Global| Apr 30 2009

Global| Apr 30 2009U.S. Employment Cost Index Increase Slackens To New Low

by:Tom Moeller

|in:Economy in Brief

Summary

Weak job markets continue to hold down the increase in labor compensation. For private industry workers, the employment cost index increased by 0.2% last quarter which was less than half the 4Q gain. The gain fell well short of [...]

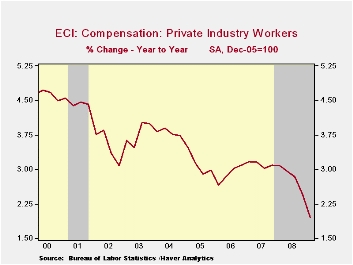

Weak job markets continue to hold down the increase in labor compensation. For private industry workers, the employment cost index increased by 0.2% last quarter which was less than half the 4Q gain. The gain fell well short of Consensus expectations for a 0.5% rise. The weakness in compensation is more apparent, however, in the 2.0% year-to-year increase which was the weakest in the series' history which dates back to 1981.

Compensation in manufacturing industries rose just 1.7% after a 2.3% gain last year while a severe slowdown in growth was evident in education & health services. The 2.9% increase compared to more than 3% growth during the prior five years. Health care compensation growth also slowed to 2.6%, its weakest on record.

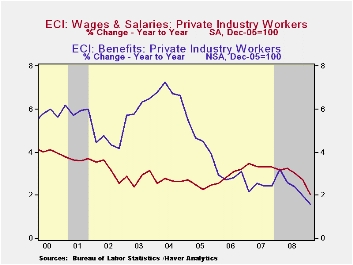

Wage and salary growth decelerated even further last quarter. The 0.2% gain pulled y/y growth down to just 2.0% which was its weakest on record. Wages account for roughly 70% of the compensation index. Wages in the services industries grew a not seasonally adjusted 0.5% and the y/y gain of 2.3% also was a record low. Wages in the goods producing industries inched up just 0.1% (2.1% y/y) and that y/y growth compares to a recent peak of 4.0% in 2000.

Slower growth in benefit costs continued to hold down overall compensation costs. The quarterly increase slowed to 0.2% after an upwardly revised gain of 0.4% during 4Q. The 1.5% year-to-year rise was a record low. In the goods producing sector benefits rose 1.3% y/y after a 2.2% increase during 2008 and in services they nudged up just 0.1% (1.7% y/y), a four quarter gain that was near the weakest on record.Health benefit costs rose 4.6% y/y which was near the slowest rate of growth since 1999.

The employment cost index figures are available in Haver's USECON database.

| ECI - Private Industry Workers (%) | 1Q '09 | 4Q '08 | 1Q Y/Y | 2008 | 2007 | 2006 |

|---|---|---|---|---|---|---|

| Compensation | 0.2 | 0.5 | 2.0 | 2.8 | 3.1 | 2.9 |

| Wages & Salaries | 0.2 | 0.5 | 2.0 | 3.0 | 3.4 | 2.9 |

| Benefit Costs | 0.2 | 0.4 | 1.5 | 2.6 | 2.4 | 2.9 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief