Global| Dec 19 2019

Global| Dec 19 2019U.K. Retail Sales Post Surprise Drop

Summary

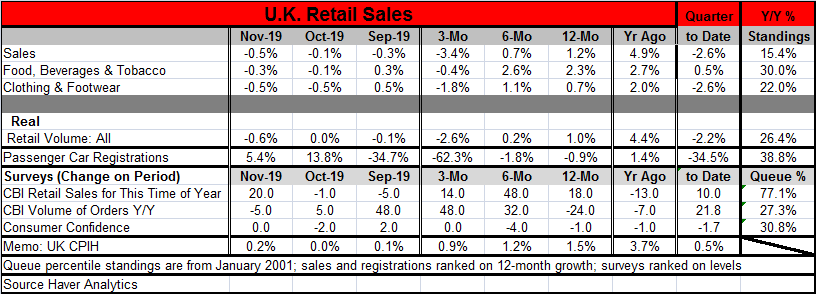

U.K. nominal retail sales are lower by 0.5% in November, marking their fourth straight decline month-to-month. With Brexit and a national election facing British citizens, they have been a bit slow on the uptake of Christmas spirit. [...]

U.K. nominal retail sales are lower by 0.5% in November, marking their fourth straight decline month-to-month. With Brexit and a national election facing British citizens, they have been a bit slow on the uptake of Christmas spirit. But now maybe they can put some of those things behind them and focus on spending…Or, maybe not.

U.K. nominal retail sales are lower by 0.5% in November, marking their fourth straight decline month-to-month. With Brexit and a national election facing British citizens, they have been a bit slow on the uptake of Christmas spirit. But now maybe they can put some of those things behind them and focus on spending…Or, maybe not.

Retail sales volume also decline in real terms in November. Sales volumes have not increased in four months and have fallen in three of the last four months.

Sequential sales volume show clear patterns as both nominal and real sales demonstrate sequentially weakening growth from 12-months to six-months and from six-months to three-months. Over three months, both real and nominal U.K. retail sales are falling.

In nominal terms, foods as well as clothing and footwear demonstrate weakening trends if not sequentially weakening trends. Although passenger car registrations are up in each of the last two months, they are sequentially slowing from 12-months to six-months to three-months. The slowing paradigm is getting a lot of support from various retail measures.

Retail sales in nominal terms have a 12-month growth rate that ranks in its bottom 15th percentile while real sales growth ranks in its bottom 26th percentile.

Other retail surveys in the bottom panels of the table flesh out further trends for retailing. Passenger car registrations ranked on year-on-year growth have a stronger rank than sales but still are below median 46th percentile standing.

In November, the CBI survey rated sales as relatively strong for this time of year with a 77.1 percentile standing. Still, the volume of orders in that survey is weak with only a 27th percentile standing; consumer confidence has only a 30.8 percentile standing.

The sequential calculation for the indicators shows net changes over three months, six months and 12 months. On those metrics, consumer confidence is net lower over 12 months and gaining no momentum in more recent periods. Sales for time of year are higher on all periods. Year-over-year orders have strong gains posted over three months and six months, but they are only digging themselves out of a hole since they are still net lower over 12 months. On balance, the CBI changes don’t seem to add much to our understanding while the rank standings for the CBI measures seem to paint a pretty clear picture of where retailers stand.

The inflation metrics remind us that a year ago inflation was excessive at 3.7%, but it is now well under the radar at a 1.5% pace. Meanwhile, both real and nominal sales have slowed. The U.K. national election has helped to give the economy leadership and direction, but there are still major issues to be settled and evidence of new friction as Scotland wants another referendum vote as it is less interested in leaving the EU than the rest of the U.K. On that score, there are also restive conditions in Northern Ireland about how it will be treated under Brexit pull out. There is no sugar-coating the fact that despite a clear decisive national election, some conditions in the U.K. simply remain contentious and in flux. Economic uncertainty remains as issue in the U.K.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief