Global| Jun 19 2020

Global| Jun 19 2020U.K. Retail Sales Rebound Sharply in May

Summary

The U.K. is being clobbered by the lockdown designed to stop the spread of the coronavirus. Sales fell by 6% in March and by 18.8% in April but have rebound smartly by 11.7% in May. The growth rates in real terms are similar in [...]

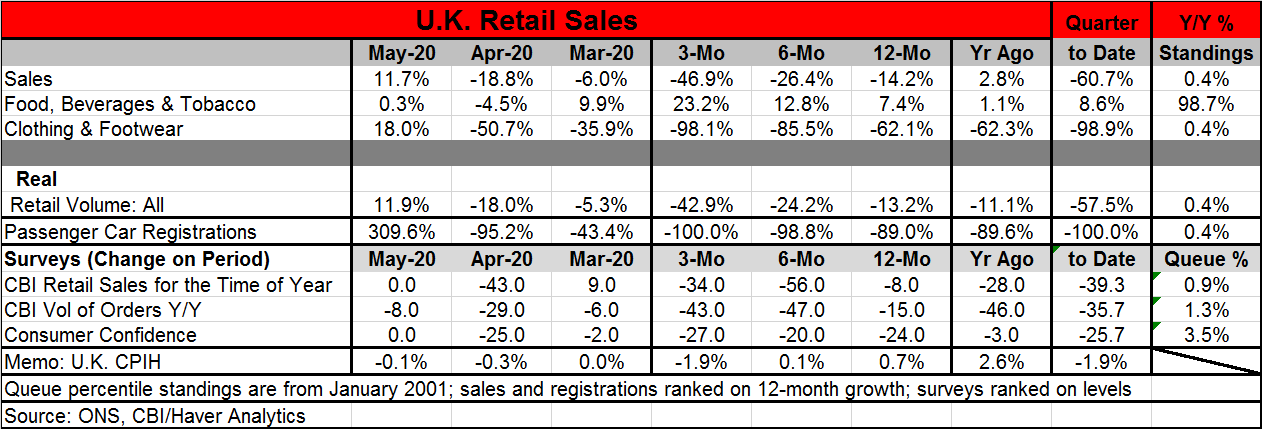

The U.K. is being clobbered by the lockdown designed to stop the spread of the coronavirus. Sales fell by 6% in March and by 18.8% in April but have rebound smartly by 11.7% in May. The growth rates in real terms are similar in pattern. The nearly 12% rebound after a nearly19% drop is an impressive rebound. But it still comes after a string of declines and it leaves retail sales down by 14.2% over 12 months. The chart plots the year-over-year growth rates; on that basis the sales rebound is not as impressive-looking. But sales did get back 60% of the drop in just one month.

The U.K. is being clobbered by the lockdown designed to stop the spread of the coronavirus. Sales fell by 6% in March and by 18.8% in April but have rebound smartly by 11.7% in May. The growth rates in real terms are similar in pattern. The nearly 12% rebound after a nearly19% drop is an impressive rebound. But it still comes after a string of declines and it leaves retail sales down by 14.2% over 12 months. The chart plots the year-over-year growth rates; on that basis the sales rebound is not as impressive-looking. But sales did get back 60% of the drop in just one month.

But the point is that growth is still weak; in fact, in the quarter-to-date (two months into Q2 compared to the sales level in Q1), sales are still falling at a 60.7% annual rate. This is because sales fell by 0.7% in January 6% in March, so that sales ended Q1 on a weakening note. Then Q2 began with an 18.8% sales drop in April so that the 11.9% boost in the middle of the quarter comes after a series that was deeply depressed. Of course, there will probably be another gain in sales in June, but the quarter is still going to be a disaster for retail sales and part of that is because of how weak sales were as the transition between quarters occurred.

In contrast, food, beverages and tobacco sales (hereafter 'food') ticked higher after falling in April. They were very strong in March. Since food stores remained open sales, there have been maintained or even improved since people had stayed at home and restaurants were either closed or forced into a take-out only business model. 'Food' sales in Q2 are stirring at an 8.6% annual rate.

There is real weakness in clothing and footwear. These are businesses that usually depend on in-store visits and hardcore shopping. Yes, I know some use the internet, but many people need to try things on especially slacks and shoes. So not surprisingly these sales screeched to a halt when there was a lockdown and they still did not make such a robust recovery in May gaining back only about 35% of the growth they shed in April after having had a horrific March as well. Clothing purchases are down at a 98% annual rate over three months and at about the same pace over 12 months.

Retail volumes are down at a 42.9% annual rate over three months and at a 13.2% annual rate over 12 months. Passenger car registrations a 'real variable' of sorts exploded with a 309.6% growth rate in May after plunging at a -95.2% pace in April and by -43.4% in March. Even so registrations are down at a 100% annual rate over three months and by 89% over 12 months.

The surveys of retail activity show their steepest declines in April some mixed and mostly negative numbers in March and numbers that are still falling or at a zero rating in May. On balance, the surveys show substantial declines over both three months and six months with all showing drops indicated over 12 months. But the queue standings tell the real story.

The queue standings for sales are applied to year-on-year growth rates. They are at 0.4% for nominal sales and the same for real sales as well as for clothing and footwear. The food category has a 98.7% standing. The lockdown was good for food and beverage stores. Passenger car registrations also have a 0.4% queue standing. As for the surveys, they are quite similar to the sales rankings. Retail sales for the time of year are at a 0.9 percentile standing and CBI order values are at a 1.3 percentile standing. Consumer confidence is at a 3.5 percentile standing.

We can conclude from all this that the various gauges on the U.K. retail scene agree. While there is life in May, it is only slightly more active than life on Mars- well, that is an exaggeration. May showed a sharp rebound, but that still pales in contrast to where sales have been and where they need to go to reflect normalcy again.

The U.K. has piled on a lot of debt to bolster its economy and the debt-to-GDP ratio now surpasses unity. The U.K. deficit is massive and monetary policy just became a bit more accommodative. So there is still a tough row to hoe to get back to normalcy…and then there will be all that debt to deal with. There are few exchange rate implications here since all countries have ramped up debt. But there will be different financial repercussions as we see how different countries go about handing their large debt stock once economic conditions normalize. Running up your credit card is much more fun than paying it down. But this incident of debt use was more like falling back on a credit line because you were too sick to work and used the credit line to survive. Now there will be having to and pay off the debt. And for many Brits, the future and its opportunities simply will not be the same. Programs to help those harmed by a lockdown can never fully compensate everyone. There are winners and losers and that is why governments should strive to do such things as infrequently as possible. The jury is still out on this one, on what happened, on why and about if the bail-out has been appropriate. But that discussion will lie ahead. Expect it to be painful and divisive.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief