5% July increase, data from the Federal Housing Finance Agency showed. Also year-over-year prices slowed, rising by 5.5% in August after a 5.8% July rise. The July gain of 5.8% was a recent cycle peak and the largest year-over-year gain since May of this year. The year-over-year gain was last stronger in April 2014. House prices are no longer accelerating.

Regional prices decelerated month-to-month in five of 12 regions. Three month changes show decelerations in seven of 12 regions compared to their six-month pace. Six-month percent changes show decelerations in six regions out of 12 regions. Clearly prices are no longer accelerating on any road front. The overall data confirm this and actually show price decelerations in train as the 12-month rise at a 5.5% pace gives way to a deceleration and a 4.5% pace over six months and slows further to a three-month pace of 3.8%.

In the chart, we compare FHFA prices to the median price series for single family homes complied by the NAR (National Association of Realtors). The series, while using very different methodologies, are very similar in terms of the major trends. The FHFA house price index is a weighted repeat sales index. It measures average price changes in repeat sales. The NAR index is simply the median price of all homes sold in a one-month period without any attempt to adjust for home size/quality. However, FHFA prices are - and have been- showing stronger price gains than is the NAR (existing home) series recently. Perhaps the NAR index is picking up more sales of lower quality or small-sized units.

Outlook for Prices

Housing activity is currently undergoing an upswing. Housing starts jumped this past month and existing home sales are rising briskly to a new local high for the three-month moving average of sales. The NAHB index (homebuilders' index) has risen strongly, too. And rising activity often pressures home prices higher. But house prices are nonetheless under downward pressure from other sources. Housing affordability has been slipping. Mortgage rates have moved up and there are concerns that they could rise further as the Federal Reserve is able to raise interest rates. Affordability is also pressured by the combination of flat wages and rising home prices. Rising home prices are actually a negative for the outlook for prices since they cause affordability to fall in this environment. In a high inflation environment, this might not be true, but in this environment with low inflation and constrained wages, rising home prices make homes less affordable and that eventually will stand in the way of further home price increases.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.