Global| Apr 30 2007

Global| Apr 30 2007U.S. Construction Shows a Brighter Side

Summary

Real construction spending was up by 0.2% in March. Nominal construction spending was revised from a weak 0.3% in February to 1.5% gain. As a result construction trends are looking a lot better. Even the drain to GDP from residential [...]

Real construction spending was up by 0.2% in March. Nominal construction spending was revised from a weak 0.3% in February to 1.5% gain. As a result construction trends are looking a lot better. Even the drain to GDP from residential construction in 2007-Q1 is showing signs of diminishing.

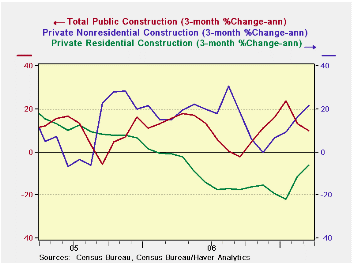

At 47.9% of total construction spending, residential spending is nearly two-thirds of private spending. And while we know that residential construction has been weak we also know that prices in the sector have been much less weak than activity has been. This relationship signals that the weakness has some sort of uneven character to it. While residential construction is still declining and fell at an annualized pace of 11.7% in March, that is a pace of decline that is below its year/year pace of decline. Moreover, building is picking up outside of the residential sector. Private nonresidential construction, although smaller, dominated the weakness in the residential sector to boost private construction to a 2.3% annualized gain in the month.

Three-month trends in spending are no longer as one-way negative. Since November, nonresidential private spending has been steadily accelerating. Its 3-month annualized rate of growth has now climbed above 20%. Meanwhile since January the 3-month growth rate of residential construction has risen from -22% to -6%. Public construction has come off during this period but is still growing at a pace of around 10%. The construction sector is getting ready to become a net CONTRIBUTOR to GDP growth despite the lingering weakness in the housing sector.

About GDP…. Residential building is only 4.4% of GDP. It can’t keep subtracting 1% from GDP growth as it did last quarter. It’s just too small. And it looks like that impact is already starting to diminish noticeably. If residential construction holds to its recent -6% growth rate it will decline by about $8 billion next quarter and that will shave just 0.3% from GDP... plus if the rest of construction remains on its trend, construction as a whole will add to GDP. The GDP story does not have the unhappy ending that some think. Not only is construction a turnaround category, but the inventory subtraction may be near the end of its retrenchment as well. But that is another report and discussion for another day.

| Percentage Change as Noted | ||||||

| 1-Mo | 1-Mo SAAR | 3-Mo | 6-Mo | Yr/Yr | Share | |

| Total | 0.2% | 2.9% | 4.8% | -0.5% | -2.0% | 100.0% |

| Private | 0.2% | 2.3% | 3.2% | -4.3% | -5.1% | 75.8% |

| Residential | -1.0% | -11.7% | -6.0% | -13.0% | -14.4% | 47.9% |

| Lodging | 13.2% | 344.7% | 134.5% | 68.5% | 58.5% | 2.3% |

| Office | 0.5% | 6.7% | 16.6% | 18.5% | 31.4% | 4.4% |

| Commercial | 1.3% | 16.8% | 16.7% | 5.5% | 10.6% | 6.9% |

| Transport | 1.4% | 18.8% | 73.4% | 74.4% | 1.3% | 0.8% |

| Communication | 2.1% | 28.1% | 65.7% | 26.5% | 20.5% | 1.6% |

| Power | 3.5% | 50.3% | -15.9% | -4.6% | 4.9% | 2.8% |

| MFG | 1.9% | 25.2% | 44.6% | 15.9% | 17.4% | 3.5% |

| Other | 1.1% | 14.7% | 1.0% | 6.3% | 9.5% | 5.8% |

| Public | 0.4% | 4.9% | 10.0% | 12.9% | 9.0% | 24.2% |

| Highway | 0.9% | 11.2% | 48.7% | 14.2% | 10.5% | 6.8% |

| Sewer | -5.8% | -51.2% | -25.1% | -6.9% | 0.8% | 1.6% |

| Water | -3.4% | -33.8% | 2.0% | 2.0% | -0.1% | 1.1% |

| Other | 1.2% | 15.2% | 1.3% | 15.7% | 10.1% | 14.8% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief