Global| Sep 01 2005

Global| Sep 01 2005U.S. Construction Spending Losing Steam

by:Tom Moeller

|in:Economy in Brief

Summary

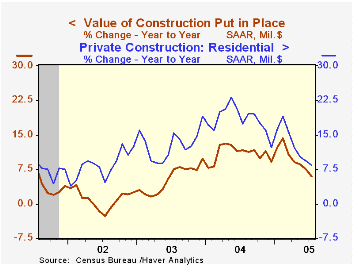

The value of construction put in place dipped slightly in July following a 0.6% decline in June, although figures for May were revised sharply higher. Consensus expectations had been for a 0.5% increase. Private residential building [...]

The value of construction put in place dipped slightly in July following a 0.6% decline in June, although figures for May were revised sharply higher. Consensus expectations had been for a 0.5% increase.

Private residential building activity rose slightly as did the value of residential building. New single family building rose 0.1% (9.0% y/y) following gains of 1.0% and 1.3% during the prior two months. The y/y growth in residential building is down by more than half from the peak growth rates of 2004.

Nonresidential building rose 0.2% following the downwardly revised 1.6% June decline but office construction (-1.0% y/y) fell hard for the third straight month.

Public construction spending fell for the second consecutive month as construction activity on highways & streets, nearly one third of the value of public construction spending, fell 2.4% (+7.0% y/y) for the fifth decline this year. While states' spending on highways & streets is up 8.0% y/y, federal spending is down by more than half versus last year.

These more detailed categories represent the Census Bureau’s reclassification of construction activity into end-use groups. Finer detail is available for many of the categories; for instance, commercial construction is shown for Automotive sales and parking facilities, drugstores, building supply stores, and both commercial warehouses and mini-storage facilities. Note that start dates vary for some seasonally adjusted line items in 2000 and 2002 and that constant-dollar data are no longer computed.

| Construction Put-in-place | July | June | Y/Y | 2004 | 2003 | 2002 |

|---|---|---|---|---|---|---|

| Total | -0.0% | -0.6% | 6.0% | 10.9% | 5.4% | 1.0% |

| Private | 0.2% | -0.6% | 6.6% | 13.6% | 6.3% | -0.4% |

| Residential | 0.2% | -0.2% | 8.5% | 18.2% | 12.9% | 8.5% |

| Nonresidential | 0.2% | -1.6% | 2.0% | 3.9% | -5.4% | -13.0% |

| Public | -0.8% | -0.6% | 3.9% | 2.5% | 2.7% | 5.7% |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief