Global| May 19 2016

Global| May 19 2016U.K. Retail Sales Snap Back

Summary

U.K. retail sales snapped back in April, rising by 0.9% after falling by 0.7% in March. However, over three months, sales are still falling at a 2.6% annual rate, a clear deceleration from their steady nominal path of 1.2% or so over [...]

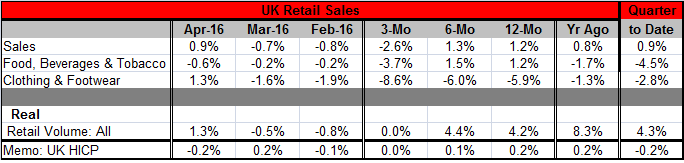

U.K. retail sales snapped back in April, rising by 0.9% after falling by 0.7% in March. However, over three months, sales are still falling at a 2.6% annual rate, a clear deceleration from their steady nominal path of 1.2% or so over six months and 12 months.

U.K. retail sales snapped back in April, rising by 0.9% after falling by 0.7% in March. However, over three months, sales are still falling at a 2.6% annual rate, a clear deceleration from their steady nominal path of 1.2% or so over six months and 12 months.

Despite that weakness, the sales volume figures show a good deal more stability. Volumes rose by 1.3% in April, sharply higher than the 0.5% March drop and more or less compensated for drops in March and February.

As a result of April strength, sales volumes are flat over three months but growing at a fast 4.2%-4.4% pace over six months and 12 months. Sales volumes have slowed from the hectic 8.3% pace of one year ago, however.

In the quarter-to-date, U.K. sales volumes are up at their well-worn 4.3% annualized rate which we see over the broader horizons. Compare this to the 0.9% rise being posted by nominal sales against declines at a 4.5% pace for food, beverages and tobacco and a 2.8% nominal pace drop for clothing and footwear.

U.K. sales trends in volume terms show a good deal of stability especially in terms of the chart of year-over-year growth rates.

The rebound in retail sales is somewhat reassuring as recent U.K. data have been on the soft side, raising concerns that Brexit fears might be affecting the economy. With the bounce back of sales in April, we see the Brexit has not brought the consumer to his knees despite what have been other weak indicators such as the BRC's like-for-like sales report. Even so, the sense of well-being in retailing stems substantially from a strong rebound in April which even in volume terms follows two consecutive months of sales declines. It is a good time not to get sucked in by any single month's numbers. The April rebound is reassuring, but it is not a definitive statement on the U.K. consumer or his mental health in the face of the challenges of Brexit uncertainty.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief