Global| May 24 2007

Global| May 24 2007U.S. Durable Goods Orders: Rise and Shine, A New Dawn?

Summary

Durable goods orders now show signs of growth, shaking off some of the weaker performance from late last year and early 2007. The 0.6% headline marks the third straight month of orders increases. Order backlog growth continues to be [...]

Durable goods orders now show signs of growth, shaking off some of the weaker performance from late last year and early 2007. The 0.6% headline marks the third straight month of orders increases. Order backlog growth continues to be strong as well. Excluding aircraft, nondefense capital goods orders are up strongly for two straight months. Shipments and most cuts on capital goods shipments were strong in the month.

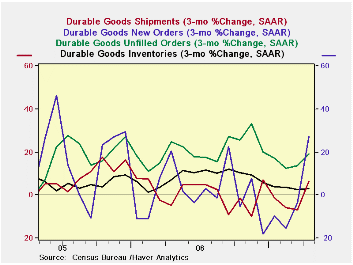

The chart for durable goods looks immediately better.

While three-month growth rates for durable goods can be very volatile, the graphs on the left documents a strong rise in new orders. A reversal (one month only) in shipments growth now shows advance instead of decline. And, more impressive, is the reduction in the rate of slowing for the declining pace of inventory growth. If firms are no longer seeking to cut inventory growth that could be very helpful to the sector assuming, of course, that the shipment pick up and order pick up are for real.

Diffusion to relieve confusion…

The statistics in the table below show that suddenly durable goods shipments and orders join unfilled orders in revealing that growth is broad-based across industries. Our (proprietary) diffusion readings are generally in the 70s or higher; 50 is neutral. These readings look for acceleration in sequential annualized growth rates (3-month Vs six-month, six-month Vs Yr/Yr, Yr/Yr Vs Yr ago, etc). We obtain these results from calculations of annualized growth rates performed across the main durables sectors. Diffusion calculations are helpful in this many-faceted report to distill common themes from an otherwise confusing array of components and subcomponent constructions. As of April, the various reading have begun to show signs of strength across most main sectors.

Sales have begun to exceed inventory growth in most industries over three and six months but are still lower in most for year/year growth (diffusion of 0.14 on this basis). Still, that weakness is an air-pocket of sorts since sales have begun to outpace inventories again just as they had done so one year ago. The report seems to show that the period of distress may have been put behind us even though the month’s reading was no clarion call to growth. It was however a step in the right direction that followed two previous stronger steps.

Orders in the once weak machinery category have broken higher. Primary metals orders again are very strong and transportation orders are strong again. Shipments data show some spottiness across industries but where there is strength it is very strong: primary metals, machinery and electrical equipment.

The report is the most upbeat from durables that we have seen for sometime.

| 3Mo | 6Mo | 9Mo | 12Mo | Year Ago | |

| Durables Diffusion | |||||

| Shipments | 71.4 | 85.7 | 71.4 | 85.7 | 100.0 |

| Orders | 100.0 | 71.4 | 42.9 | 57.1 | 100.0 |

| Unfilled Orders | 100.0 | 100.0 | 85.7 | 100.0 | 85.7 |

| Inventories | 71.4 | 85.7 | 100.0 | 100.0 | 100.0 |

| S>I Diffusion | 85.7 | 57.1 | 28.6 | 14.3 | 57.1 |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief