Global| Apr 25 2019

Global| Apr 25 2019U.K. Shows Mixed Results for Distributive Trades Survey

Summary

The U.K. distributive trades retail survey is generally more upbeat than the wholesale survey in April. That is true for the current readings as well as for the forward-looking expectations. The difference in the assessment, [...]

The U.K. distributive trades retail survey is generally more upbeat than the wholesale survey in April. That is true for the current readings as well as for the forward-looking expectations. The difference in the assessment, especially the assessment of the future, is striking.

The U.K. distributive trades retail survey is generally more upbeat than the wholesale survey in April. That is true for the current readings as well as for the forward-looking expectations. The difference in the assessment, especially the assessment of the future, is striking.

Retailing

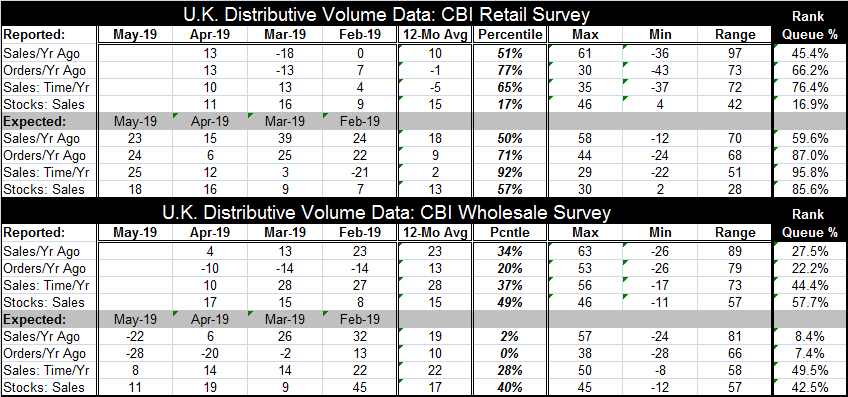

Sales in April over their one year ago value bounced strongly to log a 13 reading after being at -18 in March and zero in February. The April reading is above its 12-month average of 10. Still, it has only a 45.4 rank percentile standing. This metric has been weaker about 45% of the time despite its recent rebounding trend. Orders ‘over their one year ago level’ are in the same circumstance except they have a stronger 66.2 percentile standing. Sales ‘for this time of year’ are weaker in April than March but well above their 12-month average with a percentile standing of 76.4, the firmest reading in the retail group among current conditions. The stock-to-sales ratio is low with a 16.9 rank percentile standing.

The forward-looking expectations show an improvement for the outlook in May compared to April in each case with all expectations above their respective 12-month averages. Orders ‘compared to one year ago’ are strong with an 87th percentile standing. Sales ‘compared to a year ago’ have a more modest 59.6 percentile standing modestly above its median value. But sales ‘for this time of year’ have an impressive 95.8 rank percentile standing. While the current readings for retailing are firm, the outlook is generally much better and actually quite strong.

Wholesaling

Conditions in wholesaling are contrary to those in retailing. Wholesaling is generally weakening on the month and its percentile standings are much more modest for current readings than in retailing and are in several cases extremely weak for expectations. Current conditions in wholesaling April are weaker than March and February for both sales metrics; orders are improved on that timeline as is the stock-to-sales ratio. All four April metrics are below their respective 12-month averages except for the stock-to-sales ratio. Sales ‘for this time of year’ have the strongest rank percentile standing among activity readings as is also the case for retailing (the standing for the stock-to-sales ratio is higher). But sales compared to one year ago also have a weak 27.5 percentile standing; this reading is much weaker than its counterpart in retailing. Orders compared to year ago are weak with a 22.2 percentile standing; the stock-to-sales ratio has a 57.7 percentile standing.

The outlook metrics in wholesaling are all weaker than their respective 12-month averages, opposite the conditions we find for retailing. They are weakening month-to-month as well, not firming as in retailing. And the rank percentile standings in wholesaling speak of much weaker conditions expected ahead. Sales and orders compared to one year ago each have standings in the lower 10th percentile of their respective ranges. Sales for ‘this time of year’ are better off with a 49.5 percentile standing, but that is still just a median reading.

On balance

The distributive trends tell a mixed story. Retailing conditions are relatively firm at the present time while wholesaling is weaker. Retailing has been gaining momentum while wholesaling is losing momentum. Looking ahead, expectations for retailing range from firm to exceptionally strong compared to wholesaling where expectations are poor. It is not clear why this difference exists. It could be that retailing deals with domestic sales and that the economy has performed well so retailers continue to make good sales and are encouraged about the future. While one might expect that feel-good environment to matriculate from retailers to their suppliers, the wholesaler, wholesalers must acquire the goods they advance to the retailers, some of them might be importers or deal with importers and therefore be much more concerned about how things will evolve under Brexit which is still very much up in the air. If that is what is in play, here the difference in the outlook between retailers and wholesalers is entirely understandable.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief