Global| Feb 12 2009

Global| Feb 12 2009U.S. Business Inventory Cutbacks Gained Steam

by:Tom Moeller

|in:Economy in Brief

Summary

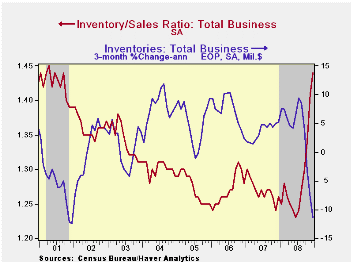

Total business inventories fell 1.3% during December after a downwardly revised November decline. The latest drop was the fourth in as many months and the rise of 0.9% year-to-year was the weakest since early-2004. The recent cutback [...]

Total business inventories fell 1.3% during December after a

downwardly revised November decline. The latest drop was the

fourth in as many months and the rise of 0.9% year-to-year was the

weakest since early-2004. The recent cutback in inventory accumulation

reflects the 11.8% y/y drop in business sales. During the

last three months inventories have been cut at an 11.4% rate as sales

have fallen at a 40.9% annual rate. The mismatch

between inventory and sales growth caused the December inventory/sales

ratio to surge further to 1.44, its highest level since the recession

of 2001. What's more is that the increase in the ratio during

the last year is the swiftest since 1982. The rise ended a twenty-eight

year downtrend.

Total business inventories fell 1.3% during December after a

downwardly revised November decline. The latest drop was the

fourth in as many months and the rise of 0.9% year-to-year was the

weakest since early-2004. The recent cutback in inventory accumulation

reflects the 11.8% y/y drop in business sales. During the

last three months inventories have been cut at an 11.4% rate as sales

have fallen at a 40.9% annual rate. The mismatch

between inventory and sales growth caused the December inventory/sales

ratio to surge further to 1.44, its highest level since the recession

of 2001. What's more is that the increase in the ratio during

the last year is the swiftest since 1982. The rise ended a twenty-eight

year downtrend.

Retailers cut inventories 1.0% in December and at an

11.7% rate during the last three months, the swiftest since

2001. Motor vehicle inventories continued to lead the

decumulation and fell at a 15.8% rate during the last three months.

Nevertheless, the inventory-to-sales ratio for automobiles remained

near its historic high at 2.59. So unless sales recover soon, expect

further production cuts to reduce the ratio.

Motor vehicle inventories continued to lead the

decumulation and fell at a 15.8% rate during the last three months.

Nevertheless, the inventory-to-sales ratio for automobiles remained

near its historic high at 2.59. So unless sales recover soon, expect

further production cuts to reduce the ratio.

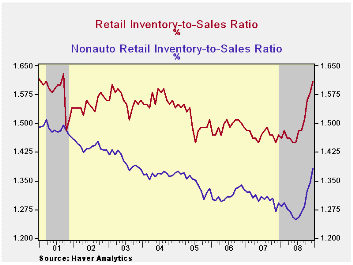

Outside of autos, retailers continued with their reduction of unsold goods. Furniture, home furnishings & electronics inventories fell 1.2% in December and they are off 5.5% during the past year. Apparel retailers cut aggressively as well. The 0.6% December decline matched the November inventory cutback and they're off 2.5% year-to-year. General merchandise inventories fell 1.1% (-2.7% y/y) during December. Overall, the inventory-to-sales ratio in the nonauto retail sector rose during December to its highest level since 2003.

| Business Inventories (%) | December | November | October | Y/Y | 2008 | 2007 | 2006 |

|---|---|---|---|---|---|---|---|

| Total | -1.3 | -1.1 | -0.6 | 0.9 | 0.9 | 4.1 | 6.5 |

| Retail | -1.0 | -1.8 | -0.2 | -2.8 | -2.8 | 2.9 | 3.5 |

| Retail excl. Auto | -1.0 | -1.5 | -0.1 | -1.5 | -1.5 | 2.9 | 4.9 |

| Wholesale | -1.4 | -0.9 | -1.2 | 3.4 | 3.4 | 5.9 | 8.3 |

| Manufacturing | -1.4 | -0.5 | -0.6 | 2.6 | 2.6 | 3.7 | 8.2 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief