Global| Dec 20 2018

Global| Dec 20 2018U.K. Retail Sales Advance on Strong 'Black Friday' Sales, But Weakness Has Not Been Reversed

Summary

U.K. retail sales in November were bolstered by solid 'Black Friday' sales as the holiday selling period kicked off. Despite the November jolt in sales that reverses two straight months of declines, U.K. retail sales are still [...]

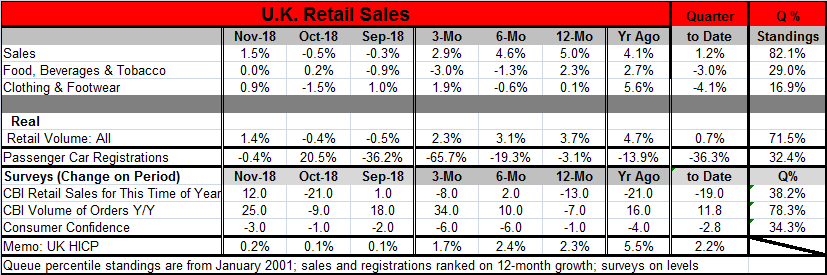

U.K. retail sales in November were bolstered by solid 'Black Friday' sales as the holiday selling period kicked off. Despite the November jolt in sales that reverses two straight months of declines, U.K. retail sales are still trending lower as 12-month growth at 5% erodes to an annualized pace of 4.6% over six months and to 2.9% over three months. Over the same monthly sequences, real retail sales (sales volume) slow from a rise at a 3.7% pace over 12 months to 3.1% over six months and 2.3% over three months.

U.K. retail sales in November were bolstered by solid 'Black Friday' sales as the holiday selling period kicked off. Despite the November jolt in sales that reverses two straight months of declines, U.K. retail sales are still trending lower as 12-month growth at 5% erodes to an annualized pace of 4.6% over six months and to 2.9% over three months. Over the same monthly sequences, real retail sales (sales volume) slow from a rise at a 3.7% pace over 12 months to 3.1% over six months and 2.3% over three months.

Also disturbing is the ongoing weakness in passenger car registrations. Registrations fell by 3.1% over 12 months after a 13.9% drop in the 12-month period before that. Over short horizons, registration weakness has persisted and even intensified with six-month registrations off at a 19.3% annual rate and three-month registrations off at a 65.7% annual rate.

The retail surveys and the actual retail sales data both show some irregularity in terms of their strength. Since you can't compare a year-on-year sales gain to a sales survey diffusion response directly, I have subjected all the series in the table to a queue ranking process that permits some direct comparisons. I rank retail sales based on year-on-year growth and I rank the CBI survey responses on their survey diffusion metrics. Nominal retail sales show an 82nd percentile queue standing, higher than the 71st percentile standing for retail volume also ranked as a 12-month growth rate. Year-over-year passenger car registrations percentage changes have a lower 30th percentile ranking – quite poor. The CBI sales for the time of year response has a low 38th percentile standing but the volume of retail orders year-on-year survey response has a 78 percentile standing, more in line with real and nominal retail sales. Separately consumer confidence (ranked as an index rather than on is annual growth rate) has a 34th percentile standing.

U.K. inflation on the HICP measure is at 2.3% year-on-year, 2.4% over six months and 1.7% over three months.

BREXIT!

Of course, there is no talking about the U.K. and its prospects without a word about Brexit. So here it is Word: Brexit!

Brexit is coming. But no one is quite sure of what it will be. It's like the old joke about the 'Viper.' A secretary gets a call and man's voice says, “I am the viper!” She hangs up. Then it happens again. She calls the police. The next day, with an officer protecting her, there is a knock on the door. She opens it. And old man with a moustache, a bucket and a squeegee says “I am the viper, I've come to vipe your vindows! I tried to make an appointment but someone kept hanging up on me….”

So Brexit is coming. But what will it be? Theresa May says she has cut the best deal possible and it should be approved; it is the will of the people. But there is opposition to it. It is possible but not likely that the EU would be willing to make some further accommodation if Parliament rejects this deal, but not much.

Some think that when Brexit was voted on, people had a distorted view of what it would mean. Now after countless negotiations, Britain knows more or less what Brexit actually will mean. Some think that a hard Brexit is so bad that if there were a new referendum the vote might switch to 'remain.' Of course, no one really knows. And last time the polls on this were terribly wrong. So even a new referendum is a roll of the dice. But it would be a vote taken with a much clearer idea of what is being voted on. You know, if the secretary in the story above knew who/what the viper was, she never would have called the police in the first place. But hindsight is often 20/20. A new referendum would be like stepping into a time capsule and re-voting…but with more knowledge, but still not exactly that.

For its part, the Bank of England has cut its forecast based on the notion that Brexit is coming and on the growing probability that it will be a hard Brexit. The bank sees inflation coming down into line at the same time. If there is a new referendum with a changed result, the new BOE forecast will have to be redone as well.

The Brexit process has been difficult for everyone. If the U.K. were to re-referendum and were the result to switch to 'remain,' would all the lost City of London jobs come back? Would the U.K. retrieve the EU ministries that had migrated across the channel? Would all the departed bankers return? How much would things actually go back to 'the same' normal? Would the dispelled expats come back? Would Scotland still go ahead with its talk of another referendum on its membership in the U.K. or would continued EU membership placate them?

Some things never can go back the way they were. With the revote situation in mind, I still wonder what the U.K. would see. I wonder if relations with Spain have been irreparably harmed over its stance regarding Gibraltar. A new referendum even with a changed vote result still comes with its own bundle of uncertainty. Mr. Carney could breathe a sigh of relief and prepare for his own exit. PM May would probably face all sorts challenges to her government once the future had been made clear and the no-win stand-off vs. the EU had been set aside. Suddenly, being PM would be attractive again. But that too is a speculative future.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief