Global| Mar 06 2008

Global| Mar 06 2008U.S. Factory Inventory Gain Strong, Orders Reverse December Rise

by:Tom Moeller

|in:Economy in Brief

Summary

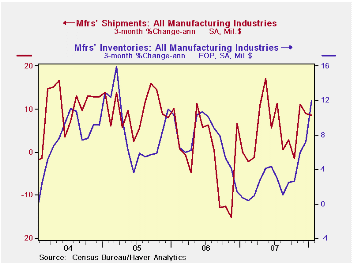

Factory inventories surged 1.3% in January and posted the strongest m/m increase since early 2005. It followed an upwardly revised 0.9% December increase. Together the gains lifted the three month annualized rate of increase to 12.0%, [...]

Factory inventories surged 1.3% in January and posted the strongest m/m increase since early 2005. It followed an upwardly revised 0.9% December increase. Together the gains lifted the three month annualized rate of increase to 12.0%, up sharply from last year's lows which were at or below 1.0% through the Summer.

Excluding the volatile transportation sector where the aircraft industry can have an outsized effect on the total figures, the story of accelerated inventory accumulation isn't much different. Inventories rose the same 1.3% in January, the December rise was revised up, and the three month rate of accumulation was 9.6%, up from slight decumulation early last year. Inventories in the civilian aircraft industry rose 3.7% during January and the three month rate of gain was 51.3%.

Total factory orders fell 2.5% during January, pulled lower by a 30.4% m/m decline in orders for civilian aircraft (+86.7% y/y). Less that decline and less the transportation sector altogether, orders fell a slight 0.4% after a 0.6% December gain. The three month rate of increase at 6.9% was down from the double digit rates of increase seen last year. January orders for durable goods fell 5.1%, about the same as the advance report of a 5.3% decline.

Factory shipments surged 1.1%, again influenced by a strong aircraft industry where shipments rose 11.7% (19.1% y/y). Excluding the transportation sector shipments rose 0.8% and the three month rate of growth of 9.2% was down by half from last year's peak rates of gain.

Overall unfilled orders rose 0.7% in January and the three month rate of increase was a hefty 18.6%. Shipments of civilian aircraft & parts still can't keep pace with orders, therefore backlogs rose 1.4% after a 4.0% surge in December (45.0% y/y). Excluding the transportation sector altogether unfilled orders rose a lesser 0.4% during January and the three month average growth rate was a still firm 9.2% (AR).

Macroeconomic Interdependence and the International Role of the Dollar from the Federal Reserve Bank of New York is available here .

| Factory Survey (NAICS, %) | January | December | Y/Y | 2007 | 2006 | 2005 |

|---|---|---|---|---|---|---|

| Inventories | 1.3 | 0.9 | 5.0 | 3.7 | 6.4 | 8.9 |

| Excluding Transportation | 1.3 | 0.5 | 4.0 | 2.5 | 7.1 | 8.0 |

| New Orders | -2.5 | 2.0 | 7.7 | 1.4 | 5.1 | 11.6 |

| Excluding Transportation | -0.4 | 0.6 | 8.0 | 1.2 | 5.4 | 11.5 |

| Shipments | 1.1 | -0.4 | 7.1 | 1.1 | 4.3 | 10.3 |

| Excluding Transportation | 0.8 | -0.2 | 8.1 | 1.3 | 5.0 | 11.4 |

| Unfilled Orders | 0.7 | 2.5 | 18.3 | 18.1 | 20.0 | 15.0 |

| Excluding Transportation | 0.4 | 1.3 | 8.6 | 9.1 | 14.1 | 8.4 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.