Global| May 14 2008

Global| May 14 2008U.S. Consumer Price Index Under Control in April

by:Tom Moeller

|in:Economy in Brief

Summary

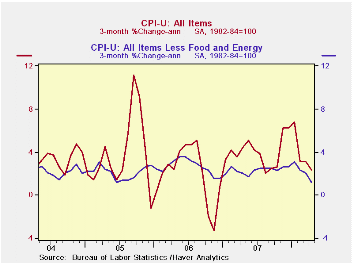

The consumer price index (CPI-U) rose 0.2% last month, down from the 0.3% March increase and less than the 0.3% rise that was generally expected. Year-to-year, prices rose 3.9% which was off the earlier highs of 4.4%. Less food & [...]

The consumer price index (CPI-U) rose 0.2% last month, down from the 0.3% March increase and less than the 0.3% rise that was generally expected. Year-to-year, prices rose 3.9% which was off the earlier highs of 4.4%.

Less food & energy, consumer prices also were under control last month and posted just a 0.1% uptick. That was half the Consensus forecast for a 0.2% gain. The year-to-year rise of 2.3% was equal to last year's full year gain and down from the 2.5% increase during 2006.

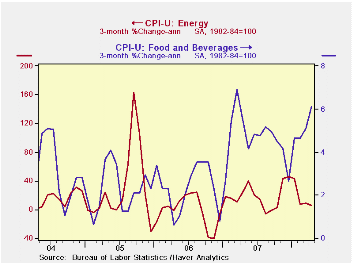

Food & beverage prices provided

lift to last month's gain in the CPI with a 0.9% increase. The

year-to-year increase of 5.0% was the strongest since 1990. Prices for

meats poultry & fish broke out of a several month slumber and

rose 0.9% (3.7% y/y). Showing real strength, however, were prices for

cereal & bakery products which increased another 1.4%. The y/y

rise in these prices of 8.9% was the strongest since 1989. Dairy

product prices also were quite firm and rose 0.7%. They surged 11.8%

year-to-year.

Energy prices were under control last

month and fell slightly. The weakness was due to a surprising 2.0%

(+20.7% y/y) decline in seasonally adjusted gasoline prices. (Not

seasonally adjusted gas prices rose 5.6% m/m in April and they are up

another 6.1% so far in May.) Conversely, fuel oil prices last month

surged 3.6% (42.8% y/y) while natural gas & electricity prices

also were strong. They posted a 2.5% increase (6.7% y/y).

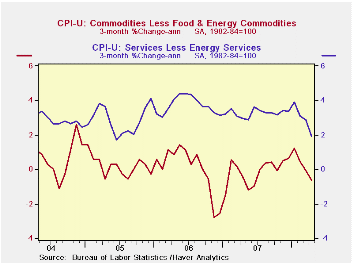

Core goods prices were unchanged following two consecutive months of 0.1% decline. Lower prices for new & used motor vehicles led the weakness with a 0.2% decline (-0.3% y/y). Prices for household furnishings & operations also fell by 0.1% (-0.1% y/y) after their brief 0.5% March increase. Apparel prices showed the only one month strength with a 0.5% (-0.6% y/y) increase that was the strongest rise since last November.

Core services prices also were under control and ticked up just 0.1%. Shelter prices, which constitute 33% of the total CPI, for the second month rose just 0.1% (2.6% y/y). Owners equivalent rent of primary residence, a measure not equivalent to other house price measures, rose 0.2% (2.6% y/y) and rents rose 0.3% (3.6% y/y). The downside to shelter costs was provided by lodging away from home where prices fell 1.9% (+1.1% y/y). Medical care services prices increased 0.3% (4.7% y/y) and tuition costs surged 0.6% (5.6% y/y). Prices for public transportation fell 0.4% (7.3% y/y) after the 2.5% March rise.

Are Inflation Targets Good Inflation Forecasts? from the Federal Reserve Bank of Chicago is available here.

Has the Behavior of Inflation and Long-Term Inflation Expectations Changed? from the Federal Reserve Bank of Kansas City can be found here.

| Consumer Price Index (%) | April | March | February | April Y/Y | 2007 | 2006 | 2005 |

|---|---|---|---|---|---|---|---|

| Total | 0.2 | 0.3 | 0.0 | 3.9 | 2.9 | 3.2 | 3.4 |

| Total less Food & Energy | 0.1 | 0.2 | 0.0 | 2.3 | 2.3 | 2.5 | 2.2 |

| Goods less Food & Energy | 0.0 | -0.1 | -0.1 | 0.1 | -0.4 | 0.2 | 0.5 |

| Services less Energy | 0.1 | 0.2 | 0.1 | 3.1 | 3.4 | 3.4 | 2.8 |

| Energy | -0.0 | 1.9 | -0.5 | 15.5 | 5.6 | 11.0 | 17.0 |

| Food & Beverages | 0.9 | 0.2 | 0.4 | 5.0 | 4.0 | 2.3 | 2.5 |

| Chained CPI: Total (NSA) | 0.5 | 0.8 | 0.3 | 3.5 | 2.5 | 2.9 | 2.9 |

| Total less Food & Energy | 0.1 | 0.5 | 0.3 | 1.9 | 2.0 | 2.2 | 1.9 |

by Tom Moeller May 14, 2008

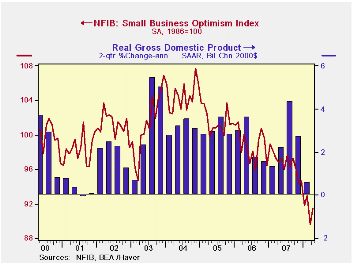

The National Federation of Independent Business (NFIB) reported that small business optimism during April gained back just more than half of its sharp drop in March. The 2.1% m/m increase to a reading of 91.5 followed a 3.6% March drop that had been to the lowest level since the short, "credit crunch" recession of 1980.

During the last ten years there has been a 70% correlation between the level of the NFIB index and the two quarter change in real GDP.

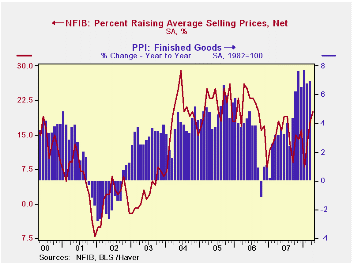

The percentage of firms actually raising

prices again rose m/m, to 20% which was the highest level since August,

2006. During the last ten years there has been a 64% correlation

between the y/y change in the producer price index and the level of the

NFIB price index. The percentage of firms planning

to raise prices also rose to 31%, its highest since late 2005.

Twelve percent fewer respondents expected the economy to improve and only five percent (up from 3% in March) of the respondents expected to raise employment. The latest was near the least since 2003. Twenty one percent of firms had one or more job openings. During the last ten years there has been a 71% correlation between the NFIB employment percentage and the y/y change in nonfarm payrolls.

Nine percent of firms indicated that credit was harder to get. That was near the highest level since 1993 and that was more than double the percentage during 2004.

Only six percent of respondents, up from five percent in March, thought that now was a good time to expand the business, the least since 1982, and expectations for earnings improved just slightly.

About 24 million businesses exist in the United States. Small business creates 80% of all new jobs in America.

The NFIB figures can be found in Haver's SURVEYS database.

Credit, Housing, Commodities, and the Economy is yesterday's speech by Janet L. Yellen, President and CEO, Federal Reserve Bank of San Francisco and it is available here.

| Nat'l Federation of Independent Business | April | March | Y/Y | 2007 | 2006 | 2005 |

|---|---|---|---|---|---|---|

| Small Business Optimism Index (1986=100) | 91.5 | 89.6 | -5.5% | 96.7 | 98.9 | 101.6 |

by Robert Brusca May 14, 2008

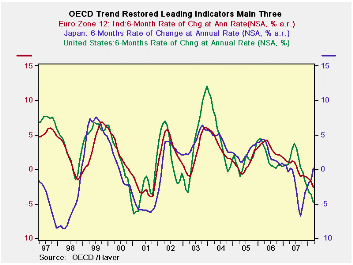

The OECD composite leading indicators show abroad slowing in

the OECD area. Only Japan is showing a rebound and that is because it

had been much weaker in earlier months. The six month horizons on the

bottom of the table shows the CLI trends in the six month periods that

the OECD likes to look at them. Weakness and accelerating weakness is

the predominate result on this basis of observation.

The chart shows that the depth of the slowdown in the various

indicators is comparable to their respective lows in the last

recession. Still the cycles are more out of phase at this time with

Japan dropping early and already signaling that it may be headed for

recovery- may be.

The Indicators are a stark reminder why the IMF has been

urging the ECB to hold off in being more aggressive in its inflation

fight. Already there is evidence of pending weakness that could help to

damp existing inflation pressures.

| OECD Trend-restored leading Indicators | ||||

|---|---|---|---|---|

| Growth progression-SAAR | ||||

| 3-Mos | 6-Mos | 12-Mos | Yr-Ago | |

| OECD | -1.9% | -1.7% | -1.3% | 1.3% |

| OECD 7 | -3.8% | -3.3% | -2.2% | 0.2% |

| OECD Europe | -3.9% | -2.3% | -1.8% | 1.5% |

| OECD Japan | 3.2% | 4.6% | -1.8% | -0.1% |

| OECD US | -6.1% | -5.7% | -2.4% | 0.1% |

| Six month readings at 6-Mo Intervals: | ||||

| Recent six | 6-Mos Ago | 12-Mos Ago | 18-Mos Ago | |

| OECD | -1.7% | -0.8% | 2.3% | 0.3% |

| OECD 7 | -3.3% | -1.2% | 1.1% | -0.6% |

| OECD Europe | -2.3% | -1.3% | 1.2% | 1.8% |

| OECD Japan | 4.6% | -7.7% | -0.3% | 0.0% |

| OECD US | -5.7% | 1.1% | 1.5% | -1.2% |

| Slowdowns indicated by BOLD RED | ||||

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief