Global| Nov 20 2020

Global| Nov 20 2020U.K. Retail Sales Rebound Strongly; Deck the Halls! Or Dock the Enthusiasm?

Summary

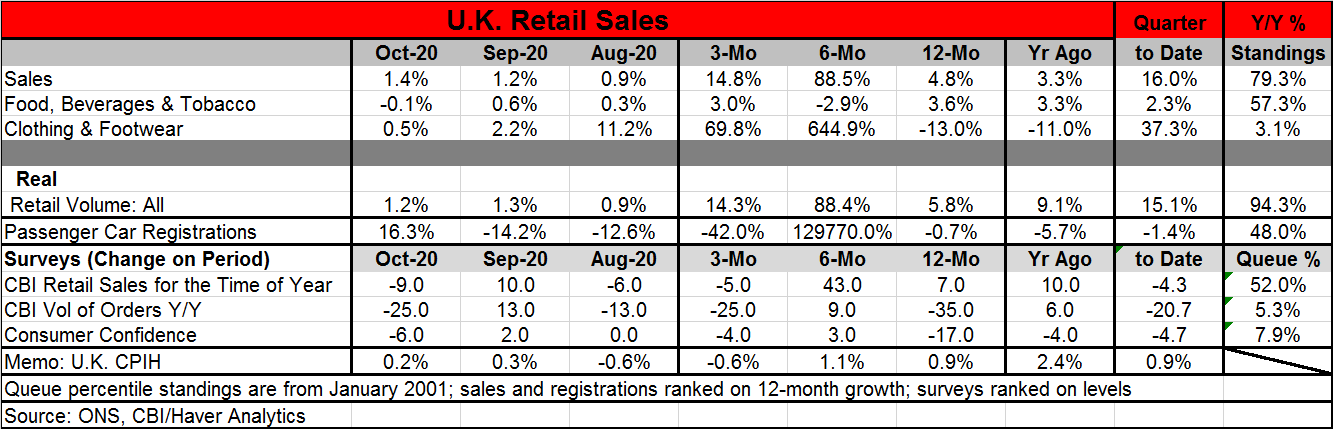

U.K. retail sales have rebounded strongly in October, rising by 1.4% after a 1.2% gain in September. Retail sales in the U.K. are higher on all three horizons: 12 months, six months and three months. Over the recent three months, [...]

U.K. retail sales have rebounded strongly in October, rising by 1.4% after a 1.2% gain in September. Retail sales in the U.K. are higher on all three horizons: 12 months, six months and three months. Over the recent three months, sales are expanding at a 14.8% annual rate, a nice head of steam underpinned by a solid monthly pattern.

U.K. retail sales have rebounded strongly in October, rising by 1.4% after a 1.2% gain in September. Retail sales in the U.K. are higher on all three horizons: 12 months, six months and three months. Over the recent three months, sales are expanding at a 14.8% annual rate, a nice head of steam underpinned by a solid monthly pattern.

The growth rates for retail sales has a 79.3 percentile standing among all growth rates from 2001 forward (a top 1% result). This is a quite-firm standing. The standing of actual retail sales is much stronger than for surveys of sales for 'the time of year' (52%), the year-on-year gain in the volume of retailer orders (5.3%) and even consumer confidence (an abysmal 7.9% standing on the level of the index). Understandably, there was surprise at the strength of sales in October and there is some skepticism that such strength can be sustained. However, expressed in real terms, the sales growth ranking is even high (94.3%) and the month sequence underpinning it is still authentically strong as well. The strength in sales may not be sustained, but it is no statistical fluke.

The U.K. remains in a difficult position after reporting bloated budget numbers. There is talk of the having to implement some selective government pay freezes. There are concerns elsewhere that tax hikes could be required and they could batter the economy. And in the background is the unrelenting drum beat of a Brexit negotiations on trade relations that are still not concluded. The U.K. continues to field unrelenting economic pressures from various sources. The recent CBI manufacturing survey was a disappointment as well. And while global measures like the just–released WTO world trade barometer has rebounded strongly in the third quarter, we are midway into the fourth quarter and we knew the Q3 was a rebound quarter what we do not know about is Q4 and beyond - especially with the virus rearing up again and doing so on a global scale. So be careful taking solace from cyclical reports like this that may actually be a step behind reality. 'The most recent economic report' still may not be fresh enough to rely on…

The GfK consumer confidence index for the U.K. plunged when the virus struck and has been slow to recover. There was a several month minor rebound, which now seems to have run out of steam, driving the reading back down near its recent cyclical lows. Confidence is poor largely for reasons related to the virus despite some recent encouraging news on vaccines. The two charts here show the disconnection between spending jumping and confidence lagging. Part of it may be retailers' attempt to jump start early the holiday shopping season, knowing that the last-minute shopping density will not be able to match up to what it has been in the past. If so, current strength may only be borrowing strength from the next couple of months. This will be something to watch as the calendar is well ahead of the 'usual holiday shopping season.' That season typically kicks off in mid-November in the U.K. and in late-November. In the U.S., it starts after the U.S. Thanksgiving Day holiday, when Santa Claus comes to town in a grandiose Thanksgiving Day parade…that will not be held in 2020 (that holiday is coming up next week, in fact!). However, stores everywhere have been offering pre-holiday sales to be sure that they do not miss out and to compete with internet sales.

As a result of this potentially changed seasonal pattern, the impact of the virus, and the uncertainty of Brexit, it is hard to know where the U.K. consumer stands. But recent budget news is a reminder that programs to help people through economic lockdowns are expensive and there are voices in the U.K. warning of the potential for tax hikes and pay freezes- nothing like that to send a chill up the spine of the consumer on a cold November day... Some skepticism about the sustainability and even meaning of the strength in U.K. retail sales seems very much warranted despite its clear authenticity.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief