Global| Apr 25 2007

Global| Apr 25 2007U.S. Durable Goods Orders Rise by 3.4% in March

Summary

Durable goods orders are up by 3.4% after a rise of 2.4% in February. In most cases this sort of back-to-back gain would set a strong chain of growth in place. Instead, orders are still in a hole following a plunge of 8.8% in January. [...]

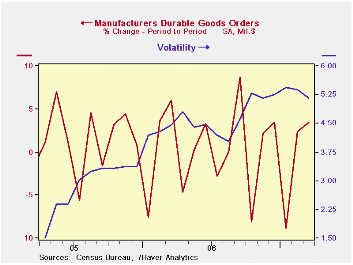

Durable goods orders are up by 3.4% after a rise of 2.4% in February. In most cases this sort of back-to-back gain would set a strong chain of growth in place. Instead, orders are still in a hole following a plunge of 8.8% in January. On balance the durable goods report shows some progress – better than expected progress -- after a very weak start in 2007. To be sure this month’s improvement does not wash out the weakness from earlier in the year. But it goes a long way to putting the MFG sector on firmer ground. Unfilled orders continue to look very strong in this report. One interesting feature of this report is the high degree of volatility it has showed. Volatility is up by 2 ½ times compared to early 2005 making it difficult to discern trend. Within the last seven months there have been THREE monthly changes in orders of 8% or more.

Three month trends are lower because in January orders were off by 8.8% and that is driving the last three month trend calculation. Next month that will fall out of the calculation and we have two quite firm months to add to whatever result April brings. On balance while we cannot say the current trends are good or solid, we can say that these lumpy data make us unsure of exactly which trend to trust. IF the data turn positive in April, we will be left with nice up trends instead of what we have now for three months.

Diffusion calculations that count the ups and downs of sector growth rates instead by overall weighted magnitudes of growth also show weakness. That’s over three months the weakness has not just been ‘severe’ but also broad-based.’ Three months shipments’ diffusion shows a value of 42 implying that over three months more sectors showed shipments decelerating compared to their six month behavior. Orders diffusion for three months was worse, too, at 28 showing orders increased in three months compared to six months in under 30% of the industries. But unfilled orders continue to mount up with 87% of the sectors showing that unfilled orders rose faster in three months than they did over six. Sales growth outpaced inventory growth in a small minority of sectors over three months. The weakness that the 8.8% drop in orders created seems to have permeated most measures and sectors for industry. Fortunately in the past two months MFG sectors show signs of breaking out of it.

The chart above plots the volatility of orders. It is quite clear that orders have had some voracious ups and downs. The past three months mimic a pattern from the previous three moths of showing a huge decline in orders followed by two quite robust monthly gains.

If we look at the major seven sectors (primary metals, fabricated metals, machinery, computers & electronics, electrical equipment, transportation equipment, and all other durables) we find that until six months ago the trends were declining and seemed to bottom. That is true of trends for both shipments and orders. But over the recent three months trends splayed in all directions, with most turning lower. Over the backward looking periods of three months, six months, and one year, order backlogs continue to show that they are rising and doing so fairly steadily. Work is piling up but increasingly it is not getting done. One singularly common feature is that these stepwise growth rates show across almost all sectors that inventory growth has been slowing. The sole exception is primary metals where prices have begun to flare once again. For computers & electronics, as well as for electrical equipment, stocks of inventories have actually been reduced.

It seems that inventory liquidation is in progress or at least that balance is being restored. After the sharp drop in orders, the desire to control stocks is understandable. We continue to see MFG as a sector that has undergone adjustment.

The MFG surveys for April (so far) continue to be uneven. It is not clear when they will light up MFG output again. For now it is a curiosity that the consumer has held up but that US business investment has been so lean. US investment and capital goods weakness is particularly surprising with the release of new German GDP data today and all the commentary there about how capital goods investment is driving German growth. Especially with the euro at these levels how could German firms benefit so much and US firms so little? What are US firms doing so badly that they are getting none of this business and investing nothing (or less) at home to boot?

| Durable Goods | 1Mo:m/m | 3Mo | 6Mo | 9Mo | 12Mo | Year Ago |

| Shipments | 0.8% | -8.1% | -0.9% | -3.2% | -0.6% | 7.6% |

| New Orders | 3.4% | -13.1% | -12.0% | -1.1% | -2.1% | 17.5% |

| Unfilled Orders | 1.8% | 13.6% | 18.6% | 20.9% | 19.8% | 20.9% |

| Inventories | 0.3% | 3.2% | 5.0% | 7.4% | 8.4% | 2.1% |

| I:S Ratio | 143.8% | 139.6% | 139.7% | 133.0% | 131.9% | 138.9% |

| Excl Transportation | 1Mo:m/m | 3Mo | 6Mo | 9Mo | 12Mo | Year Ago |

| Shipments | 0.3% | -3.7% | -2.5% | -3.0% | 0.1% | 8.4% |

| New Orders | 1.5% | -8.7% | -3.6% | -3.6% | -0.5% | 10.5% |

| Unfilled Orders | 0.9% | 10.1% | 11.5% | 12.2% | 13.5% | 12.8% |

| Inventories | 0.1% | 1.6% | 4.3% | 7.5% | 8.3% | 2.9% |

| I:S Ratio | 150.2% | 148.2% | 145.2% | 139.1% | 138.8% | 146.3% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief