Global| Jun 02 2009

Global| Jun 02 2009U-Rates On The Rise

Summary

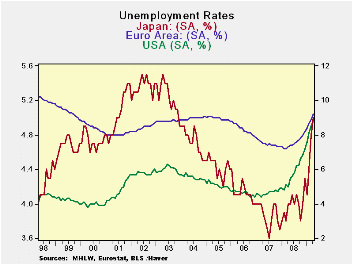

Unemployment rates are on the rise around the world. In EMU the new rate jumped up to 9.2%; the highest rate for the Area in 9-1/2 years (Sept 1999). There have been 3.1million jobs losses since the recession began. The US has seen a [...]

Unemployment rates are on the rise around the world. In EMU

the new rate jumped up to 9.2%; the highest rate for the Area in 9-1/2

years (Sept 1999). There have been 3.1million jobs losses since the

recession began. The US has seen a sharp rise in its rate of

unemployment over the past year, a gain of 3.9%. This surpasses the

1.9% point rise in EMU and the 1% point rise in Japan. However, the

rise in Spain as been of a whopping 8.1 percentage points, bringing in

its overall rate to 18.1%. And that spells e-Zone trouble.

Since the start of the US recession in December of 2007 the

German rate of unemployment has dropped – dropped - by 0.2% points. The

French rate has risen by 0.2% points. Spain’s U-rate is up by 9.2%

points. The US unemployment rate is higher by 4% points. In Japan the

U-rate is up by 1.3% points.

Spain’s rate has jumped as the property market has collapsed.

The rise there appears to have a very large structural element. In the

US the rise seems to be mostly cyclical but it is a substantial rise: a

gain of four percentage points compared to a level of 4.9% in December

of 2007.

Europe seems to have forestalled much of the rise in the rate

of unemployment – Spain excepted, of course. That leads to the

conclusion that despite a substantial social safety net in Europe, the

rise in unemployment is still in progress and will hit Europe later.

Moreover, Europe has different sorts of stresses as the social safety

net is uneven and spreads stress unevenly, across the Area. EMU is only

a common currency area with some economic harmonization rules; fiscal

policy is left to local custom and practice with two overall metrics in

place to constrain aggregate usage. That lack of commonality is now a

problem for the Area.

For the moment the e-Area’s MFG PMI indices are rising on only

a slight lag with the index in the US. This is with a relatively small

hike in the rate of unemployment in Europe (much of that in Spain) and

a substantial jump in the US. If the unemployment problem in Europe

grows worse, the European recovery that now seems to be on the heels of

the US could suffer substantial erosion. There is also a possibility of

political tensions in Europe as the recessions hit the various EMU

nations unevenly.

| Unemployment rate and changes | ||||||

|---|---|---|---|---|---|---|

| Level | Simple Changes | |||||

| Apr-09 | Mar-09 | Feb-09 | 3-Mo | 6-Mo | 12-Mo | |

| EU-Urate | 8.6 | 8.4 | 8.1 | 0.7 | 1.3 | 1.8 |

| EMU-Urate | 9.2 | 8.9 | 8.7 | 0.8 | 1.4 | 1.9 |

| m/m% | % changes (ar) | |||||

| EU-U 000s | 2.7% | 3.2% | 3.5% | 9.7% | 19.0% | 28.8% |

| EMU-U 000s | 2.8% | 3.1% | 3.0% | 9.1% | 17.7% | 27.0% |

| U-Rates | Apr-09 | Mar-09 | Feb-09 | 3-Mo | 6-Mo | 12-Mo |

| Germany | 7.7 | 7.6 | 7.4 | 0.4 | 0.6 | 0.3 |

| France | 8.9 | 8.8 | 8.6 | 0.4 | 0.9 | 1.3 |

| Spain | 18.1 | 17.3 | 16.5 | 2.5 | 4.9 | 8.1 |

| USA | 8.9 | 8.5 | 8.1 | 1.3 | 2.3 | 3.9 |

| Japan | 5 | 4.8 | 4.4 | 0.9 | 1.2 | 1 |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.