Global| Apr 17 2007

Global| Apr 17 2007U.S. CPI Gives Markets a Breath of Pretty Fresh Air

Summary

The 0.1% increase in the CPI in March (annual rate of 0.7%) is just what the CPI needed after back to back monthly increases of 0.23% but, after two such bad reports, this good one can only take the edge off bad trends; it cant by [...]

The 0.1% increase in the CPI in March (annual rate of 0.7%) is just what the CPI needed after back to back monthly increases of 0.23% but, after two such bad reports, this good one can only take the edge off bad trends; it can’t by itself make CPI trends good. For the month, inflation was not widespread; our monthly diffusion counter was at 42.9 for the headline and 42.9 for the core. Both signal that month-to-month inflation fell in more CPI categories than it rose. But both core and headline inflation now show an accelerating three-month pace compared to six months ago.

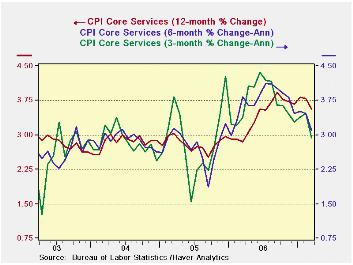

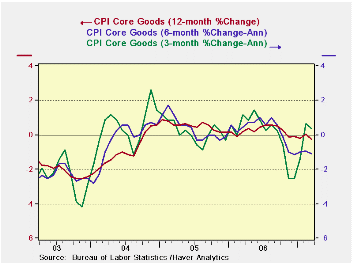

In the guts of this month’s report we find core goods prices were weak as in the PPI, falling at a 0.9% annual rate in the month. But services prices were moderate too, cutting their pace of increase to a pace of +1.4%. Still over three months core goods prices are rising by 0.4% and core services are at 2.9%. (the service sector is 71% of the core). So while the inflation game is still a tug of war between goods deflation and services inflation, both sectors say inflation pressures eased in the month. Services inflation has seen sequentially lower from 1-year to 6-months and from 6-months to 3-months.

While still high, core service sector inflation trends are cooling across horizons. However, look at the graph and realize how much this has to do with just this last month’s result. Inflation had started another minor uptrend. So while the chart looks benign, the result is still quite reversible.

Core goods prices are showing persisting declines in year/year and six-month rates of change. However, at the three-month horizon goods prices have reversed to show some inflation. So the anti-inflation trend is no longer as uniformly solid as it was.

| 5COLSPAN | Year-To-Date | 1- Mo | -- | |||||

| Quick Summary | Yr/Yr | 6-Mo AR | 3-Mo AR | -- | 2007 | 2006 | Diffusion | -- |

| CPI | 2.8% | 2.4% | 4.7% | -- | 4.7% | 3.7% | 42.9 | -- |

| Core CPI | 2.5% | 1.9% | 2.3% | -- | 2.3% | 2.6% | 42.9 | -- |

| Commodity Category | ||||||||

| Mo Annualized Rate |

Annualized Inflation Rate For Last | Mo/Mo Not Annualized |

||||||

| By Expenditure Category | Mar 2007 | % Weight | 3-Mo | -- | 6-Mo | -- | Year | Mar 2007 |

| All Items | 7.5% | 100.00 | 4.7% | -- | 2.4% | -- | 2.8% | 0.6% |

| By Economic Group | ||||||||

| All: Excl Food & Energy | 0.7% | 77.10 | 2.3% | -- | 1.9% | -- | 2.5% | 0.1% |

| (Median Increase) | 3.1% | 100.00 | 4.4% | -- | 2.8% | -- | 2.7% | 0.3% |

| Excl. Energy | 1.1% | 92.32 | 2.9% | -- | 2.2% | -- | 2.6% | 0.1% |

| Commodities Excl Food & Energy | -0.9% | 22.77 | 0.4% | (29% of core) | -1.1% | -- | -0.3% | -0.1% |

| Services Excl Energy | 1.4% | 54.33 | 2.9% | (71% of core) | 3.1% | -- | 3.6% | 0.1% |

| Core CPI less Tobacco | 0.7% | -- | 2.1% | -- | 1.8% | -- | 2.4% | 0.1% |

| Food & Energy | ||||||||

| Energy | 216.3% | 7.68 | 30.9% | -- | 1.7% | -- | 6.9% | 10.1% |

| Food | 3.4% | 15.22 | 7.3% | -- | 3.9% | -- | 3.3% | 0.3% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief