Global| Apr 06 2020

Global| Apr 06 2020U.K. Sentiment Plunges

Summary

U.K. consumer sentiment recorded its biggest fall since records began in January 1974 as policy steps taken to curb the spread of coronavirus weighed on households. The GfK consumer sentiment gauge has plunged in March, but the [...]

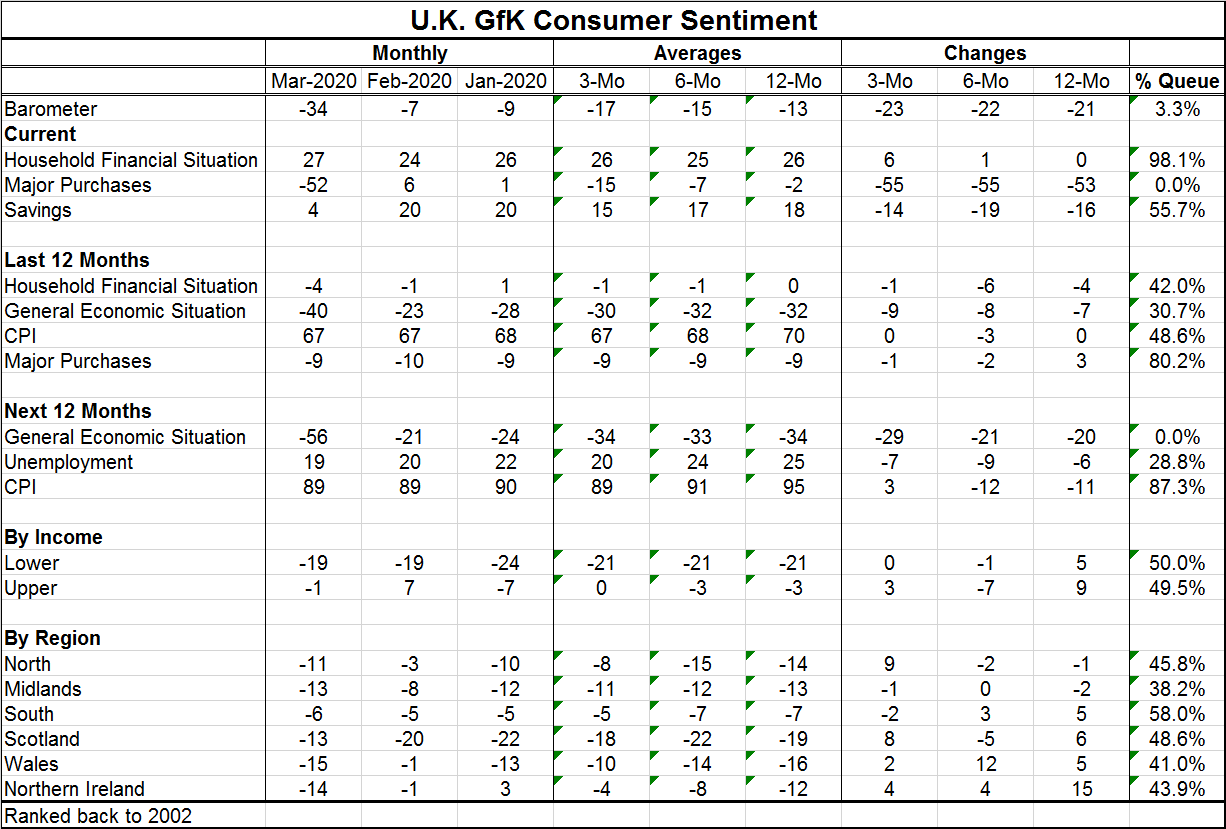

U.K. consumer sentiment recorded its biggest fall since records began in January 1974 as policy steps taken to curb the spread of coronavirus weighed on households. The GfK consumer sentiment gauge has plunged in March, but the various components of the survey display an almost surreal mix of 'best of times' vs. 'worst of times' readings. For example, the GfK headline barometer made its largest one-month drop on record. It sits at the bottom 3.3% of its historic queue of data back to 2002 in terms of the level of the barometer itself. Yet, the current household financial situation is assessed as having been better only about 2% of the time. And yet, the households assess the time to make 'a major purchase' as the worst ever since 2002. And so it goes throughout the survey. Assessments of the general economic situation in the current period already have dropped in March, but assessments of the next 12 months dropped even more to their lowest reading since at least 2002.

U.K. consumer sentiment recorded its biggest fall since records began in January 1974 as policy steps taken to curb the spread of coronavirus weighed on households. The GfK consumer sentiment gauge has plunged in March, but the various components of the survey display an almost surreal mix of 'best of times' vs. 'worst of times' readings. For example, the GfK headline barometer made its largest one-month drop on record. It sits at the bottom 3.3% of its historic queue of data back to 2002 in terms of the level of the barometer itself. Yet, the current household financial situation is assessed as having been better only about 2% of the time. And yet, the households assess the time to make 'a major purchase' as the worst ever since 2002. And so it goes throughout the survey. Assessments of the general economic situation in the current period already have dropped in March, but assessments of the next 12 months dropped even more to their lowest reading since at least 2002.

What is interesting is that even before the government policies and pledges of support were put into place, the U.K. work force has not been expecting a surge in unemployment. That's right; it has NOT been expecting a surge. Unemployment expectations for the next 12 months are only in their 28th percentile, roughly where they were (actually a bit lower) over the previous two months. Inflation expectations have not risen either.

On balance, there are some odd and bifurcated readings about the current and future expected states of the economy. These are March data and in late-March and early-April a lot happened so once again it will be interesting to see how these responses will change when one more month's-worth of data roll in. The situation remains dynamic, in flux, and every single bit of data you look at needs to have a timestamp to be compared with any other bit of data.

Germany in February...

Also released today are data on German factor orders: this release is for February. In February despite a drop in inflation-adjusted orders of 1.4%, a hot reading in January for Germany pushes the progression of orders higher with growth accelerating from 12-months to six-months to three-months. German foreign orders are stabilizing and generally show growth if not a clear acceleration, but German domestic orders are building a head of steam. Would anyone want to bet on that continuing? Probably not… March and April German data and trends are going to look very different that they look in February.

So what's next?

I am fielding calls about what happens next. There is a lot of confusion and, as always, a search for a paradigm. But there are no real paradigms for this. How do we transition out of this and where do we go? Some countries in Europe already are talking about or planning for the end-game. Germany and Austria are two such places. China has turned that corner, but somewhat disturbingly. Today China is reporting an increase in asymptomatic cases- that points up the importance of testing, testing, testing to maintain control and progress. With over 325 million people, the U.S. is going to have to be able to test more than a couple of million in order know what is going on. The same is true for everyone across Europe. The EMU region and the U.S. are nearly the same size (about 340 million for the EMU). The U.K. is home to about 66 million and except for the Chunnel, shipping and airports has a disconnection from continental Europe. And despite Brexit, there is still a lot of mingling when mitigation policies are not in effect. It seems no country is an island even if it is an island…

We have never seen anything like the conditions in which this next economic recovery will take place. The post war recovery was a rebirth but after a long war and with much of the means of production destroyed and with many of the youngest people dead. In this recuperative period, it is mostly old people and those with pre-exiting conditions who are dying an actually very few of them compared to the war period. Moreover, the means of production are still intact 100%. People will be ready to go back to work. However, there will be issues of displacements & bankruptcies and things will have changed. In our recovery wherever it is, in Europe, Asia or North America, the virus will still be lurking and some people will be cautious venturing out. It is not clear how fully group activities will come back on line, or how freely people will again to out to eat… Nor is it clear that companies will feel as secure with existing supply lines or if they will try to bring more production back home (eventually). There is a lot we do not know. And part of what happens will depend on how well government support programs work as well as on the vagaries of the ongoing spread of the virus itself.

So we are in a period of substantial uncertainty. The virus is still in play and either in full or slowing to allow some to entertain the end game phase. Policymakers want to play the end game carefully like in chess match so as not to lose the progress that has been achieved. Still, we do not know how the start over will progress. We don't know how well government programs will prove to have kept things together. We do not know if there will be a second wave of infections from this virus.

We simply do not know. And we do not know… what we do not know.

All this argues for a baseline view that seems a more moderate recovery. Perhaps it will be somewhat faster at first because there will be strong initial gains, up from some real depths as workers return from their mandated furloughs. But after the initial surge, how will growth settle in? How strong? How well will markets recover? A lot of this will depend on government policies, leadership and the foresight of corporate leaders. So far, most firms seem to be more or less enthusiastically pitching in. We are coming off a base of having had some real strength across the global economy. Even the U.K. with its Brexit transition in place and its future being negotiated has shown some substantially strong current readings. But the next month or so is an unknown. The question of what's next will continue to hang in the air.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.